Automotive Market Kuwait: 2025 Trends and Sales

.webp)

Record Sales, Market Shifts, and the Rise of Chinese Brands

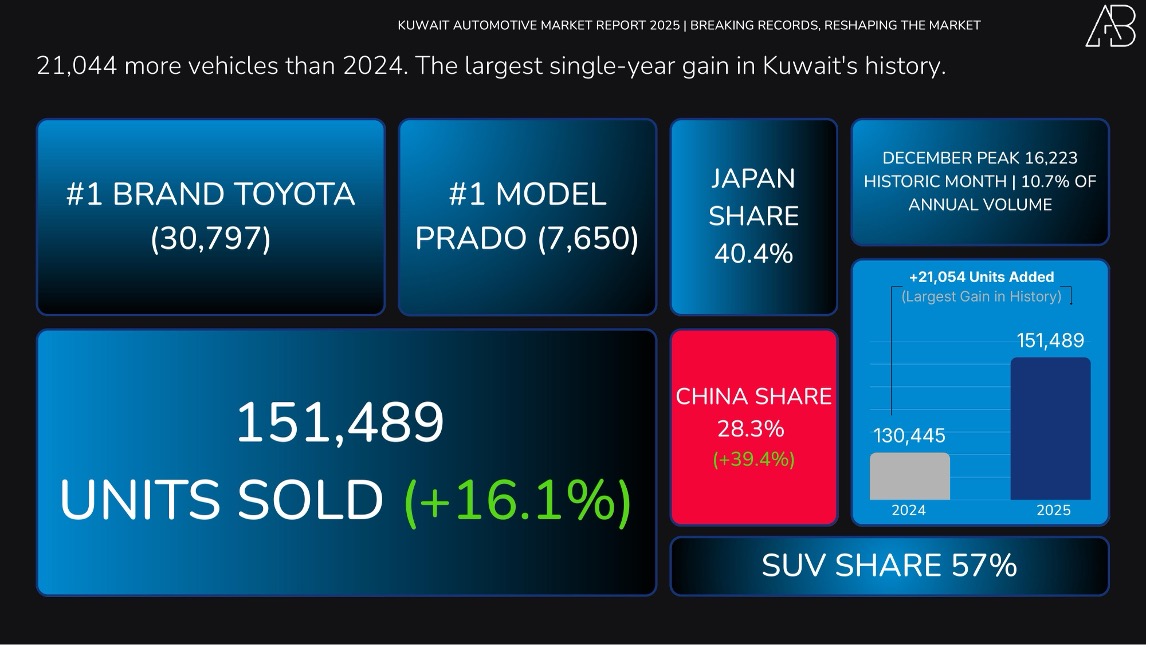

Kuwait registered 151,489 vehicles in 2025. That is more than in any previous year. Sales grew 16.1% from 130,445 units in 2024, adding 21,054 vehicles to the market in twelve months.

But 2025 was not just Kuwait’s biggest car year on record. It was the year the market quietly changed shape.

Chinese brands now account for 28% of all vehicles sold in Kuwait. SUVs account for 57% of registrations. December 2025 was the busiest sales month on record. For anyone selling, buying, or watching this market, the patterns have changed.

This report uses official vehicle registration data from Kuwait's Ministry of Interior, covering 2013 through 2025. Every figure comes from the same source. No estimates, no projections, just what dealers actually registered.

