Kuwait Traveler Experiences

%25201-min.avif)

.webp)

A visitor's decision to come to Kuwait, to stay longer than they planned, and to come back is made across nine separate moments — from the Google search a year before the trip to the message they send a friend two weeks after they leave. At every one of those moments, the country either earns the visitor or quietly loses them. We have spent two decades losing them at most of the nine.

This article walks the journey from the visitor's perspective, phase by phase. The pattern that runs through every phase is the same one I have argued in everything I have written about Kuwait: the friction is the strategy. Every step where the country has not removed an avoidable obstacle is a step where a visitor decides Bahrain or Doha or Riyadh is easier. The competition we lose to is not the destinations themselves — it is our own willingness to leave small things broken. I've made the broader case for this approach in the Friction Fighters Manifesto.

The good news, and the reason this article runs to nine phases instead of one, is that the fixes are knowable. None of them require a new vision document. They require deciding which broken touchpoints to fix in what order, and then assigning the work.

The Numbers That Frame the Argument

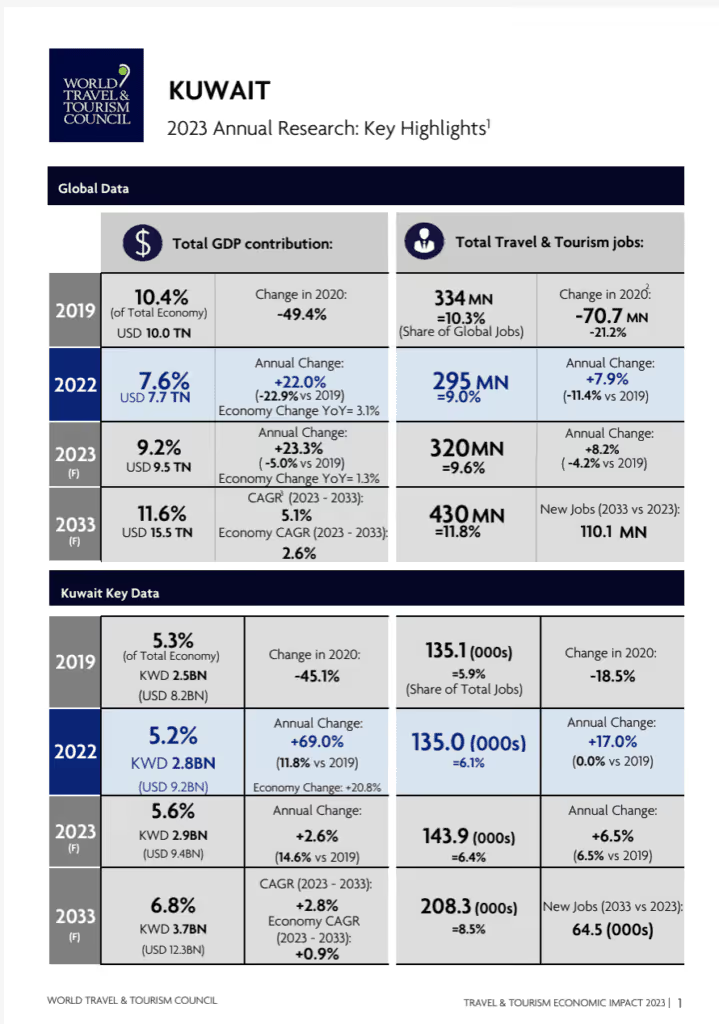

Kuwait International Airport handled 15.72 million passenger movements in 2025, according to the Directorate General of Civil Aviation's official statistics portal. That is up roughly 2% on 2024 and effectively at the pre-pandemic peak the airport set in 2023 at 15.69 million. The flow through the gate is real and growing. The problem is not that nobody is coming to Kuwait. The problem is that of those fifteen-plus million annual passenger movements, only a small fraction are international leisure visitors who chose Kuwait as a destination rather than as a stopover or a work commute.

The hotel sector tells the same split story. Kuwait currently has 13,593 rooms across 136 properties, with occupancy that climbed from roughly 30% in 2024 to 48% in 2025 on the back of better visa accessibility and growing regional interest. Average daily rates rose 16% over the same period. The pipeline through 2028 adds roughly 2,000 keys — a 10% capacity expansion — including the new Mandarin Oriental, the converted JW Marriott, and the Nobu development. The supply is moving. The demand-side question is whether Kuwait can fill those rooms with the kind of visitors who book the journey rather than the kind who already had to be here.

The outbound deficit is the figure that should worry everyone. Kuwait runs a tourism deficit of roughly KD 2.46 billion, driven by Kuwaiti households spending their leisure budget abroad because the domestic offering has not been built at the level the household demands. Redirecting just 20% of that outbound spend back into the local economy would inject KD 1 billion and create an estimated 10,000–12,000 jobs. That is the prize the conversation usually misses. Inbound tourism is the headline number that gets reported. The larger short-term lever is the 3.4 million expatriates and 1.5 million Kuwaitis already in the country who are currently spending their leisure money in Bahrain, Dubai, Beirut, and the Mediterranean. They are the most addressable audience Kuwait has.

The infrastructure investment gap is a smaller story but a real one. The Sheikh Jaber Al-Ahmad Cultural Centre is the cleanest example of the underlying problem: the building was built, the bill was paid, and the programming inside it has never been resourced at the level the venue deserves. A tourism economy that worked would have JACC as a permanent draw, not a venue that fills for a season and goes quiet. The infrastructure exists; the product has not been finished. That gap, repeated across two dozen assets in the country, is what a serious tourism strategy would close first. I have made the same argument from the hotel side in From Empty Tables to Cultural Hubs.

What Today's Visitor Expects

The visitor benchmark is not set by what Kuwait is currently delivering. It is set by what is normal in Singapore, in Dubai, in Doha, increasingly in Riyadh. A visitor arriving in Kuwait in 2026 is comparing the visa flow to Bahrain's, the airport to Doha's, the hotel booking experience to the global standard set by Marriott or Hilton, the food scene to what they have already eaten in Riyadh's new restaurants. The bar is the regional bar, and Kuwait has not chosen to compete at that level yet.

The four expectations that determine whether a destination converts a first visit into a return are well-understood: efficient processes (visa, immigration, transport), digital access (a website that works, an app that loads, search results that return current information), authentic local experience (not a generic luxury template that could be anywhere), and a basic competence around sustainability that no longer feels optional. Kuwait misses on all four today. The rest of this article is the phase-by-phase evidence of where each one breaks.

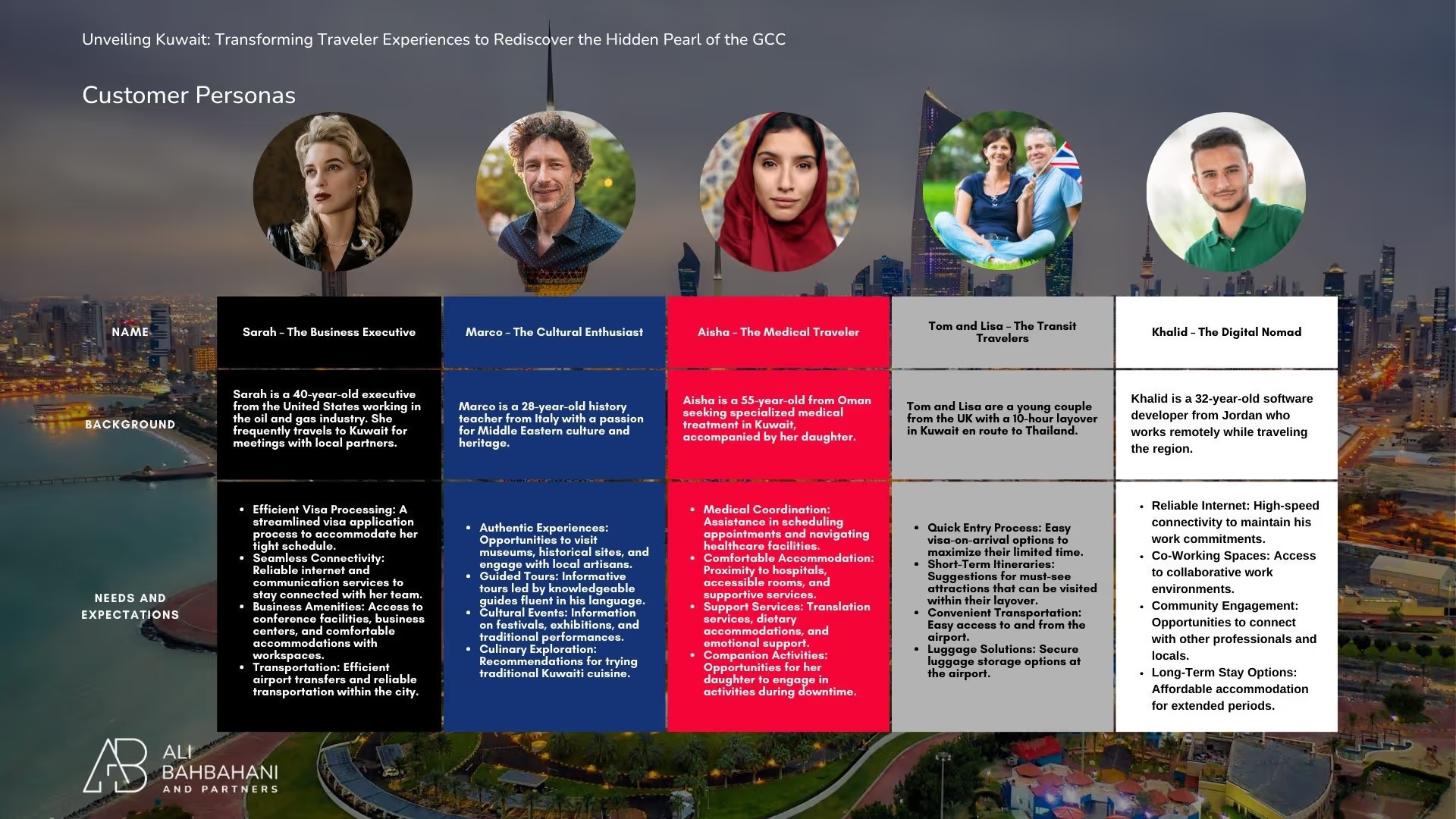

Who Is Actually Visiting Kuwait

A tourism strategy that tries to serve every visitor segment equally serves none of them. Kuwait currently designs around one — the business traveller from a multinational with a meeting in Sharq, who arrives, checks into a hotel near the office, and leaves in three days. That visitor is well-served by the existing system. The other categories, who in aggregate represent the larger commercial opportunity, encounter friction the business traveller never sees because no one designed for them.

