Kuwait Absorbed a War in March: What the Data Shows

.webp)

Kuwait Absorbed a War in March. The Data Shows How.

A research note on what the Central Bank of Kuwait's March 2026 data reveals about liquidity, behaviour, and institutional resilience.

On the night of 28 February, I heard the Kuwaiti nationwide siren. This was not a drill. The airport was closed. Iranian drones had struck Kuwait International. It was a shock to the whole of Kuwait. We had been hit by a neighbour we would never have been aggressive towards. Whatever the intentions, whether to strike US bases or something else, the country closed in on itself. We lost lives. We took damage. There were no normal commercial flights. Kuwait Airways had relocated to Dammam. Jazeera was busing passengers across the Saudi border to Al Qaisumah.

I will not write here about the sirens, or the geopolitics, or the war that was dragged to us. Those are not stories for a research note.

What I want to write about is what happened to the numbers.

Kuwait is unusual in this respect: the Central Bank publishes a monthly bulletin that is the closest thing we have to a real-time x-ray of the economy. By the time the March 2026 release came out in late April, the war was no longer a feeling. It was a dataset.

What I found is that almost every behavioural and balance-sheet variable you would expect to move in a regional war did move. And the four anchors that hold the system together did not. Both stories are correct. Kuwait absorbed the shock. The infrastructure held. The space between those two sentences is what this note is about.

A note on the data: banking and card indicators are monthly. Exchange-house currency sales and profit are quarterly, so Q1 2026 should be read as the quarter that includes the March shock, not as a March-only figure.

What changed

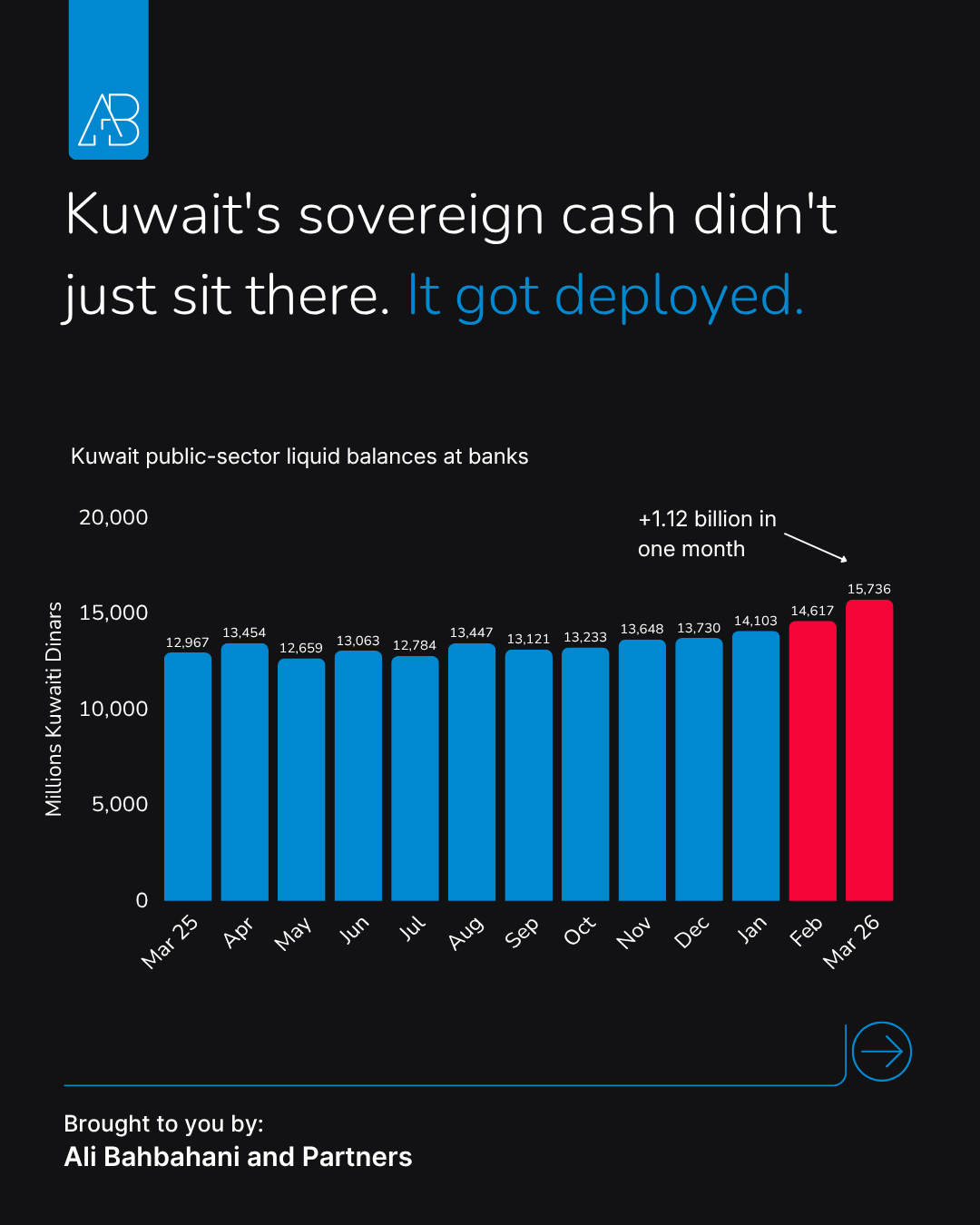

Begin with the most striking number in the release. Public-sector deposits at local banks, the consolidated total of government and public-institution money sitting at Kuwaiti banks, rose by KD 1.12 billion between February and March. That is the largest one-month move in five years. To put it in perspective, the cumulative net change in this line for the entire 2021 to 2024 period was smaller than what we saw in March 2026 alone.

The composition is what gives the move its meaning. Public-institution time deposits rose sharply, while public-institution sight deposits fell. The government's account at the Central Bank declined, while its accounts at local banks rose. A casual reading would call this a number going up. A careful reading sees something more deliberate: liquidity moving closer to the banking system.