Where the Market Has Been

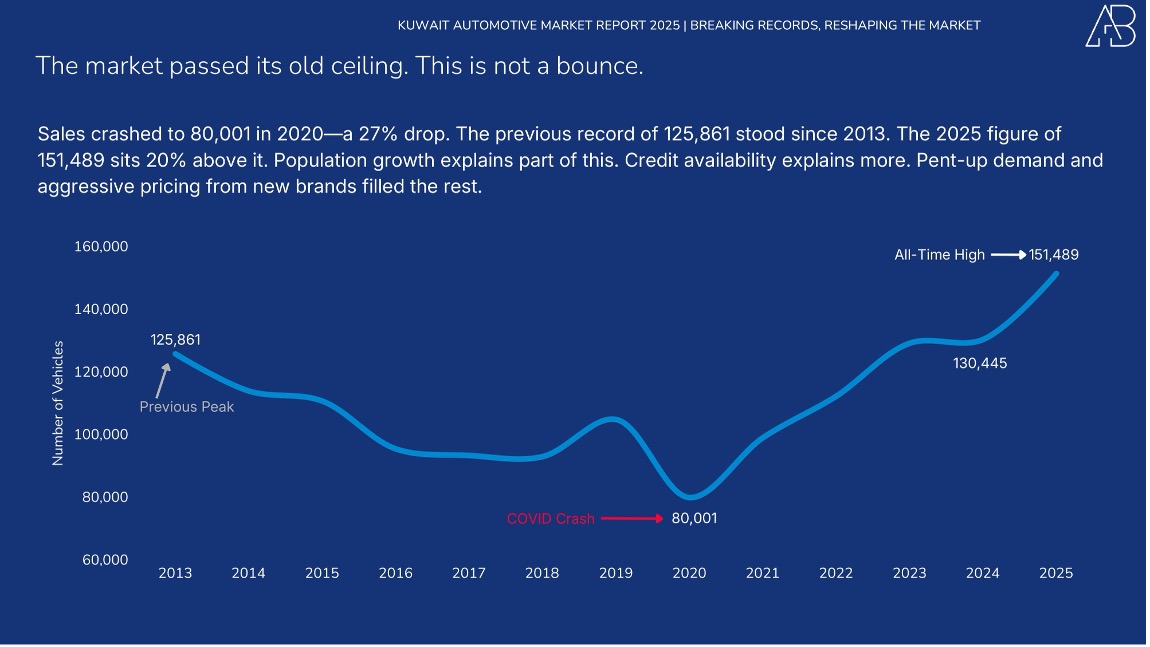

The pandemic drove sales to 80,001 units in 2020, a 27% drop from 2019. What followed was not a return to normal. The market grew past its old ceiling.

Before 2025, Kuwait's highest sales year was 2013, when dealers registered 125,861 vehicles. That record stood for over a decade. The 2025 figure of 151,489 sits 20% above it.

Population growth explains part of this. Credit availability explains more. Pent-up demand from pandemic years and aggressive pricing from new brands filled the rest.

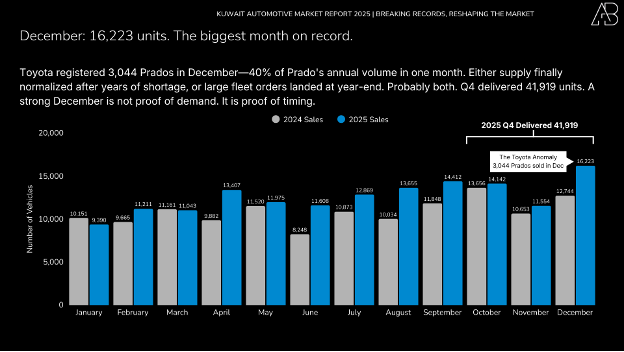

December 2025: 16,223 Units

December delivered 16,223 vehicles, the highest single-month total in Kuwait's records. Q4 is always strong. Dealers clear inventory. Buyers chase year-end promotions. Government and corporate fleets finalize orders before budgets reset.

One detail stands out: Toyota registered 3,044 Prados in December. That is 40% of Prado's annual volume in one month. Either supply finally normalized after years of shortage, or large fleet orders landed at year-end. Probably both.

The Seasonality Pattern

Kuwait's car sales follow a predictable rhythm. Q4 runs 20-25% above baseline. December's index hits 126, up from a 100 average. June typically dips to 95.

Any brand planning inventory, campaigns, or launches without accounting for this pattern is flying blind. A strong December does not mean demand suddenly spiked. A weak June does not mean the market collapsed. Both reflect timing, not underlying shifts.

Ramadan's moving calendar adds another layer. When it falls in Q2, sales dip further. When it ends near Q4, the post-Ramadan bounce amplifies year-end strength. In 2025, Ramadan ran from late February to late March, keeping the early-year dip contained.