The segments that show up in inbound arrivals data and that any serious tourism strategy has to plan around are the following. The order is roughly by current volume; the priority order would look different and is the question that has to be settled before anything else.

Business and corporate travellers. Already served reasonably well, even where execution is uneven.

Friends and family visitors. The category Kuwait under-serves most relative to its actual scale — with 3.4 million expatriate residents, the inbound family-visit traffic is structurally significant and gets almost no dedicated infrastructure.

Medical tourists. Underdeveloped but genuine, especially in specific specialisms with regional reputation.

Transit and stopover travellers. The lowest-effort, highest-volume opportunity, and the one Kuwait has done least with. Dubai built a tourism economy on the back of layovers.

Cultural tourists. Small in number, disproportionately important for word-of-mouth and the long-form travel media that shapes how Kuwait is perceived globally.

Shopping visitors. Real but commoditised across the GCC.

Educational and academic visitors. Small in absolute numbers, valuable in network effects.

Government and diplomatic visitors. Handled well at the protocol level, less well at the experience level.

Sports and event attendees. The Khaleeji Zain tournament showed what Kuwait can do when an event forces coordination; the follow-through afterwards showed what Kuwait still does not do.

Digital nomads and remote workers. A small but growing global category that Kuwait has barely entered.

Adventure and eco-tourists. Kuwait has Boubyan, Failaka, Kubbar, the desert — none of it packaged for the international adventure traveller in the way Oman has packaged Musandam or Saudi has packaged AlUla.

Luxury travellers. The category that should be most visible in Kuwait and is currently least visible. The luxury traveller is the highest-spend, highest-network-effect visitor a destination can attract, and Kuwait's current luxury hotel offering does not match what this traveller now expects internationally.

Cruise passengers. Currently negligible, but the GCC cruise market is one of the clearer growth opportunities in the next decade.

The point of the list is not to write a marketing brief for each. It is to decide which three or four to invest in first, and which to consciously defer.

The Nine Phases

The customer journey runs through nine distinct phases: awareness, research, visa, planning, booking, arrival, experiencing, departure, and post-trip. The friction at each one is the difference between a country that converts visitors into return guests and one that does not. The phases below are the actual sequence a visitor goes through when considering Kuwait today, with the specific platforms, websites, and processes they encounter at each step. The comparisons are with the GCC peer that handles the phase best — sometimes Bahrain, sometimes Qatar, sometimes the UAE — because that is the standard the visitor is unconsciously holding Kuwait against.

Phase 1 — Awareness: Where the Journey Either Starts or Stops

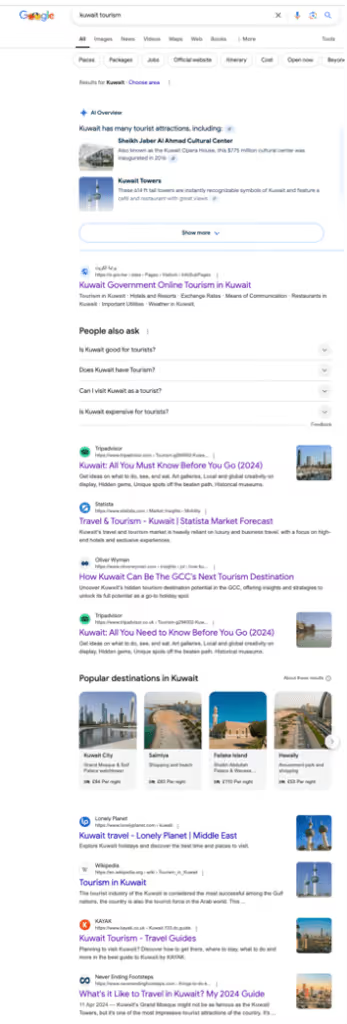

A potential visitor's first encounter with Kuwait in 2026 is almost always a Google search. The visitor types "Kuwait tourism" or some variant of it, scans the first page of results, and decides in under a minute whether the country is worth investigating further. The awareness phase is where most of Kuwait's tourism funnel quietly dies — not from negative perception, but from absence. The country has not invested enough in being findable to be evaluated, which is a different and more solvable problem than being rejected.

Kuwait's official tourism Instagram account, Visit Kuwait, has roughly 57,500 followers as of early 2026. Visit Dubai has 3.1 million. Visit Qatar has 661,000. Experience Oman has built a respectable following on a fraction of Visit Dubai's content budget. The Visit Kuwait account posts mostly in Arabic, with visuals that read as functional rather than designed, and almost no narrative through-line across posts. Visit Dubai works as a benchmark for the opposite reason: it has a point of view, multilingual captions by default, and recurring narrative threads — food, culture, the desert, the skyline — that a visitor can follow over weeks of scrolling and develop a relationship with the brand. Kuwait's account does not yet do that.

Kuwait has no official tourism Facebook presence at all. Visit Saudi has 936,000 followers and uses the platform for the kind of long-form information that performs there: visa rules, travel logistics, cultural calendar. For a meaningful share of the international travel audience — particularly travellers from emerging Asian and African source markets where Facebook is still the dominant travel research platform — not being on it means choosing not to be seen.

YouTube tells the same story. Visit Qatar's channel has 245,000 subscribers and a serious library of well-produced content. Kuwait has no official channel. The Kuwait content that does exist on YouTube is created by independent travellers, and without an official channel to balance the impression, those independent videos are what a researching visitor encounters first.

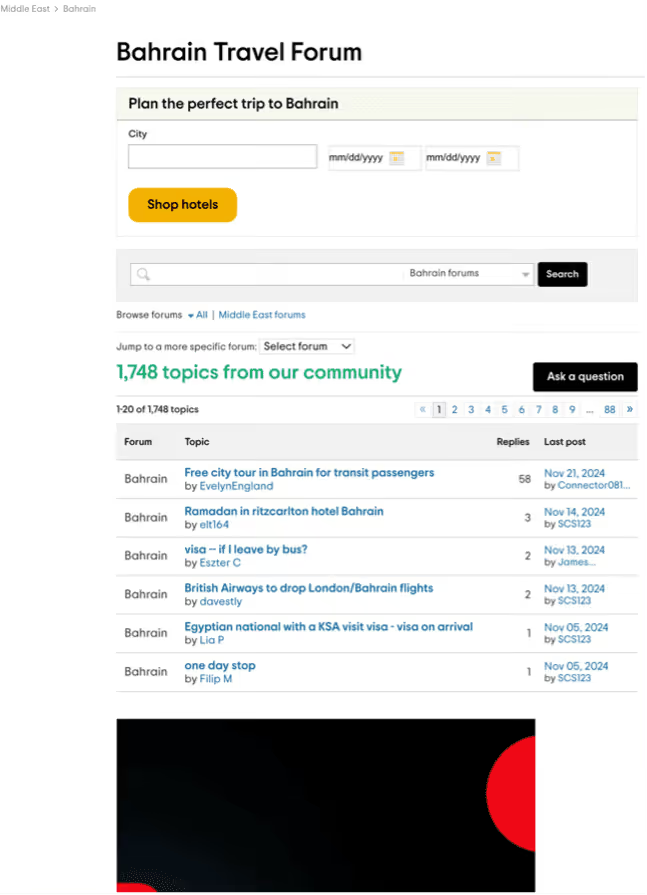

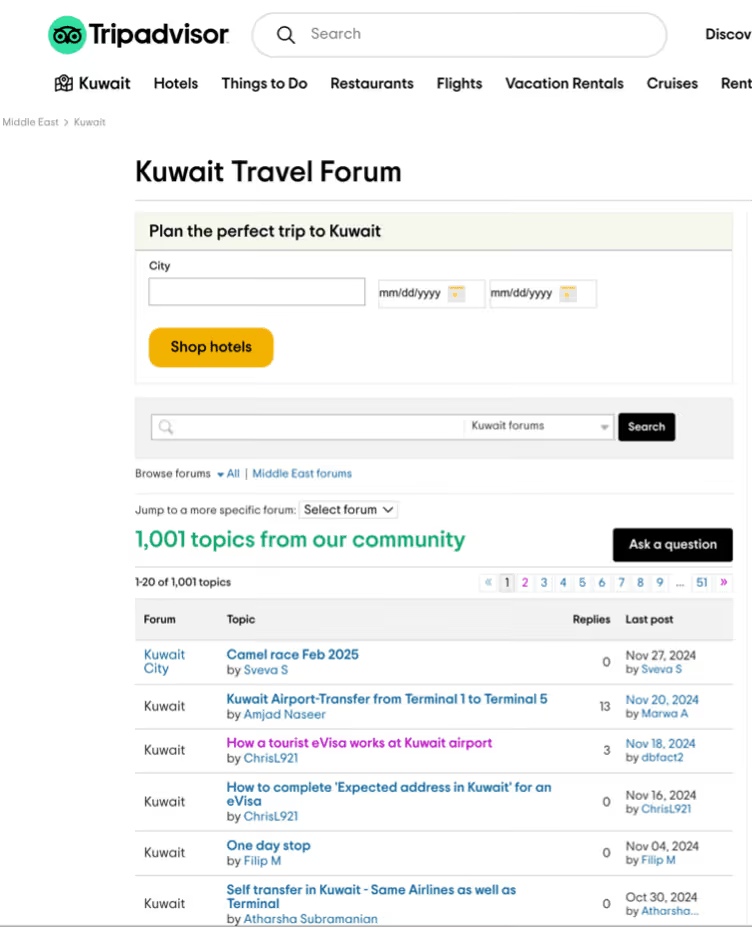

The TripAdvisor data is the cleanest quantitative gap. Kuwait's TripAdvisor forum carries roughly 1,001 topics — a respectable raw count, but dominated by visa and airport logistics rather than leisure tourism, which is the cleaner signal of how the destination is actually being researched. Bahrain's forum carries about 1,748 topics across a much broader leisure mix: cultural festivals, heritage sites, weekend getaways, transit-passenger city tours. Dubai, Qatar, Saudi Arabia, and Oman all show similar leisure-weighted patterns. The volume is comparable; the composition is what differs — Kuwait's forum is procedural where the others are aspirational.