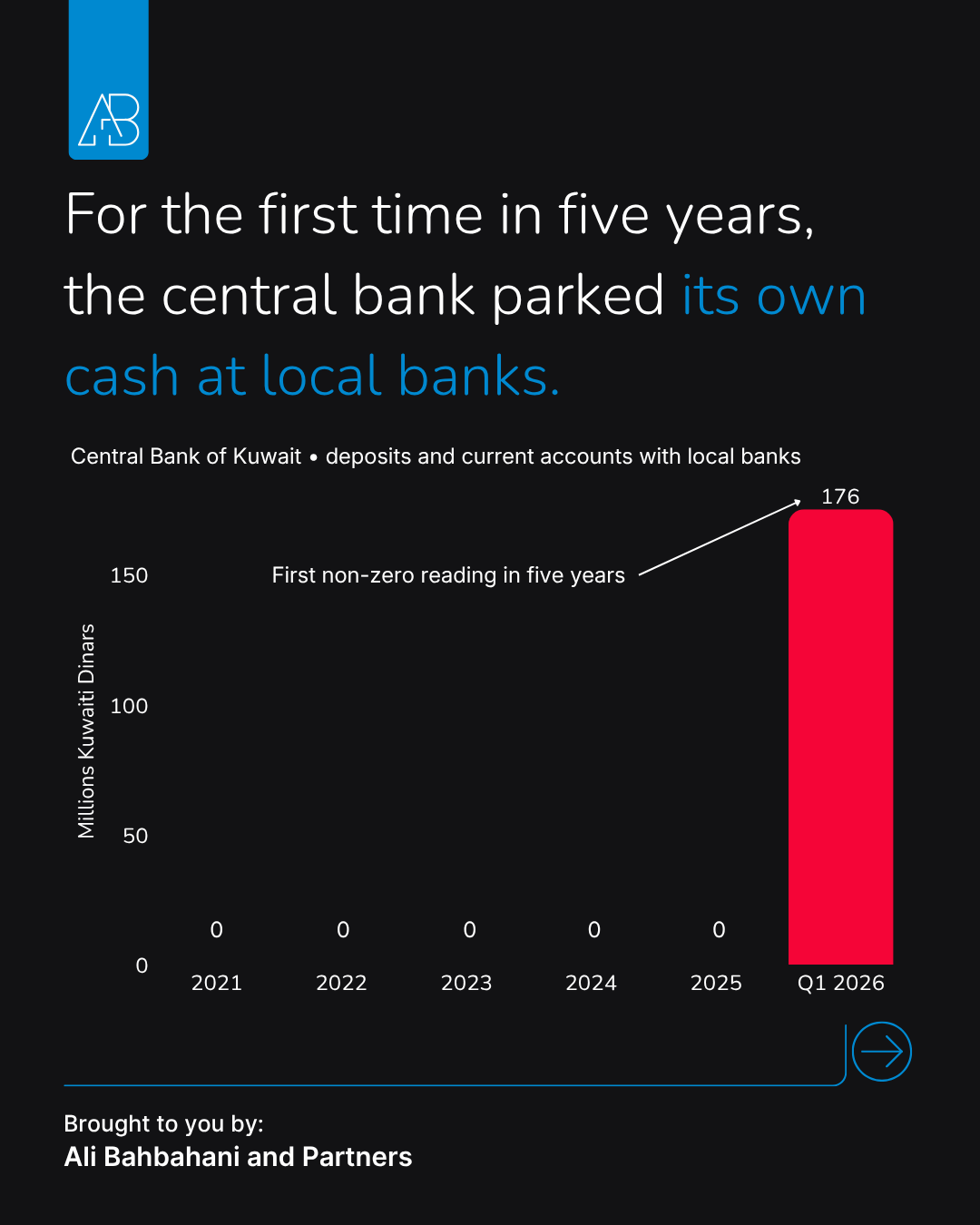

Then comes the line I almost missed on the first read. In Table 4 of the Central Bank release, a column labelled Deposits and Current Accounts with Local Banks tracks how much of the Central Bank's own balance sheet is placed with local banks. For five years it had read zero. Sixty consecutive monthly observations. In March 2026, it read KD 175.5 million.

The amount is small. The signal is not. A five-year zero line does not turn positive by accident. At minimum, it shows an operational decision to place liquidity closer to the commercial banking system during a month when overnight funding became visibly more expensive.