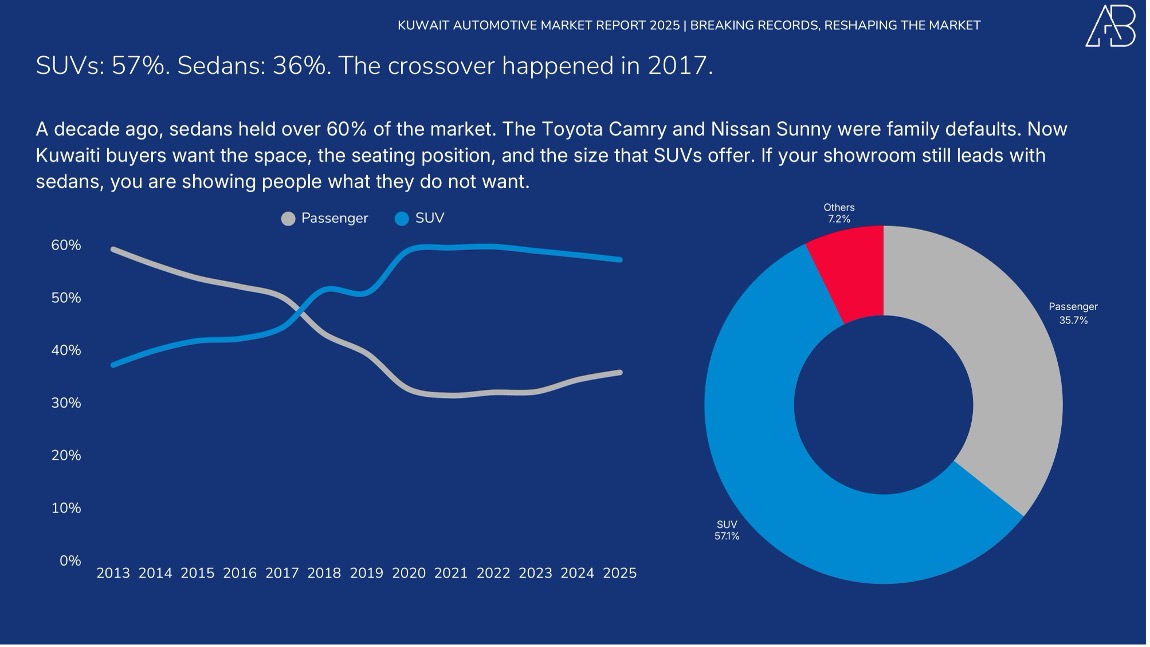

SUVs at 57%, Sedans at 36%

Walk through any Kuwaiti parking lot. Count the SUVs. The registration data matches what you see: SUVs now sell at 57% of the market. Sedans have fallen to 36%. The remaining 7% covers pickups, vans, and commercial vehicles.

This crossover happened in 2017. A decade ago, sedans held over 60% of the market. The Toyota Camry and Nissan Sunny were family defaults. Now, Kuwaiti buyers want the space, the seating position, and the size that SUVs offer.

The shift affects everything from dealer floor allocation to manufacturer product strategy. Showrooms that once featured sedans prominently now lead with SUVs. Production priorities follow.