The travel media gap is the most painful one because it is the most directly tied to commercial outcomes. Condé Nast Traveler has published 65 articles on Oman, 29 on Bahrain, and 21 on Kuwait. The Tareq Rajab Museum, which by any honest measure is a world-class private collection, gets a paragraph in most major guides and almost no editorial coverage. The Grand Mosque gets a photograph and a caption. The editorial volume follows the cultural-tourism listings, the listings follow the political will, and Kuwait has not done the work at either end. I have argued the same point about Failaka and UNESCO in Why Kuwait Needs UNESCO World Heritage Sites.

The independent travel-blog universe is harder to fix than any of the above because the operators do not work for us. Some of the most-shared blog pieces on Kuwait describe the country in terms that have stuck in search rankings for years. These pieces were written by travellers with a particular set of expectations that Kuwait did not meet, and the country has not produced enough counter-content to push them down the page. The fix is not to argue with the bloggers. The fix is to publish so much better, more specific, more vivid Kuwait content that the search engine has a better answer to offer.

The instinct of most tourism boards facing this is to commission a campaign — a hashtag, a hero film, a flight of out-of-home in the major source markets. That is the wrong first move. The first move is to fix the inventory of owned content so that when the campaign drives the visitor to a search bar, there is something credible for them to find. A serious Instagram presence with bilingual captions and an actual content calendar. A Facebook page that should have launched five years ago. A YouTube channel with twenty to thirty pieces of well-produced content in its first year. Kuwait's strongest single asset on the influencer side is @hello965, a Kuwaiti creator whose travel content has the precise tone the country should have been investing in nationally for the last five years. I covered the influencer dynamic in more depth in the Skift Megatrends response — the playbook is not complicated, and nobody is running it nationally.

The owned-content gap can be closed in twelve months by a competent team with a working budget. The earned-media gap, built on direct relationships with named editors at Condé Nast, Travel + Leisure, and the New York Times travel section, takes eighteen to twenty-four months. The perception correction in the independent-blog universe is a three-to-five-year arc but begins to move within the first year if the work starts. Kuwait has been talking about closing this gap since the early 2010s. The cost of waiting another year is now higher than the cost of starting.

Phase 2 — Research: The Funnel Narrows Fast

A visitor who decided Kuwait might be worth a closer look now enters the research phase with a list of questions: what is there to do, where to stay, what the visa requires, whether the country is set up for the kind of trip they have in mind. This is the phase where Kuwait loses most of the visitors it managed to interest at all.

The default starting point is the official tourism website. For most GCC destinations that means Visit Saudi, Visit Qatar, Visit Dubai, Experience Oman, or Visit Bahrain — modern, well-funded, image-rich sites with planning tools, booking integrations, and content in multiple languages, all built around the assumption that a confused visitor arrives, finds what they need in thirty seconds, and leaves with confidence about the next step.

Kuwait's equivalent is the Kuwait Government Online Tourism page. It is text-heavy, visually dated, and structured around the assumption that the visitor already knows what they are looking for and just needs to confirm a fact. The navigation is built for bureaucratic information retrieval, not travel inspiration. There is no narrative content, almost no high-quality photography, no embedded planning tools. A first-time visitor lands there, scrolls for ten seconds, and leaves. The site has not been seriously rebuilt in over half a decade. The contrast with Visit Bahrain is the most useful one because Bahrain is the smallest of the Gulf tourism boards and still found the resources to build something that works. There is nothing about Bahrain's tourism budget that Kuwait cannot match — the gap is one of decision-making, not capability.

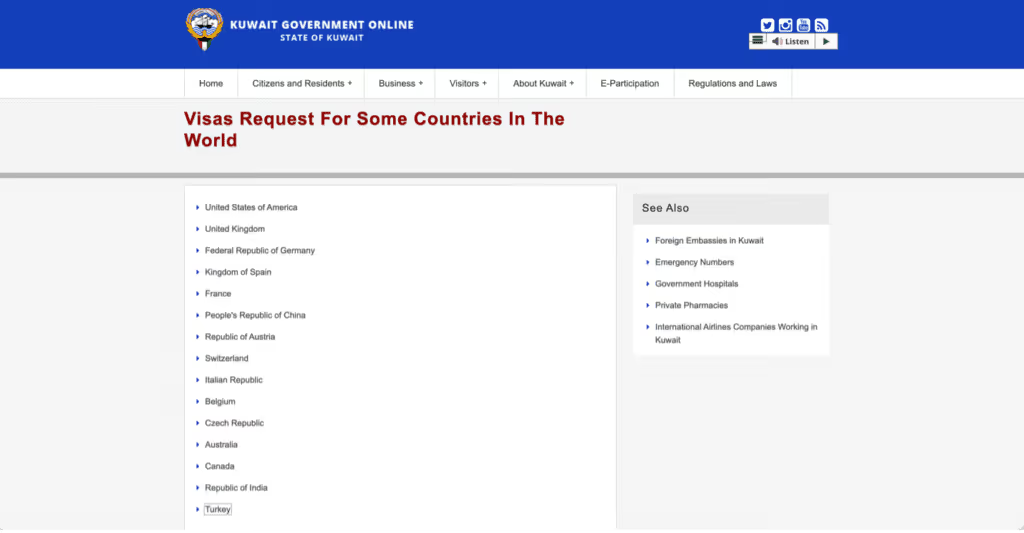

Kuwait's e-Visa page is the second touchpoint and the second failure. The page provides limited information and frequently redirects the visitor to embassy websites for nationality-specific details. There is no consolidated, plain-language explanation of who is eligible, what documents are required, what the fees are, or how long processing takes. A visitor landing on it for the first time leaves with more uncertainty than they arrived with. Bahrain's eVisa portal is the regional benchmark — eligibility check in five seconds, fully online application, real-time tracking, multilingual, transparent processing times. The whole experience is built on the assumption that the visitor's time is worth something. Kuwait's flow is built on the opposite assumption.

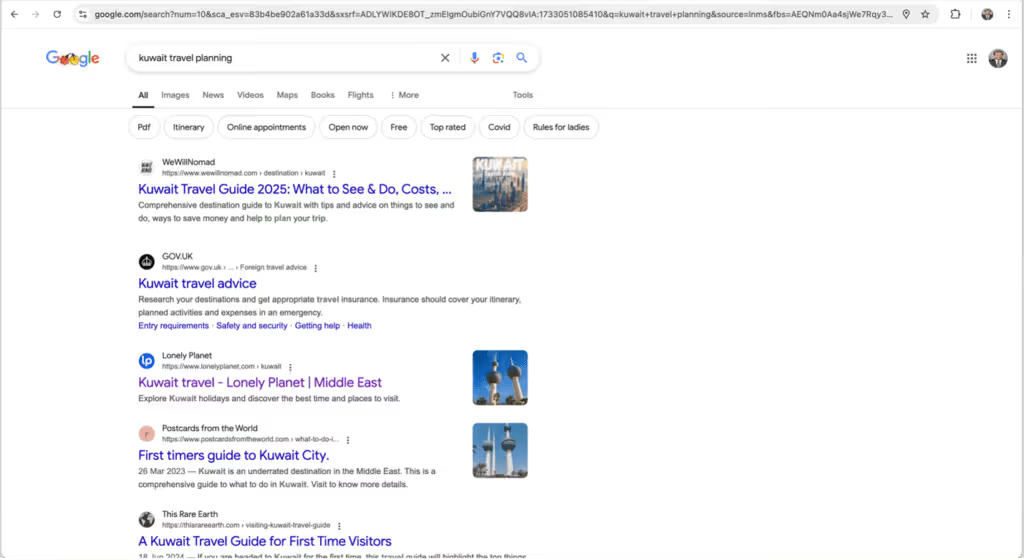

A Google search for "Kuwait tourism" returns the outdated official page as the top organic result. An Arabic search for "السياحة في الكويت" returns the same. There is no official mobile app on iOS. The Android options are limited and not maintained by the government. For visitors who do most of their research on a phone — the majority of the inbound audience — Kuwait is functionally invisible on mobile. A visitor searching "Kuwait travel planning" finds no official tool that builds an itinerary, suggests an order of visits, or links to bookable experiences. A visitor searching "Qatar travel planning" lands on Visit Qatar as the first sponsored result, with an interactive planner, suggested itineraries, and direct links to booking partners.

The fix at this phase is more concrete than at the awareness phase because the deliverables are well-defined. Kuwait needs a single, modern, multilingual tourism website that does five things well: present a clear value proposition for visiting the country, provide accurate visa information including an online application option for every eligible nationality, embed planning tools that let the visitor build an itinerary and book against it, host editorial content with English-Arabic parity in quality, and integrate with the social channels covered in the awareness phase. The visa portal is the single highest-leverage subcomponent — rebuilding it to the Bahrain standard takes six to nine months and a small team, and it has been sitting on the do-list for years.

Phase 3 — Visa: The Decision Point Most Visitors Drop At

The visa phase is where the largest single share of potential visitors abandons the trip. Not because they were rejected — most of them never apply. They drop out because the process is opaque enough that the easier choice is to go somewhere else.