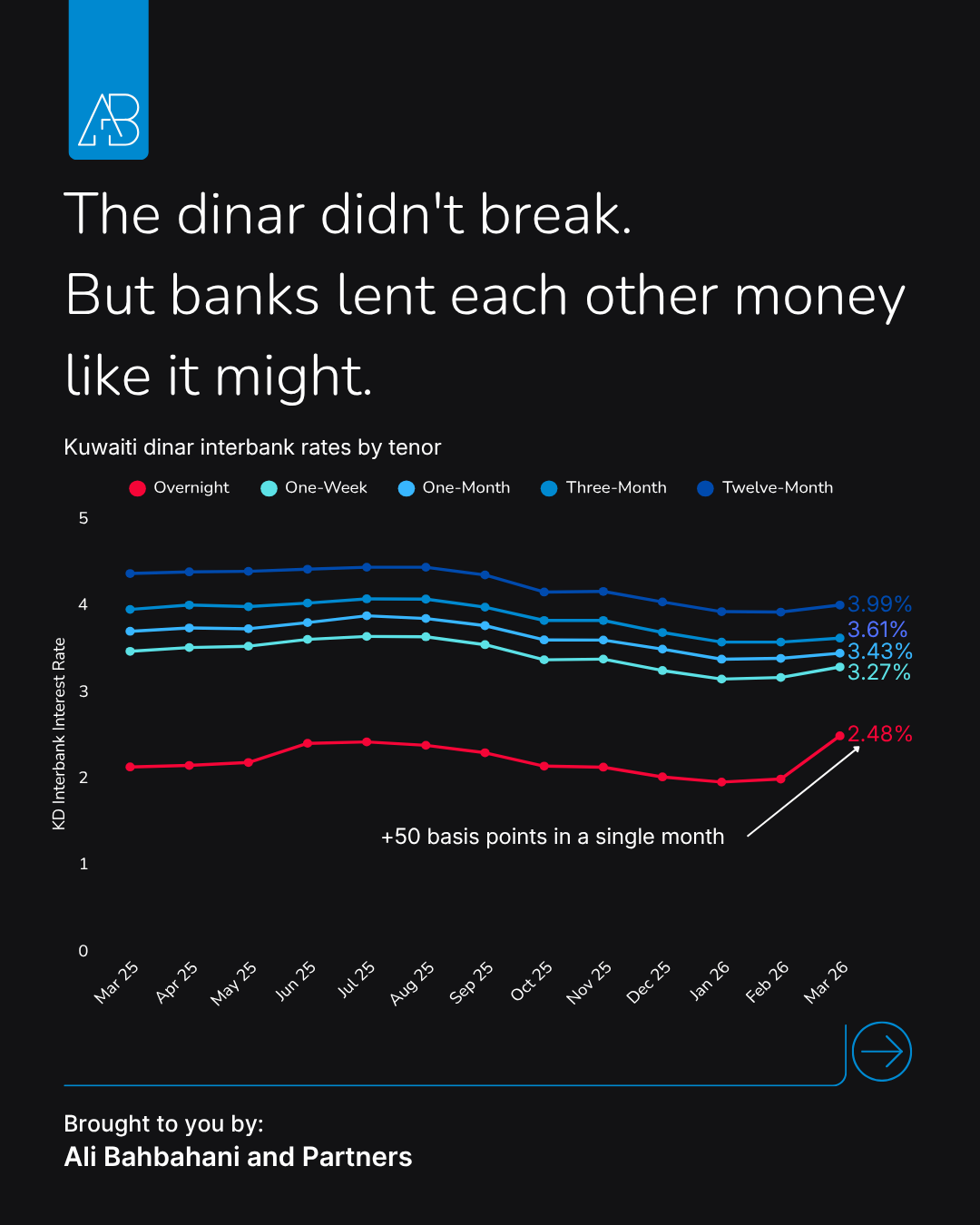

That visible pressure shows up in the third indicator. The overnight Kuwaiti dinar interbank rate jumped 50 basis points in March, from 1.98 to 2.48 per cent, while the longer tenors barely moved. The one-week rate rose only 12 basis points. The three-month rate rose six. The twelve-month rate actually declined by less than two. This is a textbook liquidity-stress signature: banks willing to lend to each other for longer, but charging each other materially more for cash needed tonight. The dinar peg held. The discount rate held. The day-to-day funding market briefly did not.

The important point is not that any single line moved. In a crisis month, many lines move. The important point is that the banking-system indicators moved together. Public-sector balances rose. The Central Bank's own placement with local banks appeared. Overnight funding became more expensive. Reading these three indicators alongside each other, you can see the outline of what looks like a coordinated stabilisation response. The state, in two different forms, put liquidity where liquidity was thinnest, while the price of overnight cash told you why.

That is the state-response trio. Now consider what was happening at the household level.

How people behaved

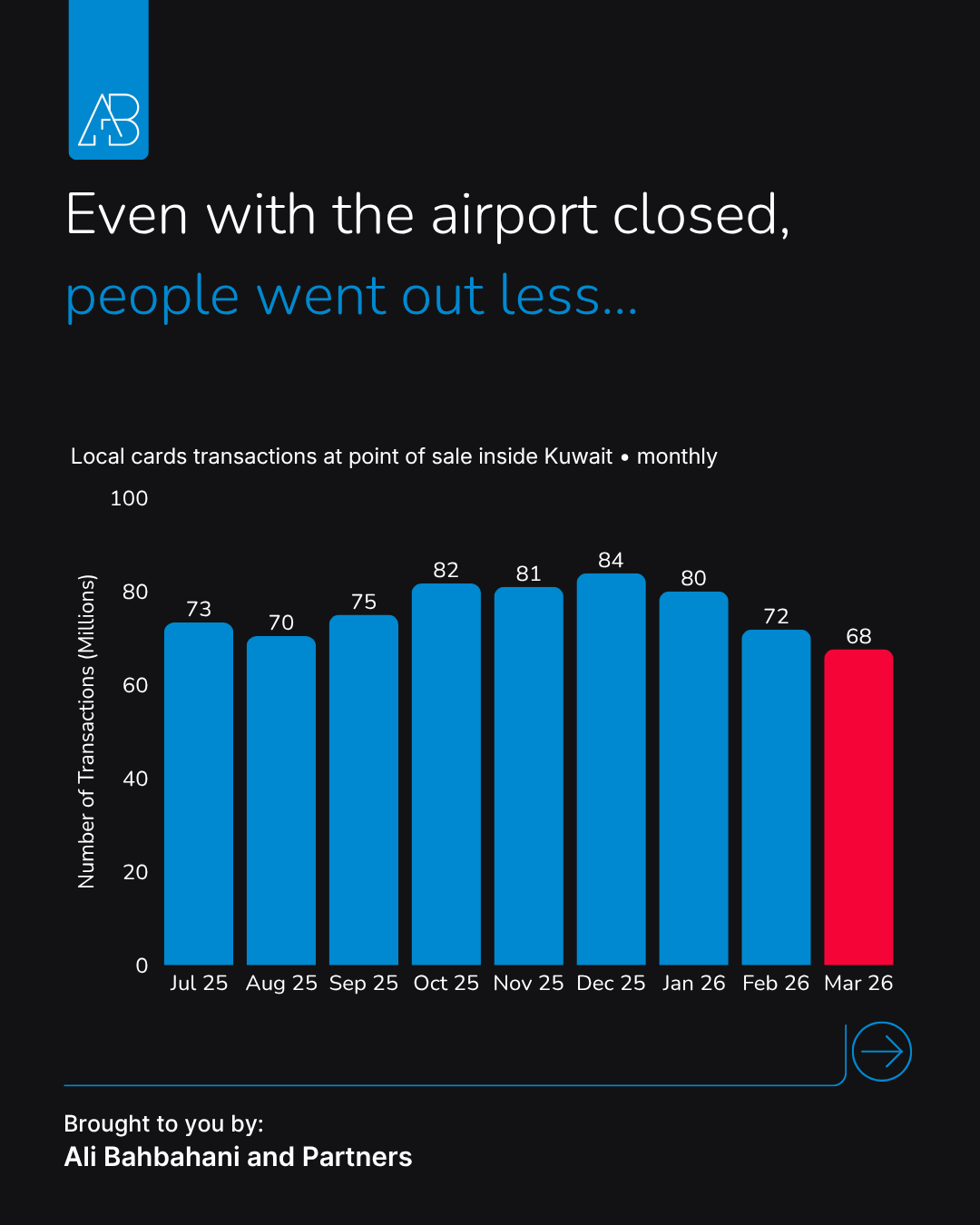

Kuwait International Airport closed on 28 February and remained closed to normal commercial operations through March. Logically, this should have boosted in-country card spending. With nobody able to fly out, more residents would be at home, going to the malls, eating in restaurants, running errands. The captive consumer base should have grown.