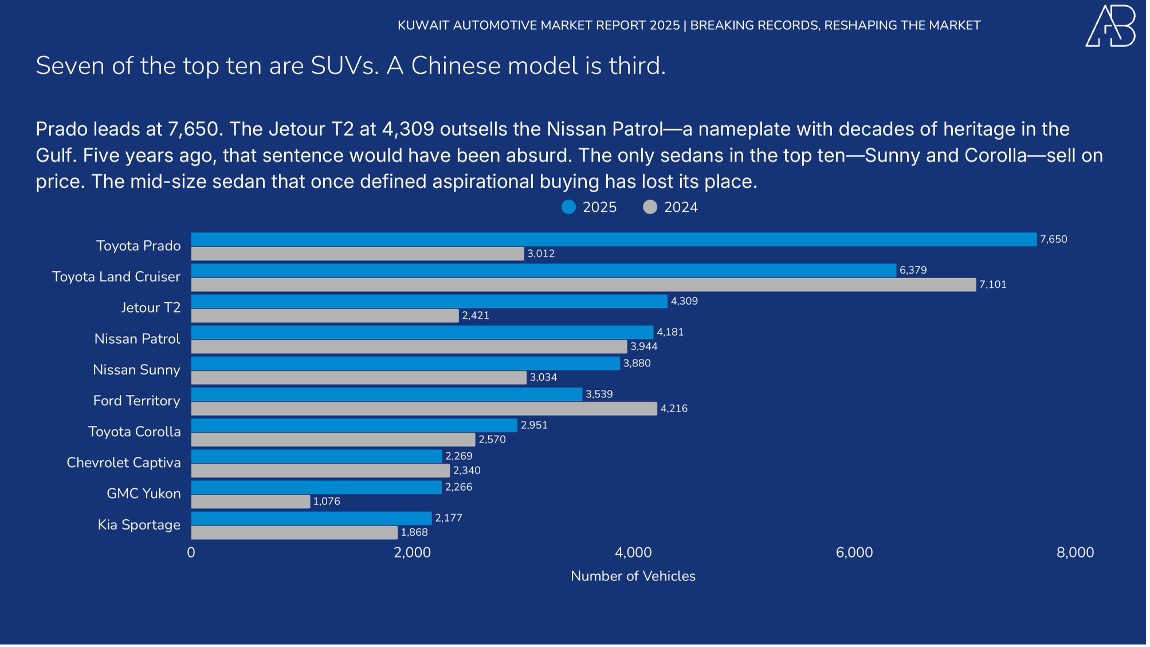

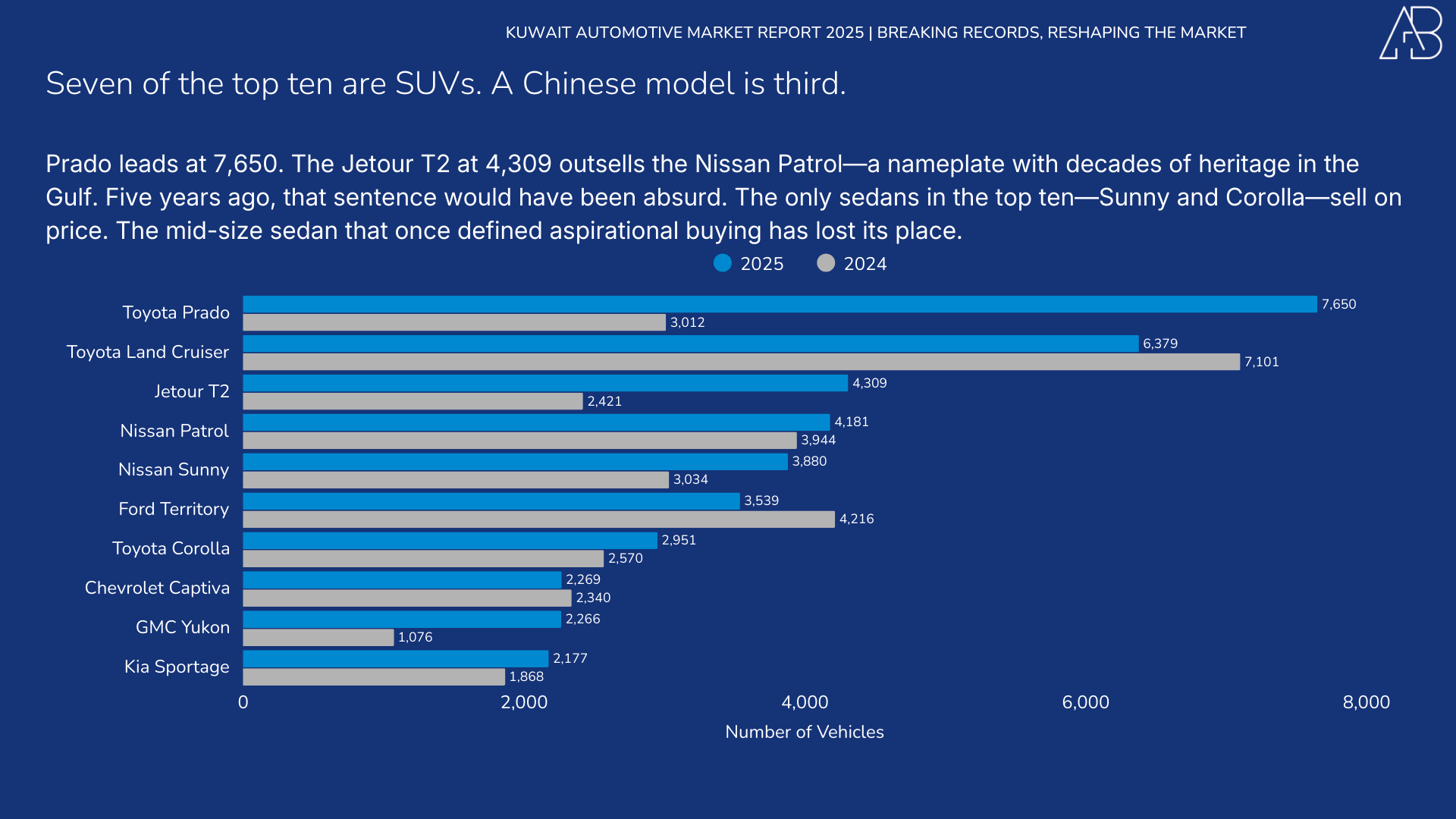

The Ten Best-Sellers

The top ten models in 2025: Toyota Prado (7,650), Toyota Land Cruiser (6,379), Jetour T2 (4,309), Nissan Patrol (4,181), Nissan Sunny (3,880), Ford Territory (3,539), Toyota Corolla (2,951), Chevrolet Captiva (2,269), GMC Yukon (2,266), and Kia Sportage (2,177).

Seven of these are SUVs. The only sedans that broke through, Sunny and Corolla, sell on price. The mid-size sedan that once defined aspirational buying has lost its place.

The Jetour T2 at third is the headline. A Chinese SUV outselling the Nissan Patrol, a nameplate with decades of heritage in the Gulf, would have seemed implausible five years ago. Now it is a fact.