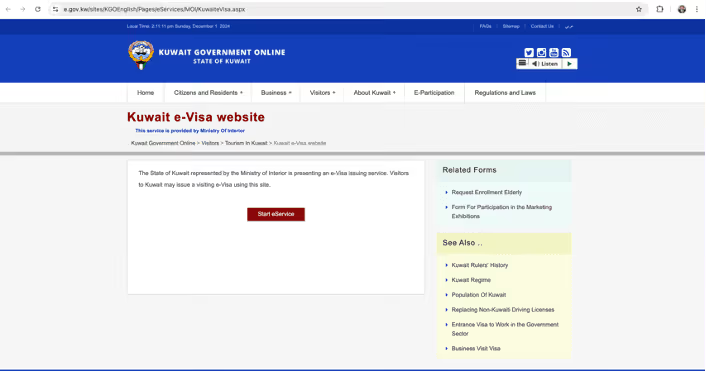

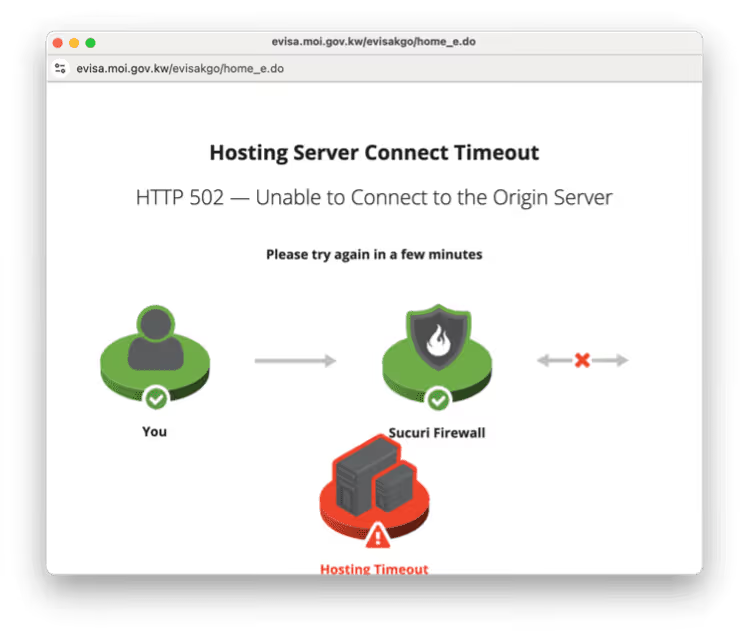

The Kuwait eVisa website's first impression in 2026 is, often, an HTTP 502 error. The page does not load reliably during peak hours. When it does load, the interface is outdated, the navigation is non-intuitive, and there is no clear step-by-step guidance for the applicant. The page does not consistently offer an online application path for all eligible nationalities, redirecting some visitors to embassy procedures with the lengthy paperwork and waiting times those involve. There is no real-time status tracking. There is no clear English-language guidance for international applicants. The page communicates, in everything it does, that the applicant's time and confidence do not matter to it.

