My Journey Witnessing Dubai's Phenomenal Rise

%201-min.avif)

.webp)

I walked through Dubai for the first time in the late 1980s. The Royal Abjar Hotel was the address for anyone who wanted to say they had stayed somewhere serious. Al Ghurair Mall was the centre of commerce and social life. The skyline was modest. The pace was unhurried. Nothing about the city suggested what was coming.

Forty years later, the same patch of coastline runs the tallest building in the world, an airline that touches every continent, and a tourism economy that pulls in more visitors than London. The journey from one to the other was not luck. It was a sequence of decisions, made over decades, by leadership that understood what the city was trying to become.

I am writing this in 2026 because every other Gulf state, including Kuwait, is now trying to repeat some version of the Dubai playbook without doing the part where Dubai sustained those decisions across forty years and two near-collapses. The interesting question is not whether Dubai succeeded. The interesting question is which parts of what Dubai did actually transfer, and which parts were specific to a moment that cannot be re-staged. This is what I saw, decade by decade, and what I think Kuwait should and should not take from it.

The 1980s: Starting From a Number Nobody Now Remembers

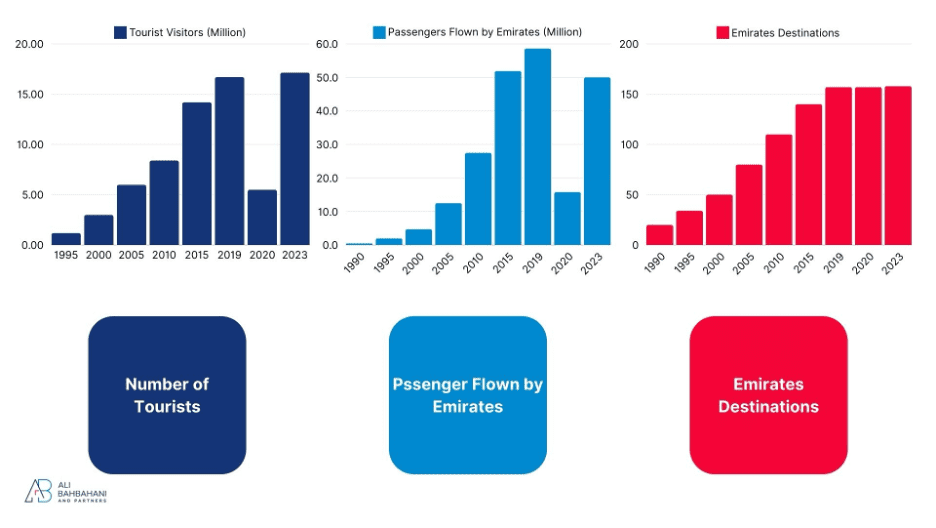

In 1980 Dubai had a population of about 276,000 and a GDP of roughly $3 billion. By 1985 the population had moved to 370,800 and GDP to about $8 billion, almost entirely on oil. No serious tourism data existed. The hotel inventory was minimal. Emirates Airline had not yet been founded; it took its first flights in 1985 with two leased aircraft.

What the city did have was a leadership willing to act on a piece of analysis nobody around the Gulf wanted to act on at the time: oil was finite, the runway was twenty to thirty years, and the work to replace oil revenue with something else had to start before the oil ran out, not after. That is the single decision that defines everything that follows. Every other Dubai story is downstream of it.

The 1990s: Building the Foundation

By 1990 Dubai had reached around 550,000 people and a GDP of roughly $11 billion. The hotel base was still small. Emirates Airline, five years old, served about 20 destinations and carried around half a million passengers. The numbers were not impressive in absolute terms. What was significant was the direction.

By 1995 the population had grown to 689,000 and GDP had nearly doubled to $18 billion. The hotel count was around 200. Dubai recorded roughly 1.2 million tourists for the year, which was the first measurable signal that the destination work was paying back. Emirates was now flying to 34 destinations and carrying 2 million passengers. The City Centre Mall opened in 1995 and set the template that almost every later development copied. By the end of the decade the Burj Al Arab opened on its man-made island and gave the city the photograph it would use to introduce itself to the next twenty years of travellers.

The 2000s: The Decade the Bet Paid Off

By 2000 Dubai was at 862,000 people, GDP of $30 billion, 3 million tourists a year, 300 hotels. Emirates was at 50 destinations and 4.7 million passengers. The plan from the 1980s was no longer a plan; it was a working economy.