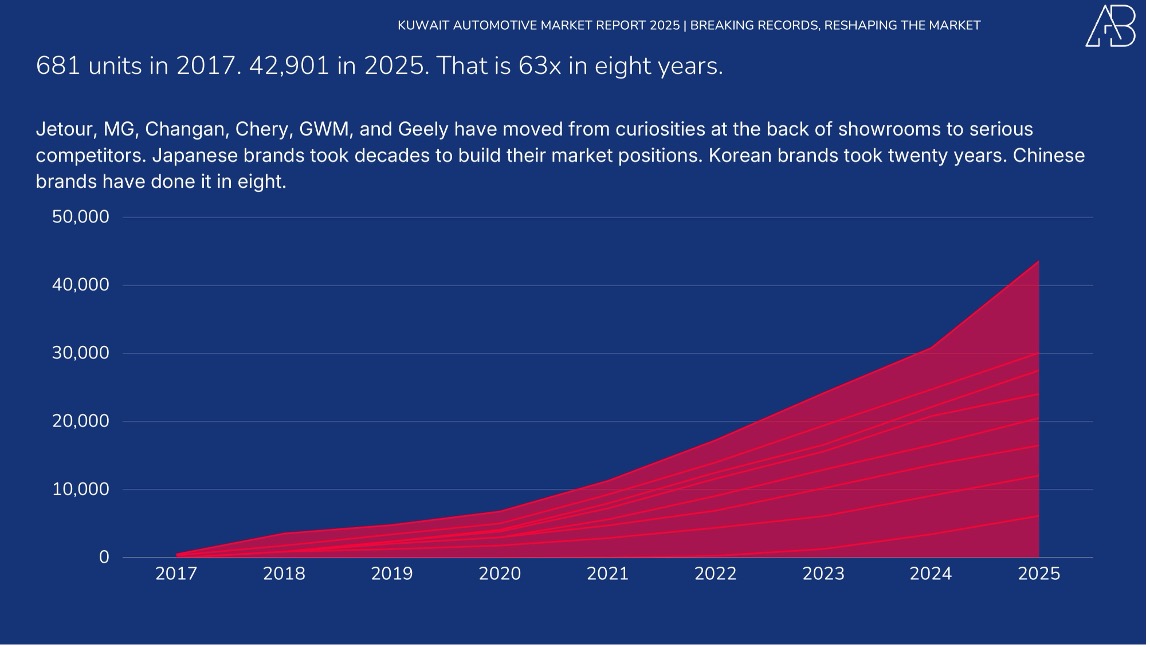

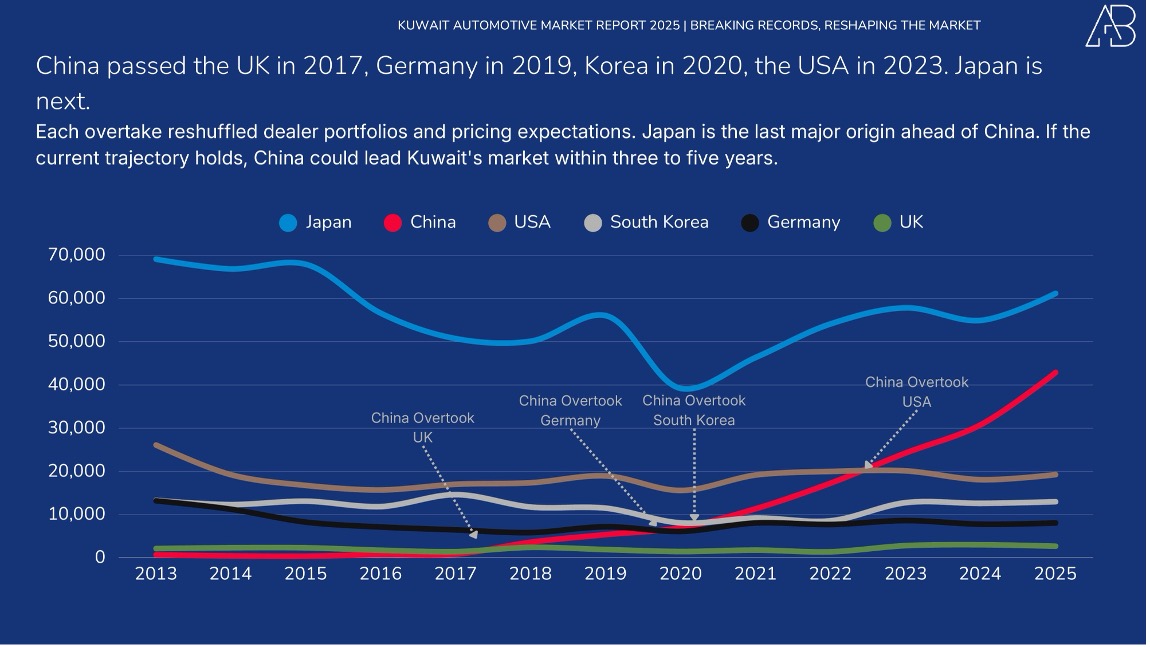

China: From 681 to 42,901 in Eight Years

In 2017, Chinese brands sold 681 vehicles in Kuwait. In 2025, they sold 42,901. That is a 63-fold increase.

Jetour, MG, Changan, Chery, GWM, and Geely have moved from curiosities at the back of showrooms to serious competitors. The Jetour T2 sits in third place overall with 4,309 units. It is the first Chinese model to crack Kuwait's top five.

The speed of this shift matters. Japanese brands took decades to build their market positions. Korean brands took twenty years. Chinese brands have done it in eight. Whether this pace continues depends on quality, consistency, and after-sales service networks.

The skeptics have legitimate questions. Resale values for Chinese brands remain unproven in Kuwait’s secondary market. Long-term durability data does not exist yet. Second-owner confidence is lower than for Japanese vehicles. These factors matter, and any honest analysis must acknowledge them. But first-owner buyers are voting with their wallets, and the trajectory is clear.