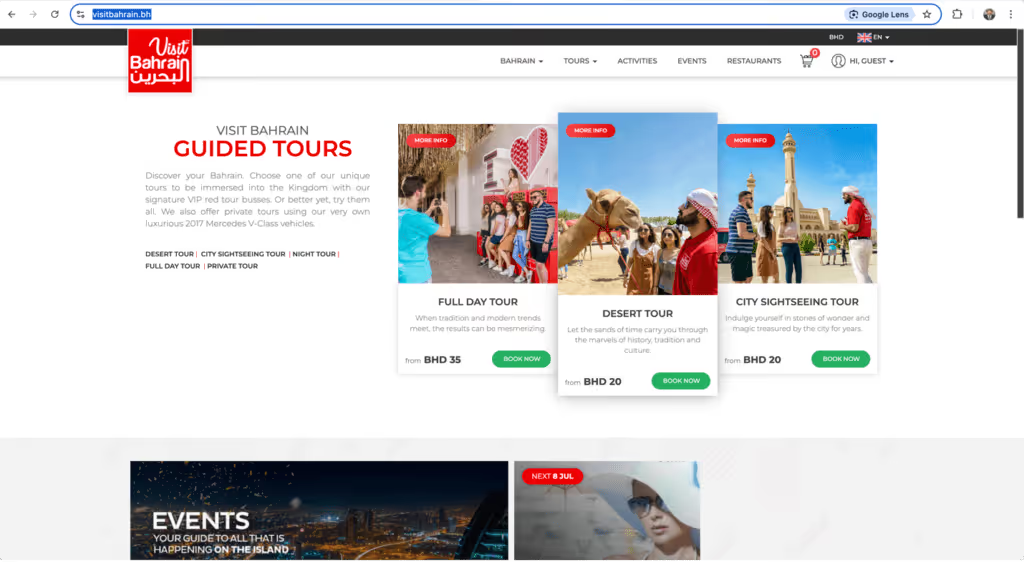

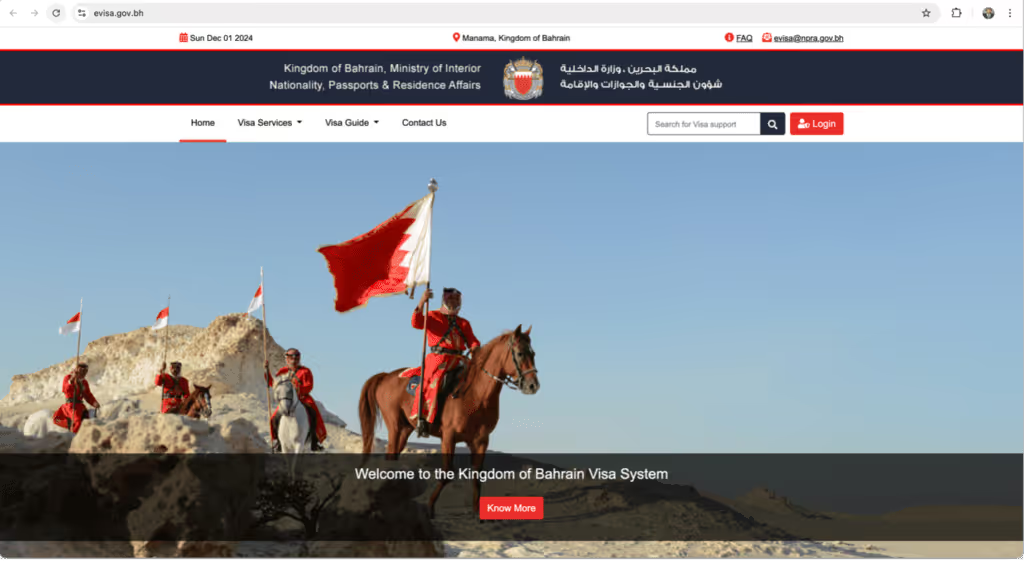

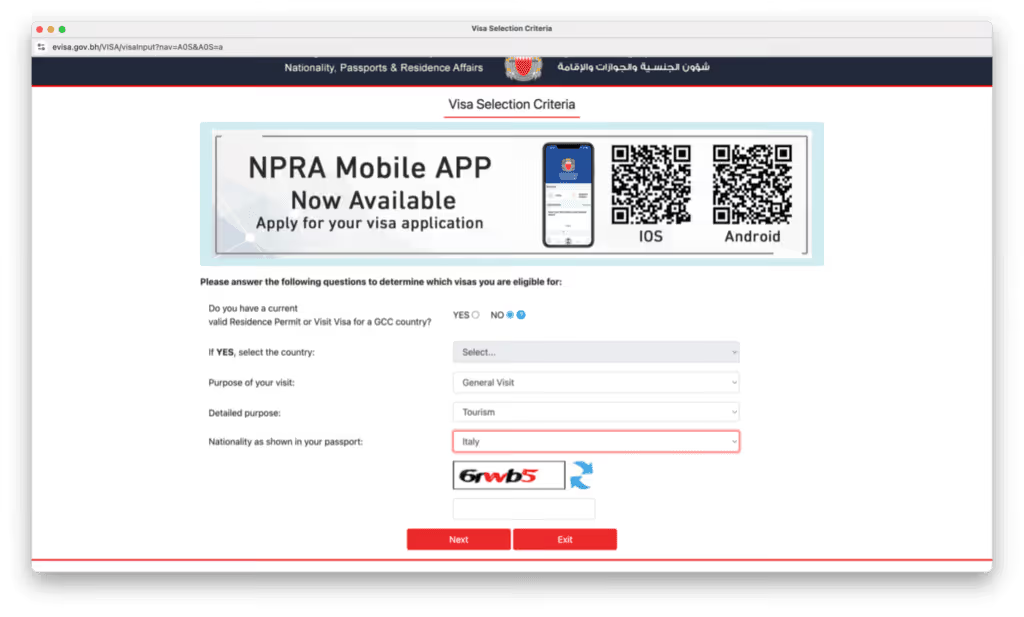

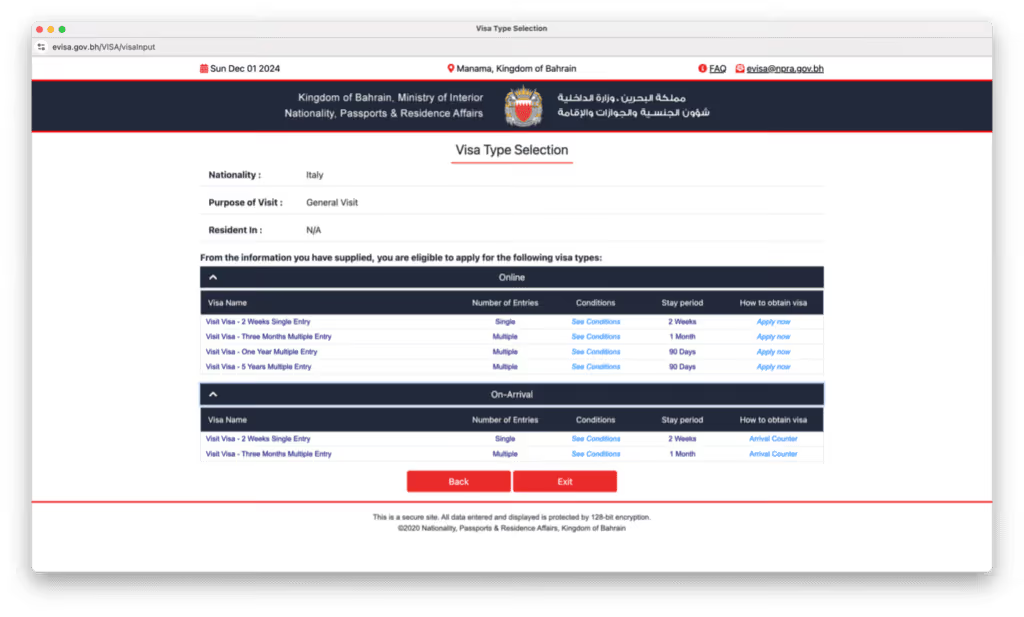

The Bahrain eVisa portal is the benchmark not because Bahrain spent more, but because Bahrain made the design choice to treat the visa as a product. The portal operates without technical errors. The visitor selects from precise visa categories with clear conditions, durations, and instructions. The interactive eligibility check tells the applicant in seconds what visa they need based on nationality and purpose. The design is modern, mobile-responsive, and multilingual. Documents and payments submit online. Processing times are clearly stated, with an expedited option when needed.

The fix here is the most concrete of any phase in the article. Rebuild the eVisa site to the Bahrain standard: reliable infrastructure, modern user-centric design, plain-language visa categories with eligibility checks, full online application with real-time tracking, multilingual support with English as a non-negotiable, and accessible customer support across live chat, email, and helpline. The application process needs to live entirely online for every eligible nationality. Travel-industry integrations with airlines and OTAs should surface accurate visa information at the point of booking, not after. A six-to-nine-month rebuild, run by a competent vendor with a working brief, fixes the single highest-leverage friction point in the entire visitor journey.

Phase 4 — Planning: Where the Visitor Builds the Trip

A visitor who pushed through the visa phase now starts building the actual trip. They are choosing accommodation, picking activities, working out logistics. This is the phase where the country's lack of curated, bookable, well-reviewed offerings shows up most clearly.

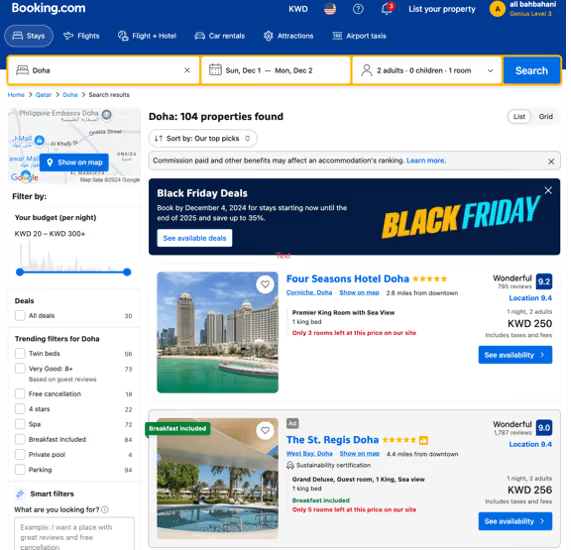

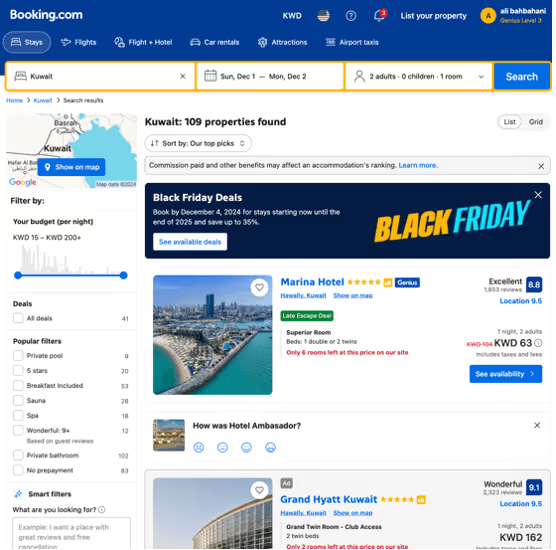

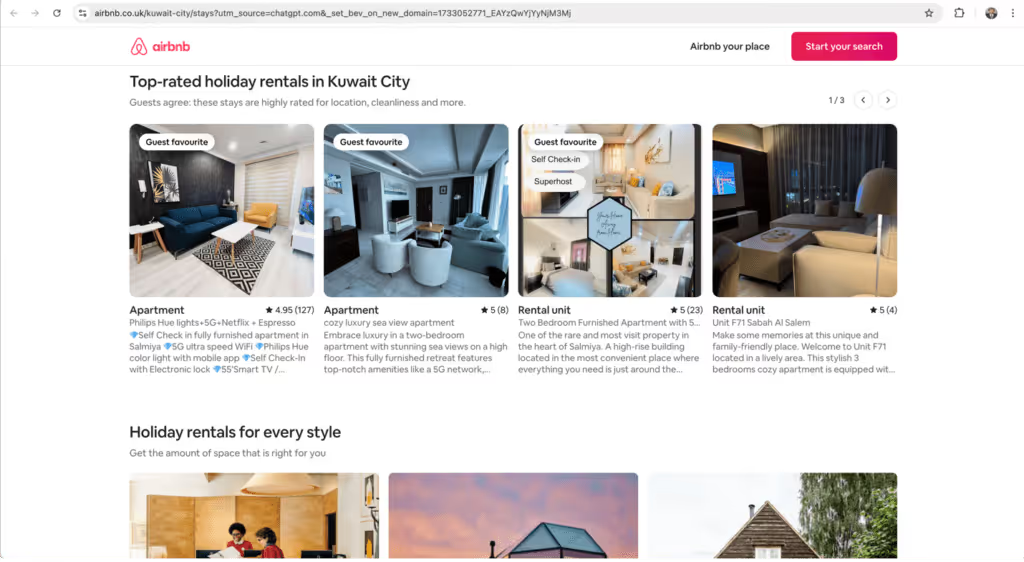

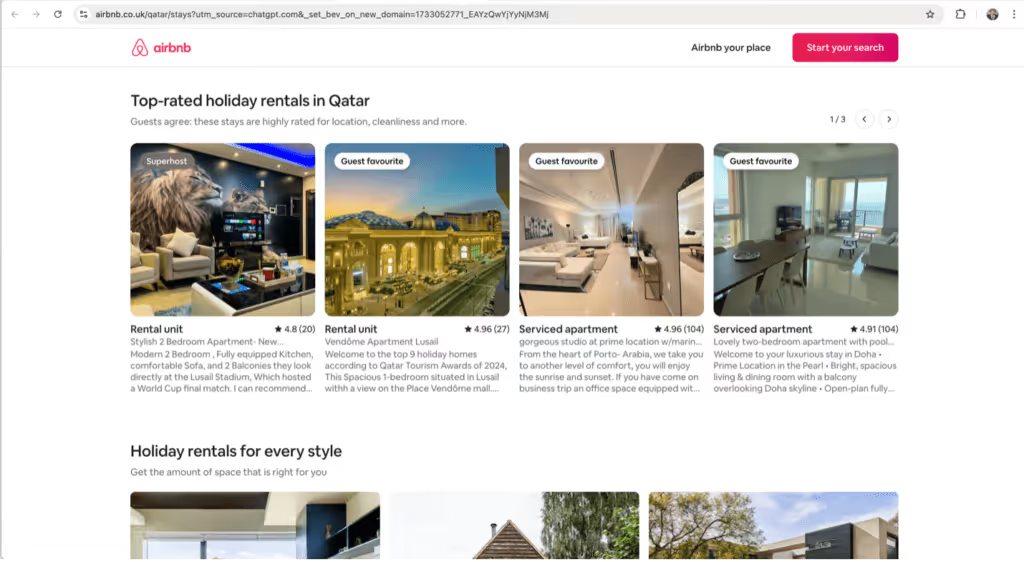

On accommodation, the available options on Booking.com, Expedia, and Airbnb in Kuwait skew toward five-star international hotels and a thinner mid-market layer averaging $96–$106 per night for 3- and 4-star properties. The list is functional but undifferentiated — modern apartments and chain hotels, with very few traditional or culturally distinctive lodgings. Many properties have limited reviews, which makes the visitor hesitate. Qatar's equivalent list is more diverse: boutique hotels, culturally themed properties, a stronger mid-market layer at $55–$74 per night, and far more numerous and positive reviews. Qatar made specific bets on differentiated accommodation product over the last decade. Kuwait did not.