I lived in Dubai for six months in 2002. Palm Jumeirah was under construction. Jumeirah Beach Residence was a sand lot. The Sheikh Zayed Road had visible gaps between buildings that today are completely filled in. The city felt ambitious in the specific sense that you could see the work and the work made you assume the outcome.

I also spent that period closer to the horse racing scene than I expected to. I attended the Dubai World Cup in the early 2000s and watched the meeting develop into the Dubai Racing Carnival that now pulls top horses and jockeys from every major racing jurisdiction. That growth tracked the city growth almost exactly: the same compound investment, the same patience, the same willingness to lose money for a decade while building the asset.

By 2005 the city was at 1.2 million people, $46 billion GDP, 6 million tourists, around 350 hotels. Emirates was at 80 destinations and 12.5 million passengers. Jumeirah was still mostly a construction site, with the billboards that I remember most clearly: full-resolution renderings of waterways and skyscrapers and marinas that had no business existing yet, propped up on hoardings in front of empty desert. The thing about Dubai at that point was that those billboards were not aspirational marketing. They were construction schedules.

Emirates as Strategy, Not Just Airline

Emirates was founded in 1985 as a government-owned carrier with one mission that was never disguised: serve the city. By 2002 the network was at over 60 destinations. By 2005 it was 80 destinations and about 12 million passengers. By 2020 it was 157 destinations and 58.6 million passengers.

The structural choice that made Emirates work for Dubai was the stopover. The fares were priced to encourage travellers to break their journey in Dubai for two or three days, with hotel packages that put them inside the city rather than the airport hotel zone. The result was that millions of people every year were not flying through Dubai; they were tasting it. A meaningful percentage of them came back as tourists, and a smaller but significant percentage of those came back a third time as residents, investors, or business operators.

Most analysts framed Emirates as a national airline. I think that framing misses the point. Emirates was Dubai's acquisition channel. The product on sale was the city itself; the airline was the funnel. Every other piece of the city's economy benefited from that funnel because it was always full.

The Lead Generation Engine

Emirates worked as a lead generation tool for the city. That phrase sounds reductive but it is what was actually happening. The mechanism was deliberate:

- Lead capture. Every transit passenger who took a stopover became a recorded contact for the destination. They walked through the duty-free zone, slept in a Dubai hotel, ate at a Dubai restaurant, and left with a passport stamp.

- Nurture. The first impression was deliberately designed to feel familiar to the upper-middle-class traveller. English everywhere, no friction at the airport, hotel service to international standard, ride-hailing that worked, recognisable retail. The unfamiliar was offered as optional, not mandatory.

- Conversion. Of the millions who came through once, a meaningful share came back as tourists. Of those, a smaller share started looking at long-term visas and property. Of those, a smaller share moved.

- Diversity by design. Emirates' network was deliberately wide. The result was an expat population spread across more than 200 nationalities, which made the city feel like a global average rather than a Gulf city.

The Property Glance

Walking through Dubai International Airport, you would pass property advertising at scale that no other airport in the region ran. High-rise apartments with Gulf views, villas on man-made islands, penthouses over the skyline. Aimed at someone with a four-hour layover and a phone.

I noticed it on every transit. So did everyone I have ever talked to who came through DXB in those years. That advertising was not designed to convert in the airport; it was designed to plant the question. The conversion happened months later, when the same person was in their own city dealing with their own logistical problems and the Dubai option resurfaced as an alternative.

This is the part of the Dubai story that gets least credit and that deserves most. The acquisition funnel for residents was not handled by the real estate sector. It was handled by the airline and the airport, working as a single advertising surface aimed at a captive audience of high-intent travellers. Real estate then closed.

Palm Jumeirah completed in the 2010s and added more than 500 kilometres of coastline that did not exist before. The luxury hotel inventory that followed it gave the city the high-end positioning it had been building toward since the Burj Al Arab. The Palm is visible from space, which is the kind of detail that turns into an icon faster than any campaign can.

The 2008 Crisis: The Part Nobody Wants to Copy

The 2008 financial crisis hit Dubai hard. The growth model had become dependent on a constant flow of foreign capital and rising property prices, and when both stopped at once, the city ran into the kind of debt problem that can end a country's development arc.