Japan Is Losing Share, Not Because It Sells Less

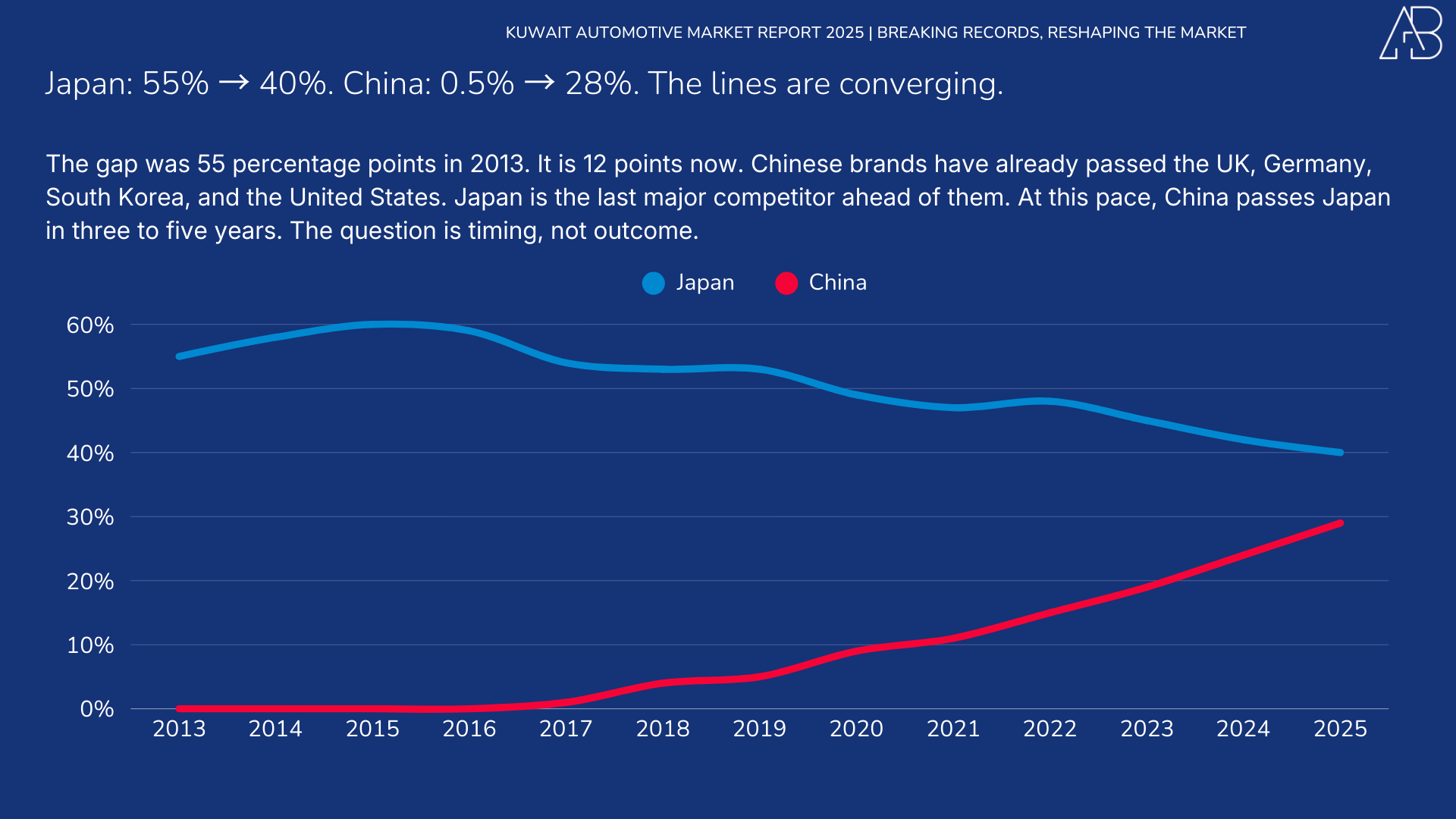

Japan held 55% of Kuwait's car market in 2013. It holds 40% today. Over the same period, China went from 0.5% to 28%.

Chinese brands have already overtaken those of the UK, Germany, South Korea, and the United States in Kuwait's rankings. Japan is the last major competitor ahead of them. If the current trajectory holds, China could pass Japan within three to five years.

The gap was 55 percentage points in 2013. It is 12 points now.