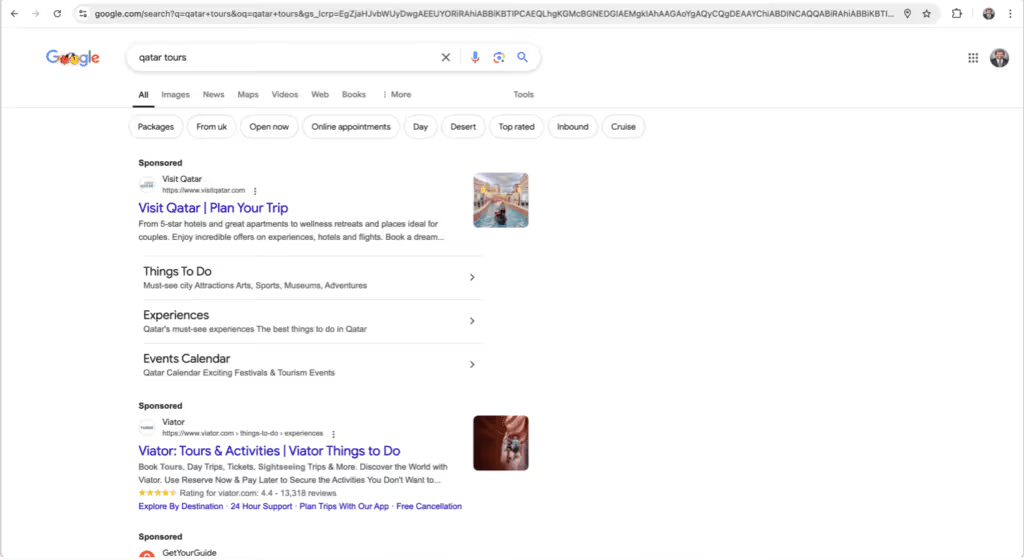

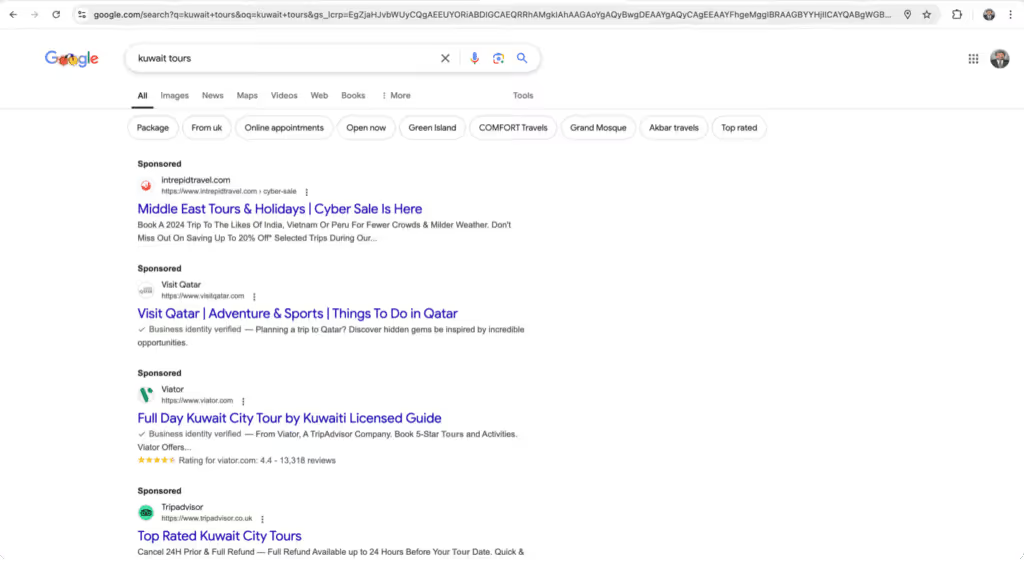

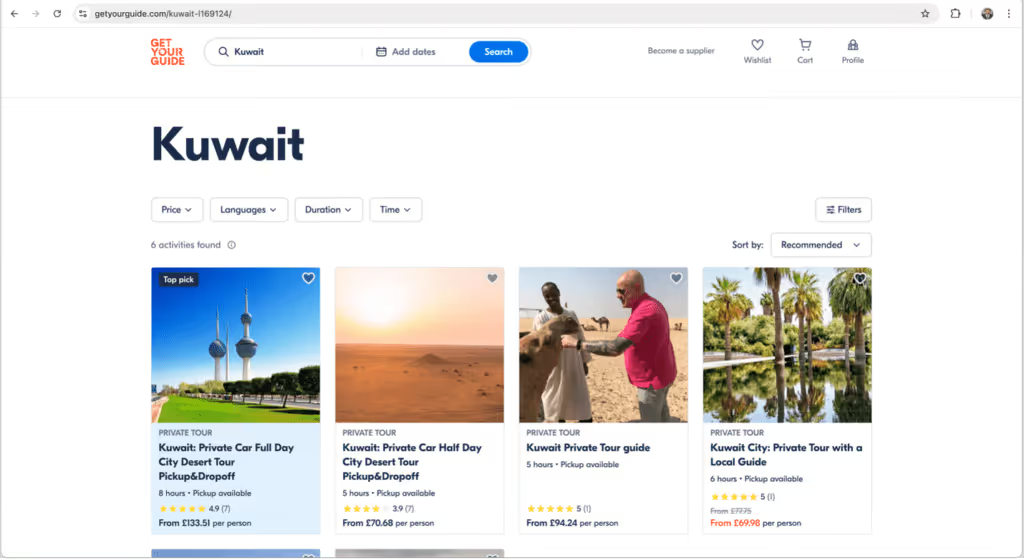

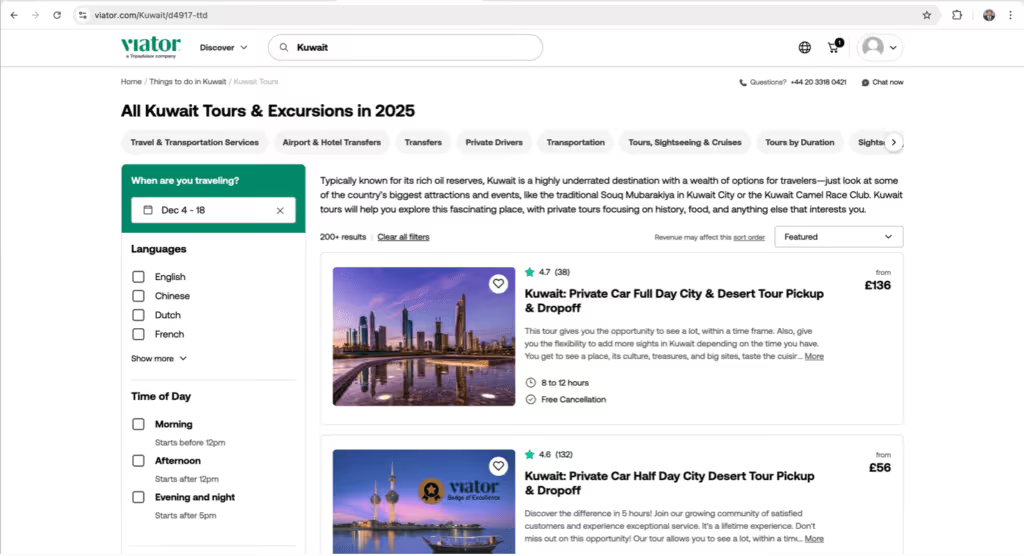

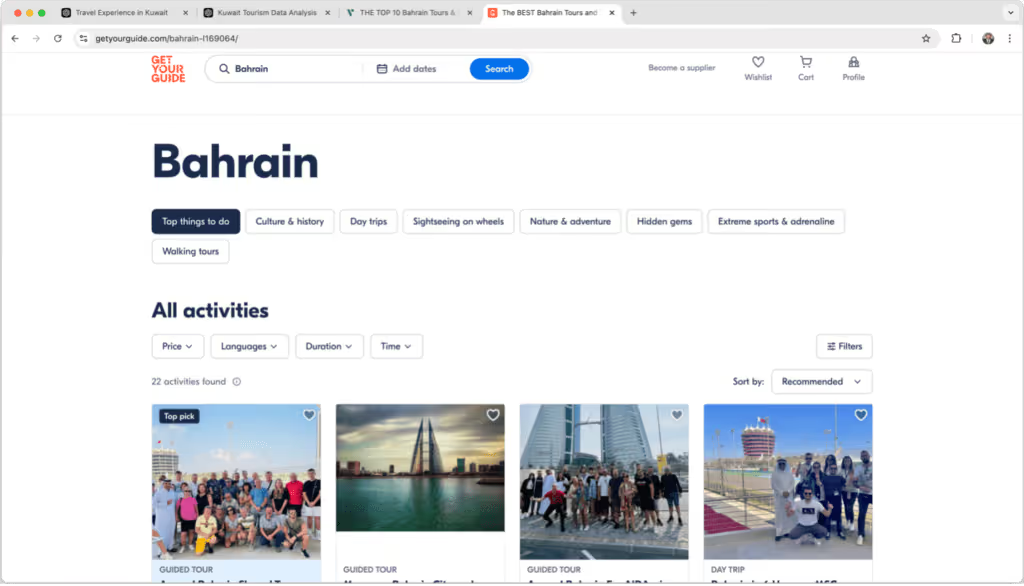

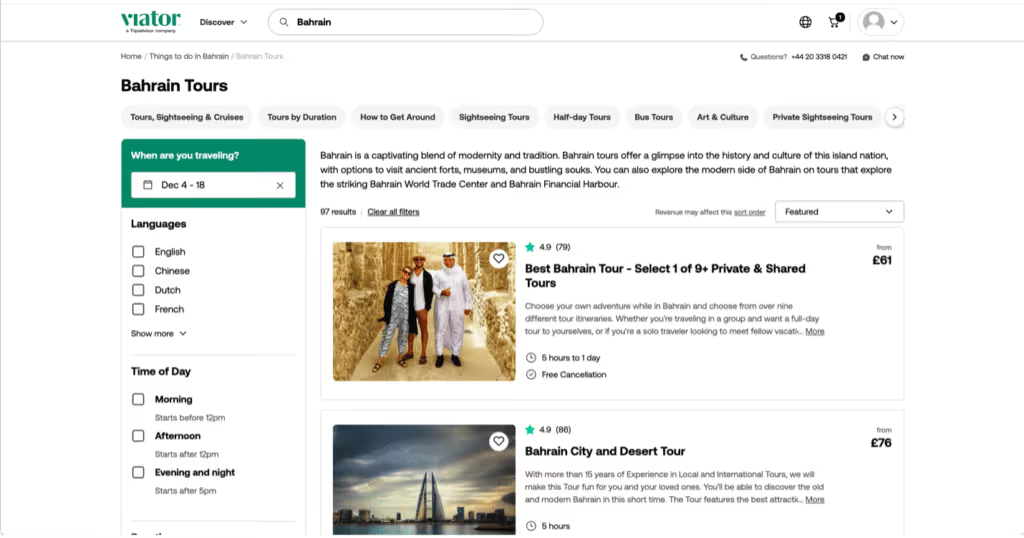

On tours and activities, a Google search for "Kuwait tours" returns no official government-backed initiative or comprehensive tour listing. The most prominent result is often a sponsored Visit Qatar placement. Qatar's Discover Qatar platform offers detailed tours, excursions, and activities for every visitor interest, with easy online booking and clear descriptions. Kuwait has no equivalent. The third-party platforms reflect the same gap — GetYourGuide and Viator carry a small selection of Kuwait city tours and desert excursions with thin reviews, while Bahrain's pages on the same platforms carry a diverse, well-reviewed range including cultural experiences and cruise-passenger excursions.