- Bond yields. Yields on Dubai government bonds surged on default fears. By late 2009 the yields on bonds issued by Dubai World, one of the largest state-owned holdings, had risen to around 12%. Dubai World announced a restructuring of approximately $26 billion in debt. Global markets reacted accordingly.

- Stock market. The DFM General Index dropped by nearly 70% from its 2008 peak. Liquidity in speculative sectors disappeared.

- Mega-projects. Nakheel's "The World Islands" and "Palm Deira" stalled. The "Dubailand" entertainment complex, planned across 278 square kilometres, was delayed indefinitely. A long list of hotel and residential projects was either postponed or cancelled.

Two things saved the city. The first was a $10 billion bailout from Abu Dhabi that stabilised the balance sheet and restored some investor confidence. The second was a real change in how Dubai talked about growth, with a more credible emphasis on tourism, logistics, and financial services as the durable sectors and a quieter set of expectations for speculative real estate.

By 2010 the city was at about 1.9 million people, GDP of $76 billion, 8.4 million tourists, around 400 hotels. Emirates was at 110 destinations and 27.5 million passengers. The recovery worked.

The point Kuwait should take from this is not that the recovery worked. It is that the crisis happened in the first place. Dubai's growth in the 2000s was levered, speculative, and ultimately had to be bailed out by a neighbour. The story is told in retrospect as ambition rewarded. At the time, it was a credit market that ran into a wall. The version of the Dubai playbook that any other Gulf state should run is the one Dubai itself ran after 2010, not before.

The 2010s: After the Reset

The Burj Khalifa opened in 2010. At 828 metres it was the tallest building in the world by a margin large enough that the record will not be casually broken. The opening was a signal to a global capital markets audience that Dubai was back. The fact that the tower was largely funded before the 2008 crisis and finished into the recovery was useful timing rather than design, but the symbolism worked.

Closer to my interests, Meydan Racecourse opened in 2010. It was a properly serious racecourse, built to the standard the Dubai World Cup had already set on lesser tracks. From that point the racing calendar in Dubai started attracting Group 1 owners from Europe, the US, Japan, and Australia. The Dubai Racing Carnival worked because the prize money was real and the surface was right; the symbolism alone would not have done it.

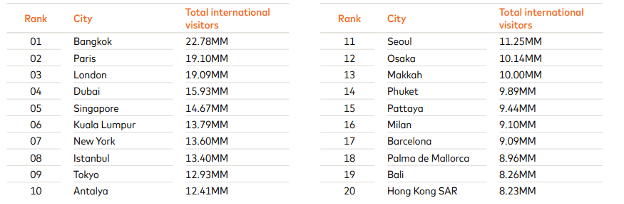

Dubai's tourism numbers through the decade told the same story as the rest of the economy. By 2019 the city was in the global top ten most-visited cities and posted 16.7 million international overnight visitors. The key numbers for the decade:

- Population in 2020: ~3.3 million

- GDP in 2020: ~$102 billion

- Tourist visitors in 2019: ~16.7 million

- Number of hotels in 2020: ~700

- Emirates destinations in 2020: 157

- Passengers flown by Emirates in 2019: ~58.6 million

The Projects That Mattered in the 2010s

Not every mega-project from this decade has held up. The ones that did are worth naming because they show what the surviving formula looked like.

- Atlantis, The Palm. Anchor hotel for Palm Jumeirah and the property that proved the Palm could carry premium hospitality at scale.

- Dubai Opera. Opened 2016. A real cultural venue, not a vanity build. Programming has been credible and consistent.

- Bluewaters Island and Ain Dubai. Launched in 2018, Bluewaters Island added a new mixed-use district. Ain Dubai, at 210 metres, is the world's largest observation wheel. It has had operational issues since opening but it remains an iconic skyline anchor.

- Dubai Creek Harbour. Designed around a tower planned to surpass the Burj Khalifa. Slower-paced than the 2000s mega-projects, which is partly intentional and partly a function of post-2008 caution. Dubai Creek Harbour as a development is now substantially built out.