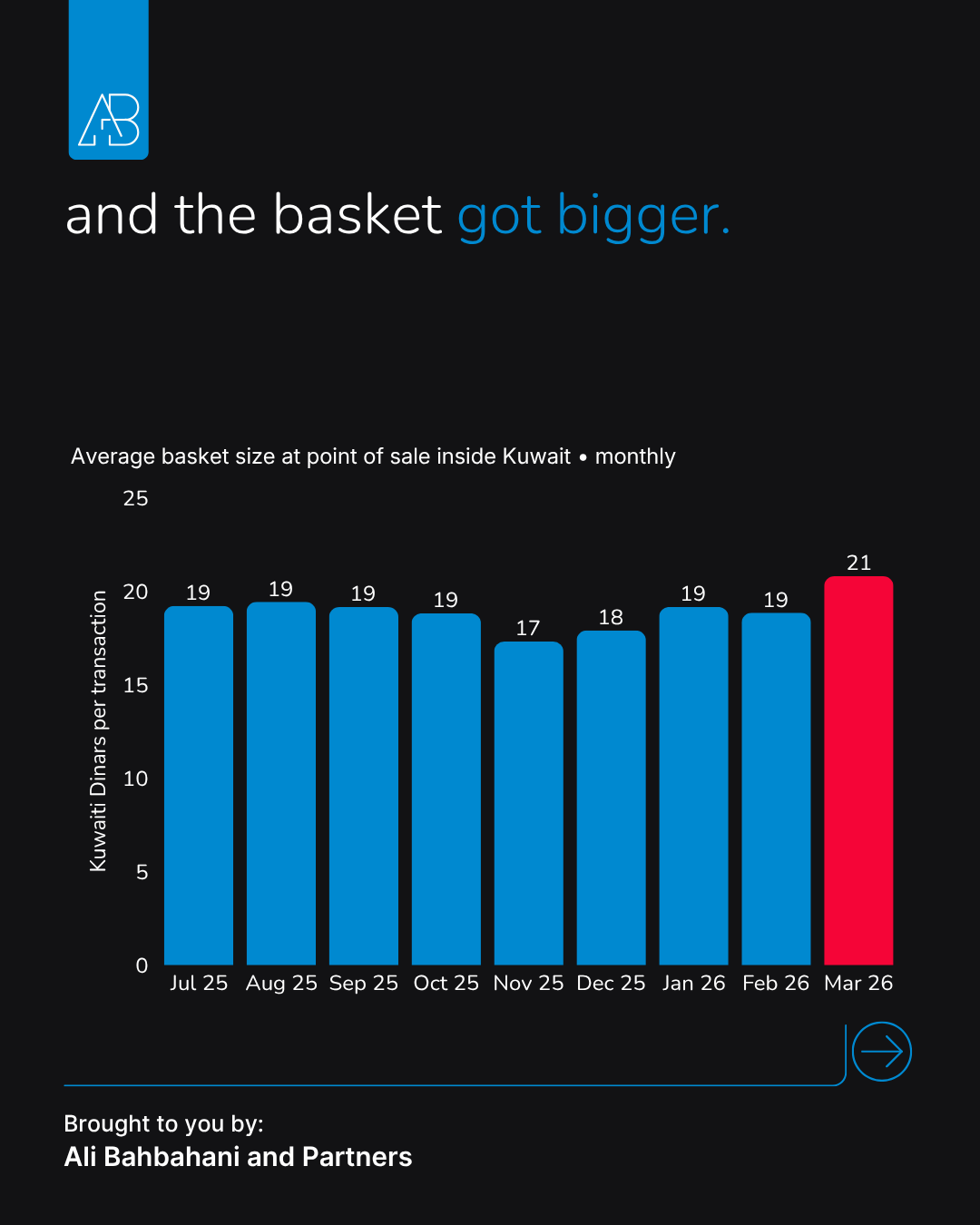

Instead, point-of-sale transactions inside Kuwait fell by almost six per cent month-on-month, from 72 million to 68 million — the lowest reading in the published series.