Transportation planning is the third friction. Kuwait does not host the global ride-hailing services most international visitors are familiar with, though local services like Ride Rove and Careem cover the same function. The public bus system exists but lacks the tourist-friendly information layer — clear routes, schedules, multilingual signage — that makes a visitor confident enough to use it. Bahrain runs Uber, has a more legible public-transport experience, and the visitor's anxiety about getting around drops accordingly.

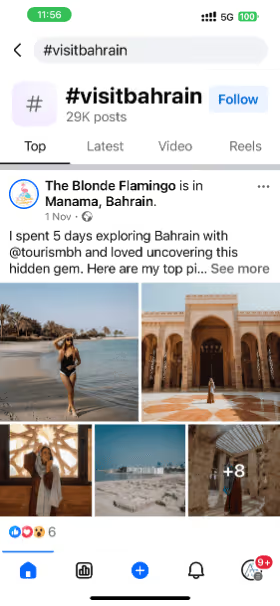

The digital content side compounds the planning problem. Travel blogs and vlogs about Kuwait are sparse compared to neighbouring destinations. The hashtag #visitkuwait has roughly 4,300 posts on Facebook; #visitbahrain has around 29,000. A visitor researching Kuwait finds it difficult to visualise the experience, because most of the visualisation that exists on the internet is from non-tourism sources.

The fix is an integrated tourism platform that does three things: lists curated, accredited tour operators with detailed offerings; lets the visitor book accommodation, activities, and transport in one place; and supports the experience with content created by Kuwaiti and visiting creators alike. Promoting culturally distinctive accommodation — traditional guesthouses, restored heritage properties, properties that lean into Kuwaiti craft and cuisine — is the single largest accommodation-side opportunity, and it is the opportunity the country's hotel development pipeline has largely ignored. I made the same argument from the hotel side in the Kuwait Hotel Industry 2025 analysis.

Phase 5 — Booking: Where Intent Becomes Commitment

The booking phase is where the visitor's intent solidifies into a confirmed trip. Any obstacle at this phase costs the country a visitor who had already done the hard part of deciding to come.

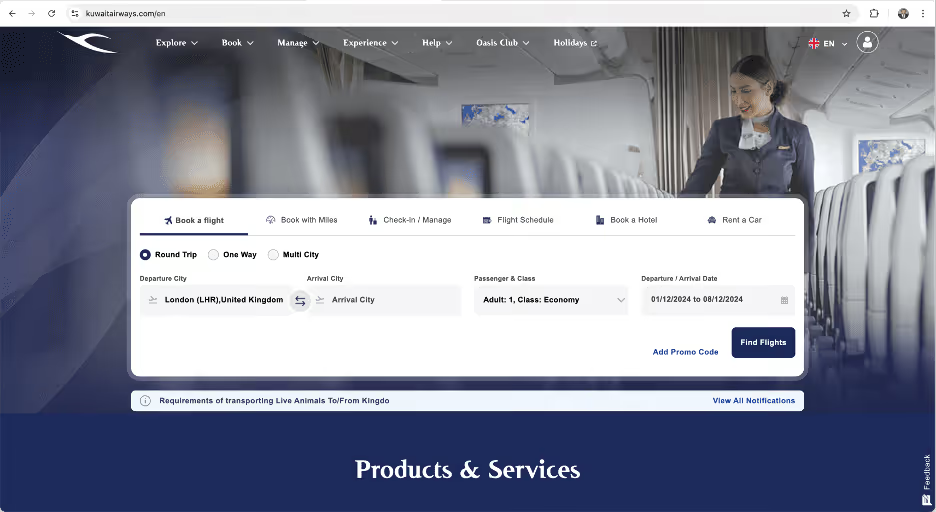

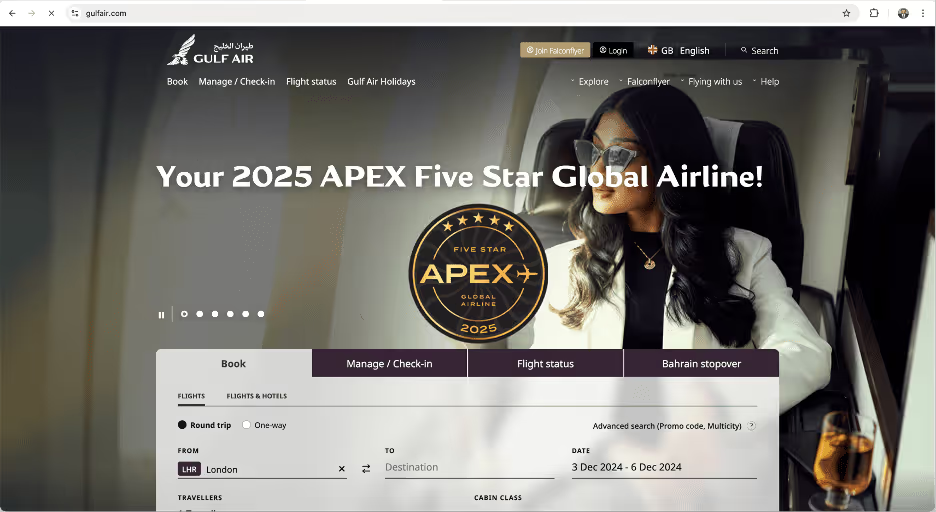

The flight access into Kuwait is workable. Kuwait Airways operates direct flights from major European cities on selected days, and connecting flights through Frankfurt, Munich, Istanbul, and Dubai cover the rest. The frequency is lower than to Bahrain on certain routes (Gulf Air runs multiple direct weekly flights from Rome to Bahrain on equivalent fares), but the access exists. Most visitors will not find this phase a deal-breaker on flights.

The hotel booking experience surfaces more friction. The major platforms — Booking.com, Hotels.com, Airbnb — list Kuwait accommodation primarily in Kuwait City and Salmiya, with a heavier weighting toward luxury and serviced apartments and a thinner mid-market layer. The user reviews are sparser than for comparable Bahrain or Qatar properties, which costs the visitor confidence. Bahrain's equivalent listings span a wider range, supported by extensive reviews and ratings that let the visitor make a confident choice.

The tour and activity booking is the weakest sub-phase. GetYourGuide and Viator list a limited selection of Kuwait private city tours and desert excursions, with thin reviews and sometimes incomplete descriptions. Bahrain's pages on the same platforms list a diverse set with detailed itineraries, numerous reviews, and flexible booking options. The Bahrain tourism authority worked actively to populate the listings; Kuwait has not.

The technical experience is the smaller but more annoying friction. Some Kuwait-based hotel websites and local tour operators run outdated infrastructure with slow loading times, non-responsive design on mobile, and limited payment options. International credit card acceptance is uneven; secure payment gateways like PayPal are not universally supported. Instant booking confirmation is not the norm, with some properties requiring manual approval. Bahrain's booking platforms are generally more advanced — fast, mobile-responsive, multilingual, with secure payment options and immediate confirmation.

The fix is a coordinated upgrade across the platforms Kuwaiti tourism operators use. Modernise the websites of local hotels and tour operators with mobile-responsive design and fast loading. Integrate internationally recognised secure payment systems including PayPal and major card networks across all currencies. Encourage every Kuwait-based operator to list their services on the major global booking platforms with comprehensive information, high-quality images, and prompt communication. Display all pricing transparently, including taxes and fees, and provide clear cancellation and refund policies. Implement instant booking confirmation. Offer multilingual customer support across the entire booking flow. None of this is novel work — the rest of the region has already done it. I covered the same dynamic from the airline side in our GCC airline booking review.

Phase 6 — Arrival: First Impressions at Kuwait's Gateway

A visitor who has booked the trip lands at Kuwait International Airport, and the next ninety minutes either reinforce or undermine everything the country has invested in attracting them. The arrival phase sets the tone for the entire stay.

Immigration processing at peak hours sees longer queues than the airport's current capacity is designed for. With 15.72 million passenger movements per year flowing through the existing terminals, multiple international flights arriving simultaneously can extend wait times noticeably, which is fatiguing for visitors at the end of a long journey. The airport is investing in this — the new mega-terminal under construction will materially change the experience once operational — but the current state is what visitors experience today.

Language accessibility at immigration and at the airport more broadly is uneven. English proficiency among airport staff varies; multilingual signage is present but not comprehensive. For an international visitor without Arabic, the experience is workable but rarely smooth. The benchmark airports in the region — Doha, Dubai, Bahrain, increasingly Riyadh — invest heavily in language training and multilingual signage as a first-line product feature, not a courtesy.

Ground transportation from the airport works but is not legibly presented. Airport taxis are available immediately outside the terminal with a roughly twenty-minute journey to Kuwait City, but fares are not always meter-based and require negotiation. Ride-hailing apps including Careem and Ride Rove offer a more transparent alternative. The public bus system run by Kuwait Public Transport Company connects the airport to the city, but route and schedule information is not prominently displayed in English. A first-time visitor without local guidance defaults to whichever option is most visible, which is rarely the most efficient one.