The Tourism Economy at Full Cruise

By the end of the 2010s, Dubai was ranking around fourth most-visited city in the world, behind Paris, Bangkok, and London. That ranking was a result of compounding work over thirty years: every decade had added a layer (the airline, the hotels, the shopping festivals, the iconic architecture, the cruise market, the cultural programming) and by 2019 all of them were running in parallel. There was no single thing that made Dubai a top destination. There were twenty things, each of them visible and each of them running for long enough that they had built reputation.

COVID-19: The Test Dubai Passed

The pandemic was the most serious threat to the post-2008 Dubai model. A tourism-dependent city, hyper-connected by an airline that needed wide-bodies flying full to break even, with a workforce that was 85% expat and could leave on short notice. None of the underlying numbers worked if global travel did not come back.

What Dubai Did Differently

Three things distinguished Dubai's pandemic response from regional peers.

- Testing and vaccination at scale. Rapid PCR testing was set up across the city. As vaccines arrived, the UAE ran one of the most aggressive vaccination programmes in the world. By mid-2021 over 85% of the eligible population was vaccinated.

- Digital infrastructure. The Al Hosn app handled test results, vaccination records, and exposure notifications. The same infrastructure made venue check-ins and travel clearance fast enough that the visitor friction never spiked.

- Early reopening. Dubai reopened to international tourism in July 2020, while most major destinations were still closed. The signal that sent was that Dubai had measured the risk, taken it, and bet on operational competence to manage the consequences.

To support the reopening, Dubai launched the "Dubai Assured" certification programme for hotels, restaurants, and attractions. The standard was real enough that international travellers used the certification as a decision input. The marketing followed the operational reality rather than running ahead of it, which is the inverse of how most national tourism boards handled the same moment.

The Numbers

In 2021, while global tourism remained at historic lows, Dubai recorded over 7 million visitors. That was not a return to pre-pandemic numbers. It was a meaningful share of them captured in a year when most destinations recorded almost none. The events calendar resumed quickly: GITEX Technology Week in October 2020 was one of the first in-person tech conferences in the world; Expo 2020 ran from October 2021 to March 2022 and drew over 24 million visits.

The strategic lesson from the pandemic is the one most people miss. The reason Dubai recovered fast was not that the response was fast. It was that the city had spent twenty years building the kind of infrastructure (airport capacity, hotel inventory, digital governance, regulatory flexibility) that allowed it to respond fast when it mattered. The response was the visible part. The capacity to respond was the part built earlier, in conditions that did not look like crises.

The 2020s: Doubling Down

Post-pandemic, Dubai entered the 2020s with the same posture as before but with a different rhetorical emphasis on diversification, knowledge work, and long-term residency. The headline metrics:

- Population. Around 3.5 million by 2023, growing as remote workers, founders, and high-net-worth households continued to relocate.

- Digital economy. The Dubai Digital Economy Strategy is targeting a doubling of digital economy contribution to GDP by 2031. The fintech and Web3 corridors built out of DIFC are visible enough that the targeting is credible rather than aspirational.

- Tourism. 2023 surpassed the 2019 pre-pandemic peak. The city is now consistently one of the top three or four destinations globally by overnight visitor count.

The Active Mega-Projects

A short, honest list. Some of these projects are working. Some have been quietly trimmed.

- Dubai Creek Tower. Still planned to surpass the Burj Khalifa. Progress has been slower than the original timeline. The site is active but the completion date has slipped several times. Honest framing: this one is real but on a different schedule than originally communicated.

- Royal Atlantis Resort & Residences. Completed in early 2023. Has performed at the high end of the city's luxury hotel inventory. Residential pricing has held.

- Mohammed Bin Rashid (MBR) City. The mixed-use development continues to build out. District One, the inner lagoon community, has matured as one of the strongest residential addresses in the city.

- Expo City Dubai. The Expo 2020 site has been repurposed as a mixed-use district. Occupancy and programming have been credible. This is the model for how a single-event site should be retained, and the contrast with most former Expo and Olympic sites globally is significant.

Technology and Visa Engineering

The 2020s shift toward knowledge work has been explicit. Three policy moves matter:

- Remote work and freelance visas. Dubai introduced specific visa categories for remote workers and freelancers serving clients abroad. The category is now competitive with Lisbon, Bali, and Mexico City for the digital-nomad audience and has the advantage of Gulf time zones and Tier 1 infrastructure.