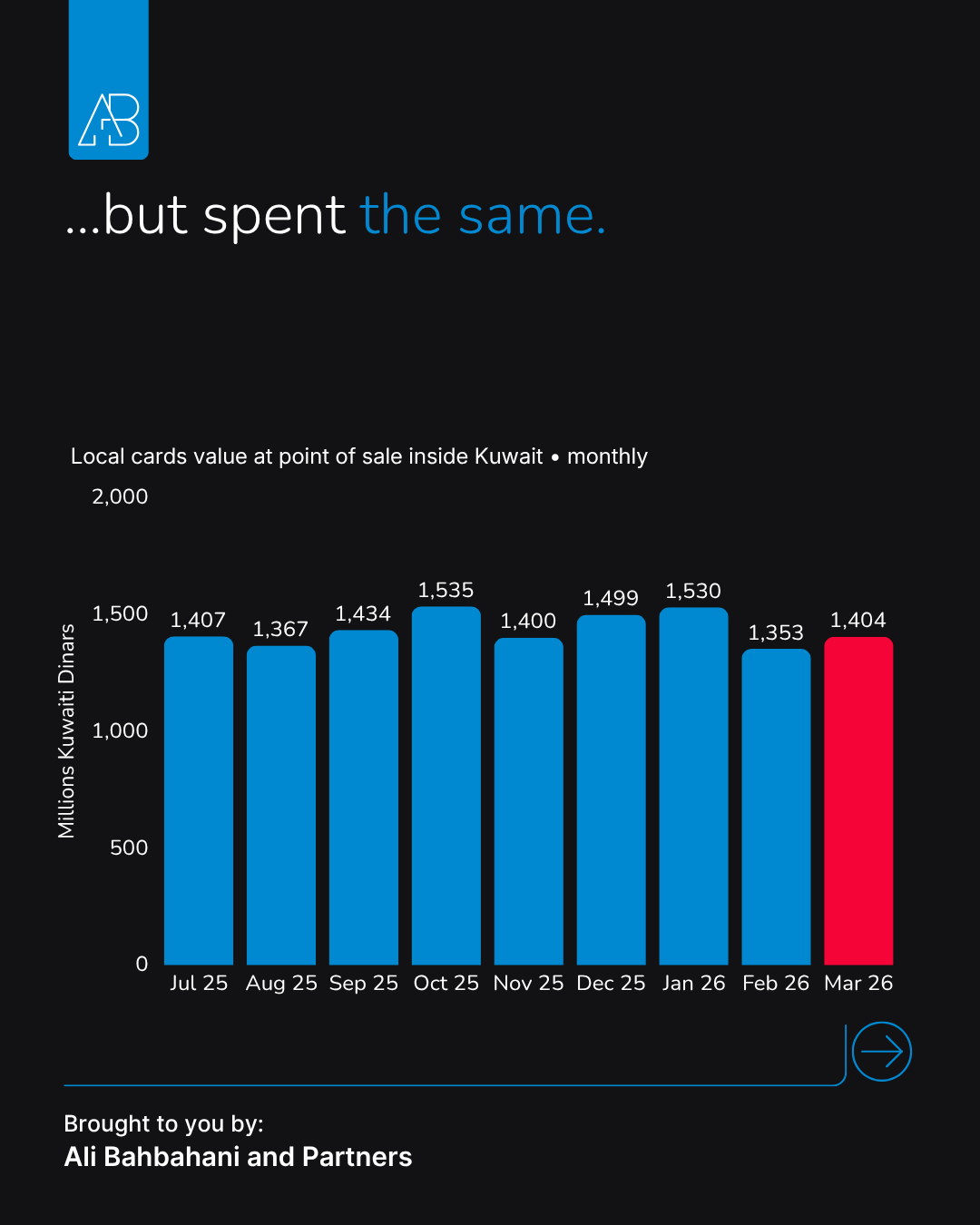

The total spend held roughly flat at KD 1.4 billion.

Which means the average basket grew, from KD 18.84 to KD 20.79 per transaction. A 10 per cent jump.

The pattern looks precautionary. People did not stop spending. They consolidated. Fewer trips, bigger baskets. Anyone who has lived through a regional crisis recognises this rhythm immediately. You go out less. When you do go out, you buy more. You stock up on things you do not normally stock up on. The basket size jumping while the trip count fell is the data signature of a country that read the situation correctly and acted on it.