Tourist information at the airport is the weakest specific gap. There are no dedicated tourist information desks or kiosks in the arrivals area. Online resources exist but require prior knowledge and internet access that the visitor may not have on arrival. A visitor expecting to pick up a map, ask a question, or get a recommendation finds nothing. Every comparable international airport — Doha, Dubai, even smaller airports across Europe and Asia — staffs an arrivals information desk because the moment of arrival is when the visitor is most receptive to a recommendation that shapes the next seventy-two hours.

Road conditions on the route into Kuwait City are functional but uneven. Kuwait's road quality has been rated below the world average in international comparisons, and a visitor noticing potholes or uneven surfaces on the way from the airport forms an impression that is hard to undo with later positive experiences.

The fix is a coordinated arrival programme. Accelerate the completion of the new terminal to relieve current congestion. Optimise space usage in the existing terminal in the interim. Expand multilingual signage and invest in language training for front-line airport staff. Establish a tourist information centre in the arrivals area, staffed by knowledgeable personnel with materials in English, Arabic, and the source languages of the largest inbound segments. Standardise airport taxi fares with clear displayed pricing. Promote the ride-hailing options actively rather than passively. Provide clear, multilingual signage on all transportation options. Maintain road infrastructure visibly on the airport-to-city corridor — it is a small budget against a high-leverage first impression. Incorporate Kuwaiti cultural elements visibly in the airport, not as decoration but as the visitor's first contact with what makes the destination distinctive. Train airport staff in customer service and cultural sensitivity. None of this is expensive at scale; it is a matter of deciding the arrival phase is worth investing in as a product.

Phase 7 — Experiencing: The Country Itself

The experiencing phase is the actual visit — the days on the ground where Kuwait either delivers on the implicit promise of the previous six phases or falls short. This is the phase Kuwait has the most raw material to win on, and the phase the country's current tourism infrastructure has done the least to support.

The well-known landmarks are accessible and worthwhile. The Kuwait Towers offer panoramic views and a recognisable architectural identity. The Sheikh Jaber Al-Ahmad Cultural Centre is a serious cultural venue when it programmes seriously. Souq Al-Mubarakiya is one of the oldest markets in Kuwait, with the lived atmosphere that no theme-park-style heritage construction can replicate. The Grand Mosque provides guided tours through stunning Islamic architecture. These are real assets. The friction is in the supporting layer: on-site information is limited, English-language guided tours are not always reliably available, and the depth of context a visitor receives depends heavily on which day they arrive and which guide they get.

The lesser-known assets are where the gap is largest. Old Kuwait City rewards visitors who walk it with a guide who knows the stories, but the stories are not surfaced for the independent visitor. Salmiya and Al-Bida'a have seaside promenades that are pleasant but not packaged for tourists. Kubbar Island and Umm Al-Maradim are summer destinations for boating and snorkelling, but accessing them requires prior arrangements and local knowledge that the visitor does not have. Winter kashtas in the desert — the traditional camping experience that for Kuwaitis is one of the seasonal highlights of the year — are essentially invisible to the international visitor. The country's hidden assets are hidden by neglect, not by design.

Cultural programming is similar. The Yarmouk Cultural Centre hosts local music and cultural activities of genuine quality. Event information is mostly distributed through local Arabic-language channels. A visitor wanting to attend has to do significant research and often relies on a local contact to even know what is on. The Tareq Rajab Museum is one of the most underrated private collections in the region and one of the least promoted. The raw material for a serious cultural tourism circuit exists. The promotion does not.

The food scene is the one area where Kuwait already delivers without much friction. Traditional dishes like machboos and mutabbaq are widely available. The international cuisine layer in Kuwait City is genuinely diverse. The under-promoted layer is the local family-run eateries that visitors miss without a recommendation — and a curated culinary tour, run by knowledgeable Kuwaiti operators, would turn a strength the country already has into a programmable visitor product.

The shopping malls — The Avenues, Marina Mall, 360 Mall — are functional but resemble malls in every other capital city in the region. They are not a differentiator. The traditional souks and the small Kuwaiti retail operators are the differentiator, and they need surfacing.

The fix at this phase is a curation and promotion programme rather than a construction programme. Develop a network of certified local guides who can offer personalised cultural tours in multiple languages. Publish an updated, accessible events calendar in English and Arabic. Package the hidden assets — Kubbar, Umm Al-Maradim, winter kashtas, the Tareq Rajab Museum, the lesser-known historic neighbourhoods — into bookable visitor experiences. Develop a culinary tourism product around the existing food scene, with food tours and cooking classes. Invest in adventure and leisure offerings — water sports, desert experiences, family-friendly outdoor activities — that fill the current gap between the city experience and what visitors get in neighbouring destinations. Ensure attractions have multilingual staff and materials. Maintain visitor-facing facilities — clean amenities, rest areas, clear signage — to the standard the visitor expects. The argument from the hotel side in From Empty Tables to Cultural Hubs applies at the destination level too: most of what is needed already exists, and the work is to make it visible and bookable, not to build it from scratch.

Phase 8 — Departure: The Last Impression

The departure phase is the last impression the visitor takes with them, and it disproportionately shapes what they tell their network. Kuwait International Airport in 2026 is operating at full capacity by recent measure, with 15.72 million annual passenger movements through terminal infrastructure designed for materially less, and the visitor experience reflects it.

Terminal congestion at check-in and security during peak hours is a recurring complaint. The existing terminal infrastructure struggles to accommodate the current passenger volume. The new mega-terminal under construction will materially change the experience once operational, but the current state is what departing visitors experience. The multi-stage security process — baggage scans and additional verifications — adds time on top of the already-slow flow. Past security, the amenities visitors find depend on how full the terminal is on a given day. Seating is scarce during busy periods; dining and shopping options are limited compared to international peer airports; the lounges are functional but several would benefit from modernisation.

Transportation to the airport is reliable but variable. Taxis, ride-hailing services, and public transport all serve the airport, but unexpected costs and traffic delays can add stress to a visitor's departure day.

The fix is the most straightforward of any phase in the article because the answers are already known. Accelerate the new terminal. Optimise the existing terminal's space in the interim. Streamline security procedures with advanced screening technology where possible. Upgrade the lounges with modern amenities — comfortable seating, charging stations, Wi-Fi, entertainment. Expand the dining and shopping options with an emphasis on showcasing Kuwaiti products and souvenirs. Establish reliable, fairly-priced transportation partnerships to the airport with clear visitor-facing information on options, costs, and timing. Train airport staff in customer service excellence and provide language support across the most common visitor languages. Make signage and information desks multilingual and easily accessible. A visitor whose last ninety minutes in the country were smooth tells a different story to their network than one whose last ninety minutes were stressful, and the difference between those two outcomes is operational, not structural.

Phase 9 — Post-Trip: The Conversation We Are Not Joining

The post-trip phase is the visitor's conversation with their network after they return home, the reviews they post, the recommendations they make, the future visits they consider. It is the phase where most national tourism boards now invest the most aggressively, because it is where word-of-mouth scales. It is the phase Kuwait has done the least with.

The visitor who has been through the previous eight phases returns home with a mixed impression. They probably enjoyed the Grand Mosque tour and the Kuwait Towers view. They probably enjoyed the food. They probably had a frustrating experience at the airport and a confusing one with the visa. They share these experiences in the channels they always use — Instagram, TripAdvisor, group chats with friends and family, occasional blog posts — and the country has almost no infrastructure to engage with what they say.

The opportunities here are concrete. Tourism operators can send personalised post-visit messages thanking the visitor and inviting feedback. The Visit Kuwait social channels can engage actively with user-generated content using official hashtags. Feedback forms can be short, mobile-optimised, and routed to someone who reads them. Identified issues — airport delays, visa friction, language gaps — can be visibly addressed in subsequent communications so the returning visitor sees the country improving. Newsletters featuring upcoming events, new attractions, and seasonal promotions can encourage repeat visits. Online forums or social media groups where past and prospective visitors share experiences and advice can build the kind of organic community that does the country's marketing for free.

None of this is novel. Every serious tourism board in the region runs some version of it. Kuwait does not, which means the country forfeits the most leveraged marketing channel a destination has access to. The visitors are doing the talking anyway — the question is whether Kuwait is in the conversation or not.

What the Country Has to Decide

The nine phases above describe a single country doing the same thing in nine different ways: leaving avoidable friction in place because no one has been responsible for removing it. The aggregate cost of the friction is the KD 2.46 billion of outbound tourism deficit, the inbound leisure visitor numbers that sit far below what the infrastructure could support, the cultural tourism circuit that does not exist because the assets that would anchor it have been left unprogrammed.

The fix is not a vision document. The fix is a decision about which phases to attack first and who is accountable for closing them. My read, after walking the journey end to end, is that the order is: visa rebuild first, because it is the highest-leverage single fix and unlocks several of the other phases; awareness-phase content infrastructure second, because the campaign budget is wasted until the owned channels can hold the visitor when they arrive; arrival-phase information and signage third, because it is cheap and visibly improves first impressions; and a national curated experience programme fourth, because it gives the country the bookable product layer it does not currently have. Everything else follows from those four moves.

The conditions for getting this done are better than they have been in a decade. The hotel pipeline is adding 2,000 keys through 2028, including the new Mandarin Oriental, the converted JW Marriott, and the Nobu development. The Khaleeji Zain tournament demonstrated that Kuwait can run a coordinated international event when the country decides to. Hotel occupancy lifted from 30% in 2024 to 48% in 2025 on the back of better visa accessibility and growing regional interest — the early signal that, when the country fixes one friction point, the visitor responds.

What the country needs now is the discipline to pick the four moves above, assign each one to a specific accountable team, and not let the work drift into the multi-year planning exercises that have absorbed every previous attempt. The visitor journey is nine phases long. The first year of work is four of them. Kuwait does not need a new tourism vision to start. It needs to start.

I have spent twenty years walking customer journeys for clients in hospitality, finance, automotive, and luxury, and Kuwait's tourism journey is the most fixable I have audited. The assets exist. The talent exists. The capital exists. The only missing input is the decision to begin.