- Golden Visa. A ten-year residency category for investors, founders, specialised professionals, and high-net-worth individuals. The Golden Visa is the single most consequential immigration product in the region. It has reset relocation calculus for a global audience.

- Blockchain and fintech. DIFC's Innovation Hub now hosts over 500 fintech firms and startups. The Dubai Blockchain Strategy commits to digitising government transactions on-chain. The execution has been variable but the direction is clear enough that international fintech operators take it seriously.

Real Estate, Honestly

The 2020s residential market has been one of the strongest globally, driven by relocations of high-net-worth households from London, Moscow, Mumbai, and Singapore. The Golden Visa is the structural driver.

- High end. District One, Bluewaters, Palm Jumeirah, Royal Atlantis residences. Pricing has continued to climb on global wealth flows.

- Mid-market. The mixed-use developments around MBR City, JVC, Dubai South. These have been the demand absorber for the wave of middle-income expats following the high-net-worth wave.

- Caveat. Dubai property has had two major downturns in twenty years (2008-2010, 2014-2016). The current cycle is healthier than either but the question of how the market handles a global wealth-flows reversal is open. The 2008 lesson was that leverage at the developer level is where the city is most exposed. Whether the current developer leverage is materially lower than 2008 is a question the city's analysts disagree on.

The Event Economy

Dubai's 2020s event calendar has stayed dense. Dubai Shopping Festival, Art Dubai, GITEX, COP28, the Dubai World Cup, Formula 1 events, UFC. Each one runs as a destination event in its own right. The aggregate effect is that the city is never out of season, and the tourism numbers have stayed flat against seasonality in a way no other Gulf destination has matched.

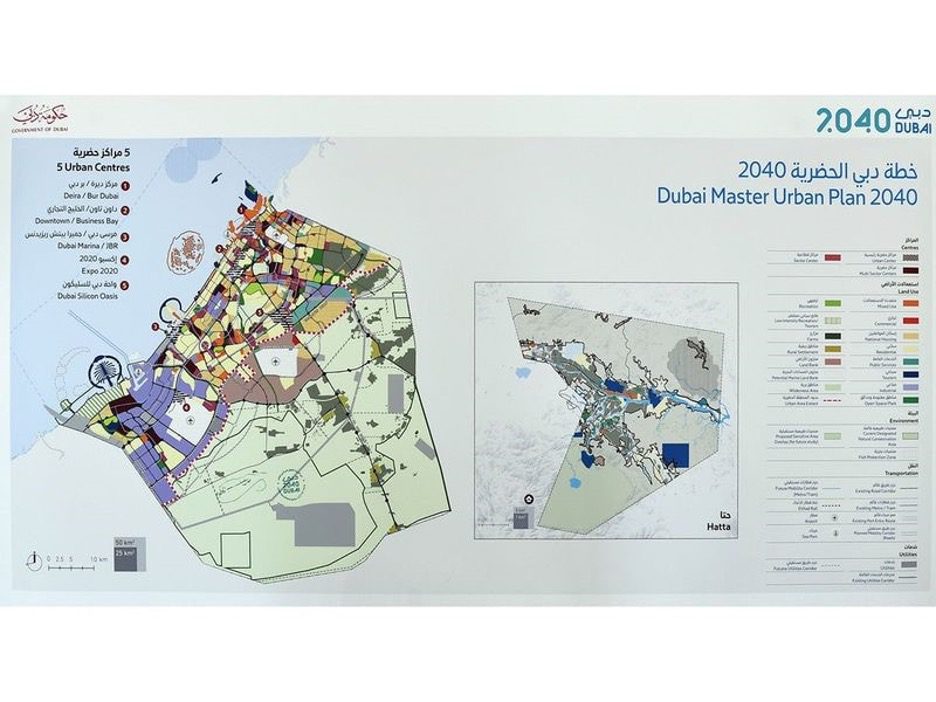

The 2040 Master Plan

Dubai's leadership has published the Dubai 2040 Urban Master Plan as the framework for the next two decades. The document is detailed and the parts most worth flagging are the parts that signal where the leadership thinks the model has reached its limits and needs to evolve.

- Population target of 5.8 million by 2040. Continued absorption of global talent, with infrastructure planned at parity with the growth.

- Green spaces +105%. Doubling of public green space per capita. The implicit acknowledgement is that the current liveability ratio is below where leadership wants it to be.