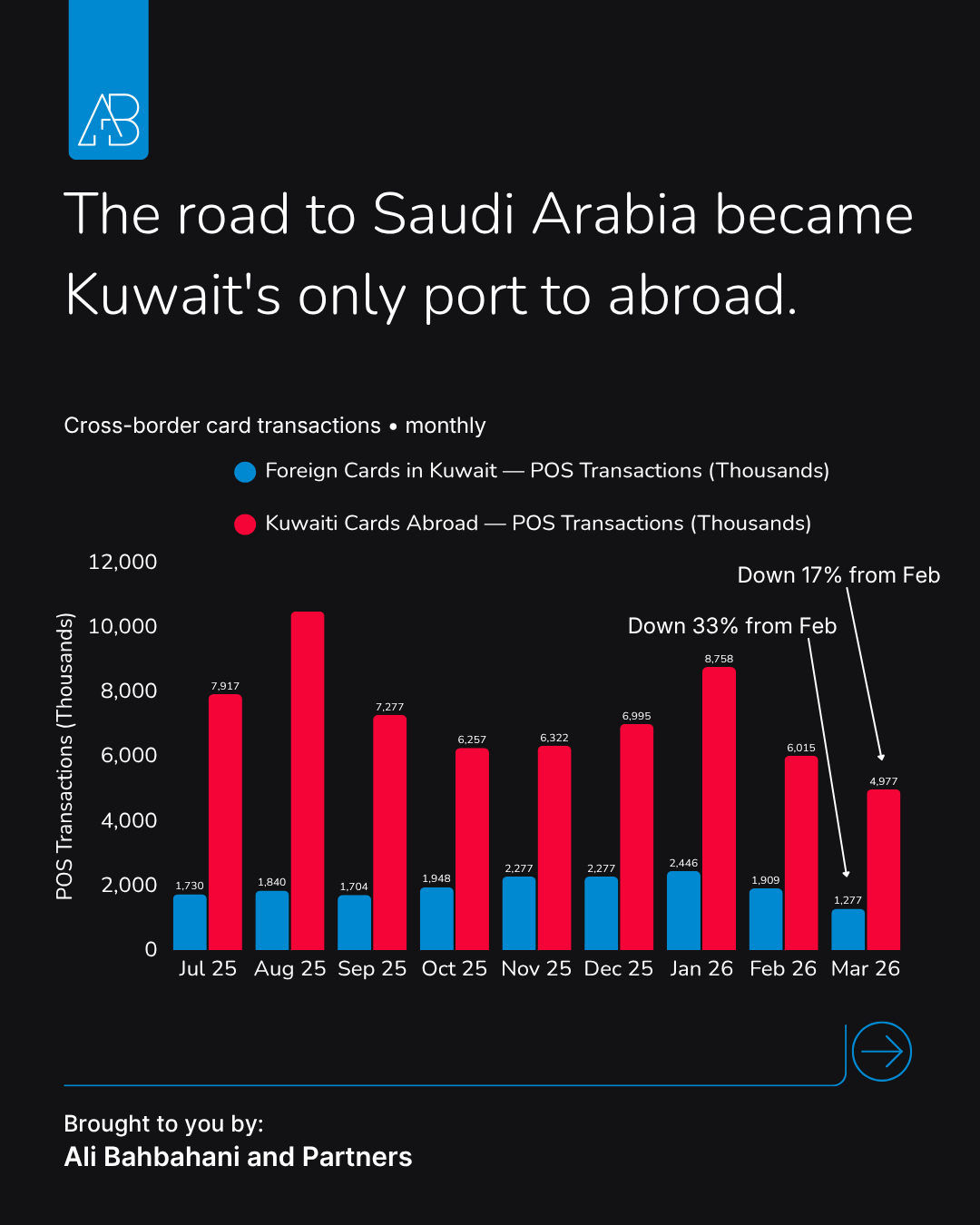

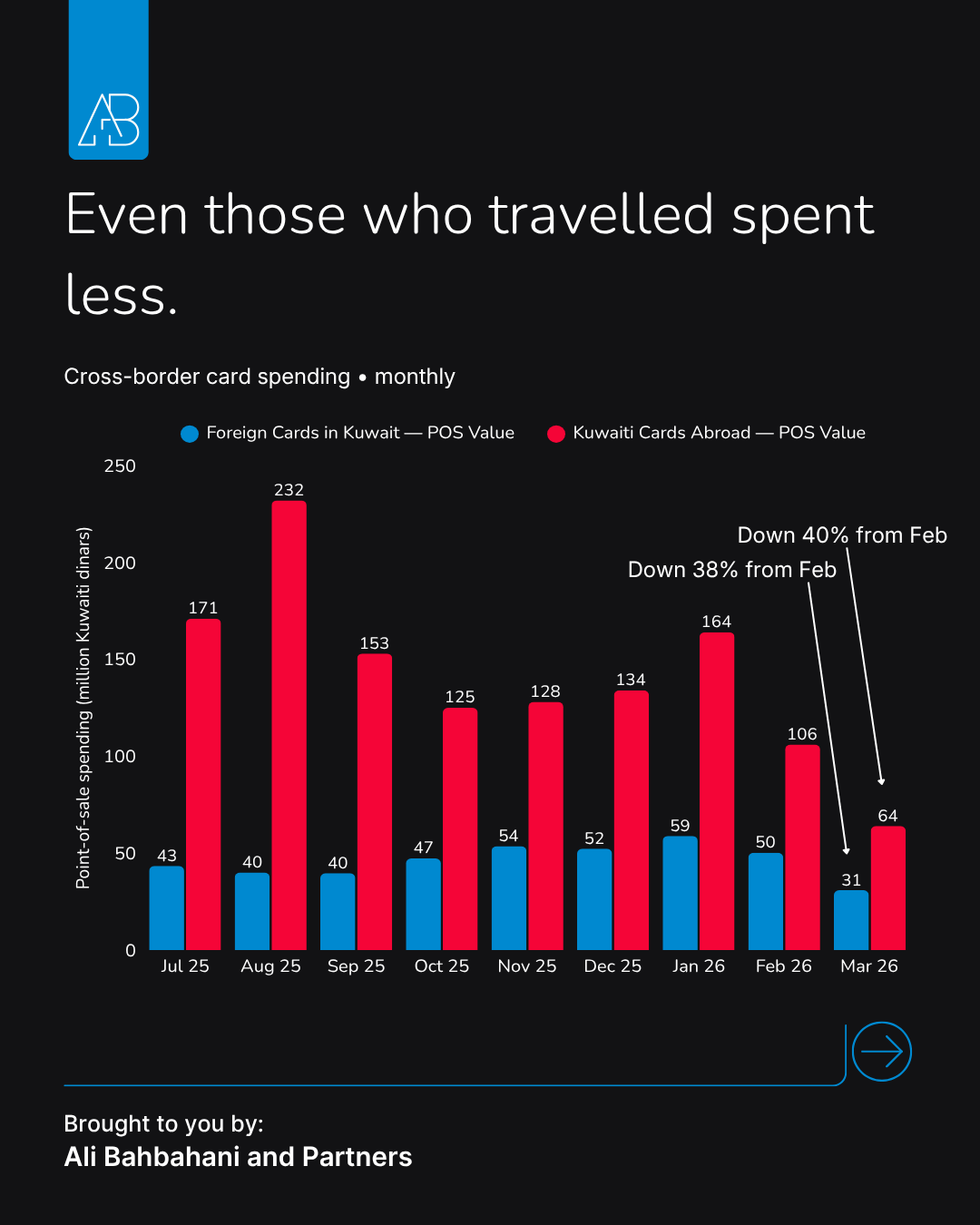

The cross-border numbers are more revealing still. With the airport closed, the only way out of Kuwait was overland through Saudi Arabia. Kuwait Airways relocated its hub to Dammam. Jazeera relocated to both Dammam and Al Qaisumah. Passengers who wanted to fly anywhere had to take an organised bus across the land border, check in at a Saudi airport, and depart from there.

Yet outbound card spending was not zero. Kuwaiti cards used abroad rang up KD 63.5 million in March, against a pre-war six-month average of around KD 158 million. Against the pre-war average, outbound spending was roughly 60 per cent lower. Against February alone, it was down around 40 per cent. The 4.97 million transactions abroad in March represent the friction cost of determined travel. People who needed to leave, left. They drove to Saudi Arabia, flew from Dammam, spent overseas.

Inbound is the mirror image. Foreign cards used inside Kuwait fell to KD 30.9 million, 47 per cent below the pre-war six-month average. With no commercial flights landing, this number captures foreign residents already in Kuwait, plus the small number entering via the Saudi land route, minus those who left in reverse.

There is one more household-level indicator that deserves a section of its own.