- 20-minute neighbourhoods. Pedestrian, cycling, and public transport priority. This is a structural reversal of the 2000s car-dependent development pattern and is the most ambitious part of the plan because the existing built form makes it expensive.

- Knowledge economy. Innovation districts for technology, biotech, digital media, renewable energy. The explicit acknowledgement that tourism and real estate can no longer be the lead growth drivers.

- Mobility target. 55% of population travel by public transport, cycling, or walking by 2040. Currently nowhere near that. The metro and tram networks are expanding; the Hyperloop remains aspirational rather than scheduled.

- Carbon neutrality. Solar and waste-to-energy investments. Natural reserves and mangrove expansion along the coast. The Clean Energy Strategy 2050 sits underneath this.

- Global business hub. Continued investment in free zones and East-West trade infrastructure.

Emirates Today

Emirates continues to function as the lead acquisition channel. The current scale:

- Fleet: Over 270 aircraft, including the world's largest fleet of Airbus A380s.

- Service standard: Consistently in the global top three by passenger experience surveys.

- Economic footprint: Materially significant contributor to Dubai GDP and to employment across hospitality, retail, and logistics.

Why People Move

The pull factors that make Dubai work as a relocation destination are now well understood. The honest list:

- Population mix. Over 85% expat from more than 200 nationalities. A new arrival does not have to integrate into a host culture; they integrate into a global average. This is structurally different from every other major destination.

- Infrastructure. Healthcare, education, transport, and digital governance all at international standard.

- Tax. No personal income tax. The single most consequential pull factor for professionals at high marginal tax rates elsewhere.

- Climate caveat. Worth saying honestly: four months a year the heat makes outdoor life impractical. Anyone weighing relocation should be told this and not sold a year-round Mediterranean fiction.

Personal Reflection

Watching Dubai over forty years has been a long-running case study in compound returns. The city I walked through in the late 1980s and the city I land in today are not on the same scale, and the bridge between them was built by a leadership that kept making the same kind of decision (long-horizon, infrastructure-first, demand-creating) over and over until the decisions accumulated into a city.

What Kuwait Should and Should Not Take From This

This is the part that matters for anyone reading this in Kuwait, Doha, Riyadh, or Manama. The Dubai story gets used as a generic template for Gulf city ambition, and the template is mostly wrong. Here is the version I would actually run.

What transfers. The acquisition funnel architecture. Dubai used an airline as an advertising channel for the city, and the city as a product the airline could deliver. Any Gulf state with a national carrier should be running that playbook hard. Kuwait Airways and Jazeera Airways are nowhere near the conversion engine that Emirates is, and the fix is not aircraft. The fix is product integration with hotels, tourism boards, and visa policy. I have written about the same gap on the booking side in our GCC airline case study.

What transfers, with adjustments. The visa engineering. Long-term residency products work because they reset the calculus for high-skill mobile professionals. Dubai's Golden Visa and remote work visas are now copied across the Gulf. The Kuwait version of this exists only at the corporate level and is not consumer-facing. The fix is small in design effort and large in commercial impact.

What does not transfer. The 1980s-to-2000s leverage curve. Dubai built its tourism inventory on debt that almost broke it in 2008. Any state trying to replicate the scale-fast approach today is doing it in a global capital markets environment that is far less forgiving. The version of the Dubai playbook that works now is the post-2010 version: diversified, slower, less levered, more focused on knowledge work.

What no one should try to repeat. The iconic architecture race. The Burj Al Arab worked because it was first. The Burj Khalifa worked because it was, and remains, the tallest. The third or fourth or tenth iconic tower in the region has no marketing value because the photograph is no longer new. Kuwait has spent a lot of effort on iconic projects (JACC, the towers) and the return has been low because the global audience has been visually saturated since 2010. The investment should go elsewhere.

The honest summary. Dubai succeeded because it made the same long-horizon decision in 1985 and kept making it through two crises. The decision was to build the infrastructure of a destination before there was demand for it, and to let the demand catch up. That part is replicable, but it requires forty years of patience and political continuity, and that is the input that is hardest to produce in any other Gulf state. I have argued the case for what Kuwait should actually invest its forty years in across How Kuwait Wins the Visitor Journey. The short version is that the friction is the strategy. Dubai removed friction at scale. Kuwait, for forty years, has not.