The expat community voted with their wallets

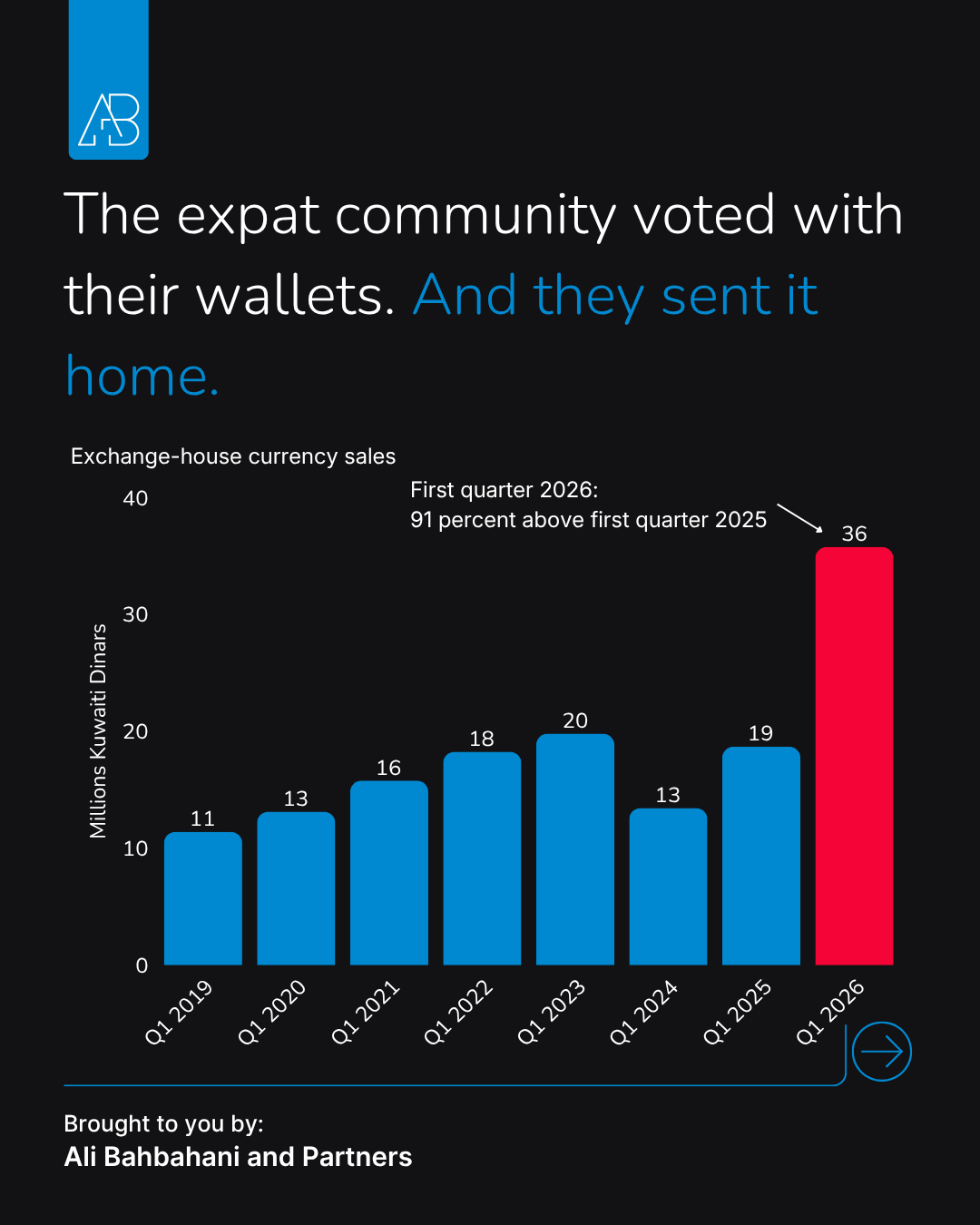

Kuwait has 31 licensed exchange houses, regulated by the Central Bank, that handle the bulk of remittance flows for the country's roughly 3.4 million expatriate residents. Their quarterly aggregated currency sales are reported with a one-quarter lag. The Q1 2026 data, the first quarter that includes March, was published in this release.

The number is striking. Currency sales at the 31 exchange houses reached KD 35.8 million in Q1 2026. That was 91 per cent above Q1 2025 and well above the recent quarterly run rate. Q1 2026 alone exceeded the full year of currency sales in 2019, 2020, 2021 and 2022.

The quarterly timing matters. The data does not isolate March. But given when the shock occurred, it is difficult to read the Q1 jump without seeing March as the month that carried the stress.

The profit figure points in the same direction. Net profit at the 31 exchange companies came in at KD 15.3 million for the quarter, the highest quarterly profit in the series. Roughly half of all of 2025's profit was earned in the first three months of 2026.

The motivation cannot be known from the aggregate data alone. But the behavioural signal is clear. One plausible reading is precautionary remittance acceleration: expatriate households sending money home earlier, or in larger amounts, because uncertainty had risen. Another possible contributor is local hedging demand for foreign currency. Either way, the data shows money moving faster through the exchange-house channel during the quarter that included the March shock.

This may be the cleanest behavioural signal in the release, although the quarterly timing requires caution. We will see whether the Q2 2026 reading, when it publishes in July, returns to the pre-war run rate or whether something has structurally changed in how this community holds and moves its money.

What held

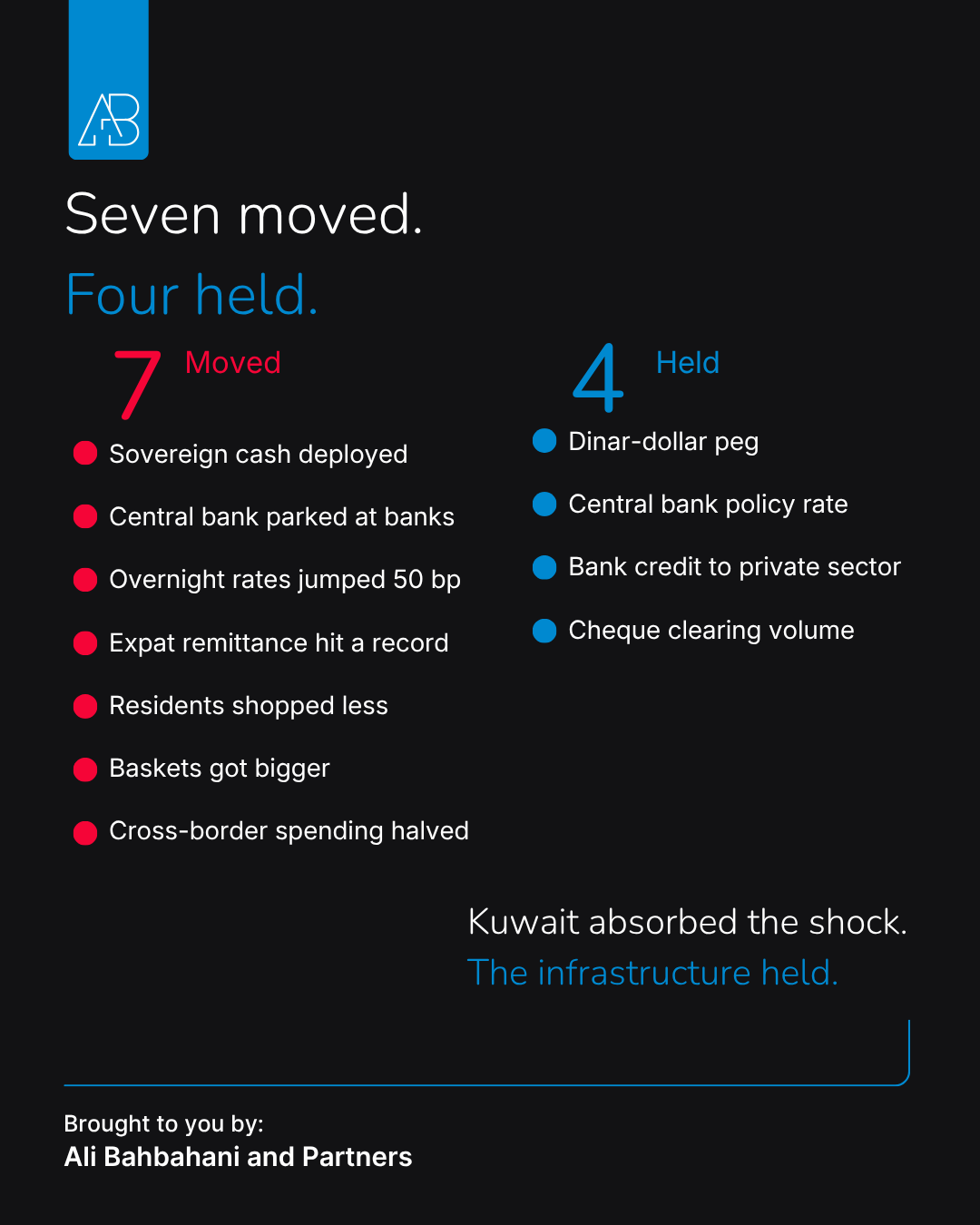

I have just walked through seven separate moves: sovereign cash deployed, central bank cash placed at banks, overnight rates spiked, residents shopped less, basket sizes grew, outbound spending collapsed, and exchange-house flows hit a record. Each of them is the kind of finding that, in a normal month, would lead a research note on its own. In March, all seven happened together.

Now consider what did not move.

The Kuwaiti dinar ended March at 306.95 fils per US dollar. It started the month at 305.30. A 0.5 per cent move within the basket band, well inside normal day-to-day variation. The peg held cleanly through the war. Nothing in the published exchange-rate data suggests visible pressure beyond the normal operating range of the basket regime.

The Central Bank's discount rate held at 3.50 per cent. Despite the overnight liquidity stress, despite the regional pressure on neighbouring central banks, the policy rate was not touched. The signal sent to the market was that the policy stance had not changed, even as the operational tools were being used heavily.

Bank credit to the private sector grew by 0.5 per cent month-on-month. Lending continued. The friction was in the interbank market, not in the customer-facing market. Households borrowed, businesses borrowed, the credit channel did its job.

Cheque clearing volumes were essentially flat. The plumbing of the payments system worked. Cheques cleared, KNET ran, cards swiped, online transfers settled. Anyone living in Kuwait in March will tell you: at no point did the financial system itself feel any different from a normal week, even as everything else was on fire.

These four anchors are the most underrated numbers in the release. Seven things moved, and they moved hard. Four things held, and they held cleanly. The combination is what tells you the system absorbed the shock rather than buckling under it.

What this means for businesses operating in Kuwait

The release gives us one month of monetary and payments data, and one quarter of exchange-house data. The April release, which will publish in late May, will tell us whether March was a single-month spike that mean-reverted as the regional situation stabilised, or whether something has structurally changed in how Kuwaitis hold cash, where expatriates remit, and how cross-border spending behaves.

In the meantime, there are three observations that businesses operating in Kuwait should be thinking about right now.

Card data moved before the official narrative did. It captured the war effect within days, weeks before any official tourism, retail or labour-market statistic will report it. If you operate a business that depends on domestic consumer spending, the basket-size data is your early-warning indicator. If you operate a business that depends on inbound tourism or expatriate workforce stability, the cross-border and remittance data is yours. In a region prone to sudden shocks, the businesses that monitor Central Bank monthly releases as a routine input to operating decisions will react meaningfully faster than those that wait for the front-page newspaper coverage.

State liquidity support is real, but it is not a treasury plan. KD 1.12 billion of public-sector liquidity and KD 175 million of Central Bank balance-sheet were placed inside the banking system in a single month. This is not theoretical capacity. It happened. Anyone running a business in Kuwait whose operations depend on a functioning credit and payments system should take some quiet comfort from that. It is not an unlimited backstop, and it should not be relied on as a substitute for prudent treasury management. But it is real.

Friction can destroy demand faster than marketing can rebuild it. The cross-border spending data shows that, with sufficient friction, outbound consumer demand can be cut by more than half in a single month. The retail, hospitality, leisure and tourism categories that depend on inbound visitor spend, or on Kuwaitis travelling and bringing back foreign-bought goods, are exposed to this in ways that are not always visible during normal periods. Building a business in Kuwait means accepting that the regional environment can compress demand faster than any local marketing strategy can offset. The friction tax, when it is imposed, is paid in days.

A closing note

I started writing this on the assumption that I would walk through the indicators clinically. By the time I got to the end, I realised this is not quite an ordinary research note, because March was not an ordinary month.

Kuwait is small. The expatriate community that remitted at record volumes, the residents who stayed home and consolidated their shopping, the travellers who paid the friction tax to leave, the staff at the exchange houses booking record profits, the people inside the Central Bank making decisions about deposits and discount rates, are all, in the small geometry of this country, no more than two or three degrees of separation from one another. The data in the Central Bank release is also a record of how a country I know well actually behaved, in a month that nobody who lived through it will forget.

The headline finding is that the system held. That is genuinely good news. It is also a finding that is only possible because of decades of careful institutional building, by people who designed a Central Bank, a peg, a payments infrastructure and a sovereign cash management framework that could absorb something like this without breaking. Most of those people are not visible. Most of them never will be. We should notice them anyway.

At Ali Bahbahani & Partners, we help businesses operating in Kuwait understand the structural patterns underneath the headline numbers, and translate Central Bank into operating decisions that hold up across cycles. If the way your business reads regional risk, monitors consumer behaviour, or models stress scenarios needs to be sharpened, we would be glad to help.

The March data showed how the state’s balance sheet absorbs a shock. What that balance sheet carries in ordinary times is a different question — one we have now priced end to end, from birth to 80, in The Kuwaiti Dream, Priced: KD 4.13 million for one modelled household, with the state funding 55%.

Method note: This note uses the Central Bank of Kuwait's March 2026 Monthly Monetary Statistics release, with comparisons to February 2026 and selected historical periods where stated. Card and banking indicators are monthly. Exchange-house currency sales and profit are quarterly, so Q1 2026 should be read as a quarter that includes the March shock, not as a pure March-only figure. "Pre-war average" refers to the six-month average of September 2025 to February 2026 unless otherwise stated. "Five-year" comparisons refer to monthly observations from March 2021 to March 2026.

Source: Central Bank of Kuwait, March 2026 Monthly Monetary Statistical Bulletin. Analysis: Ali Bahbahani & Partners.