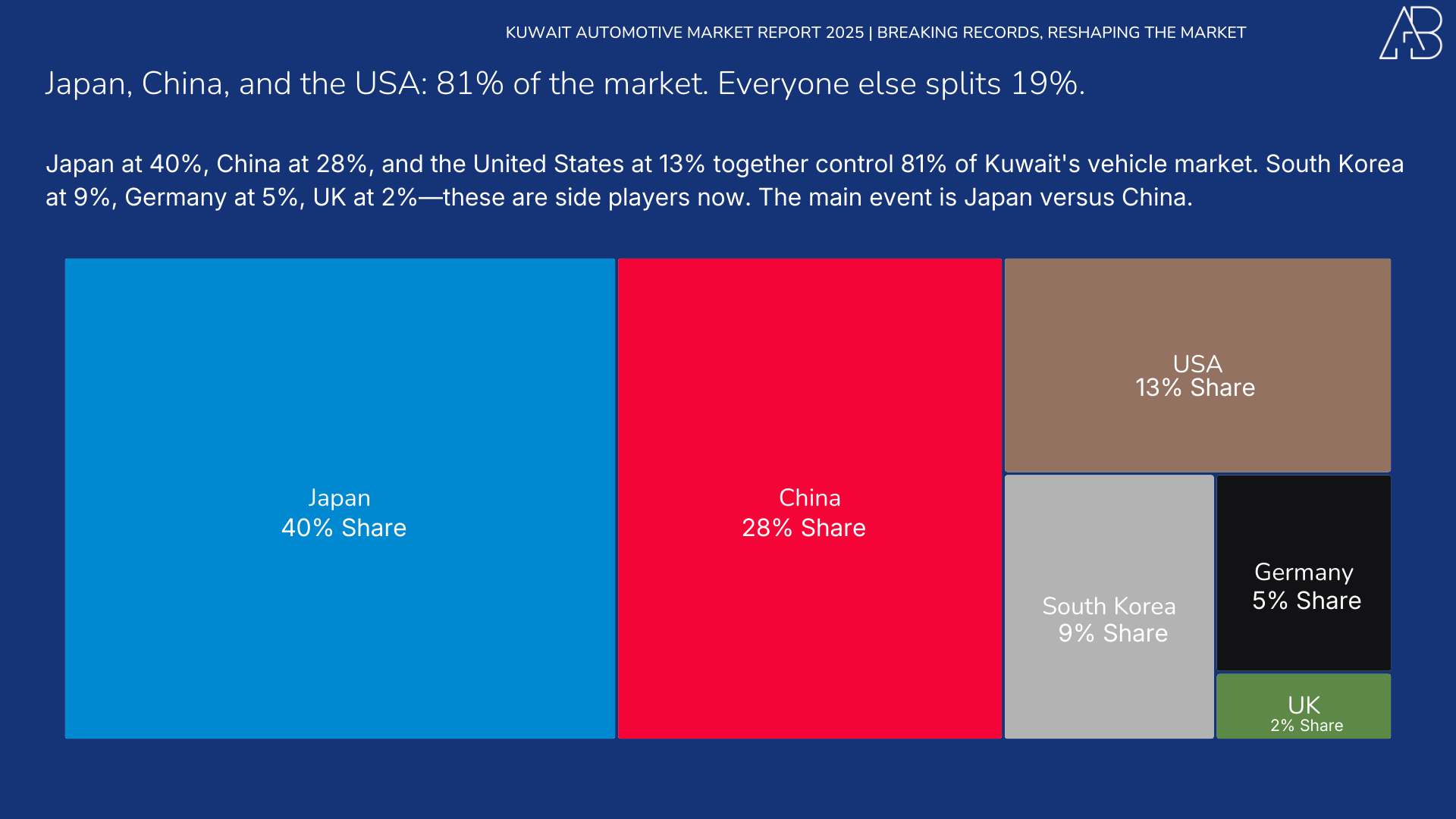

Three Countries, 81% of Sales

Japan at 40%, China at 28%, and the United States at 13% together control 81% of Kuwait's vehicle market. South Korea holds 9%, Germany 5%, and the UK 2%. Everyone else splits the remaining 3%.

Where Chinese Brands Win

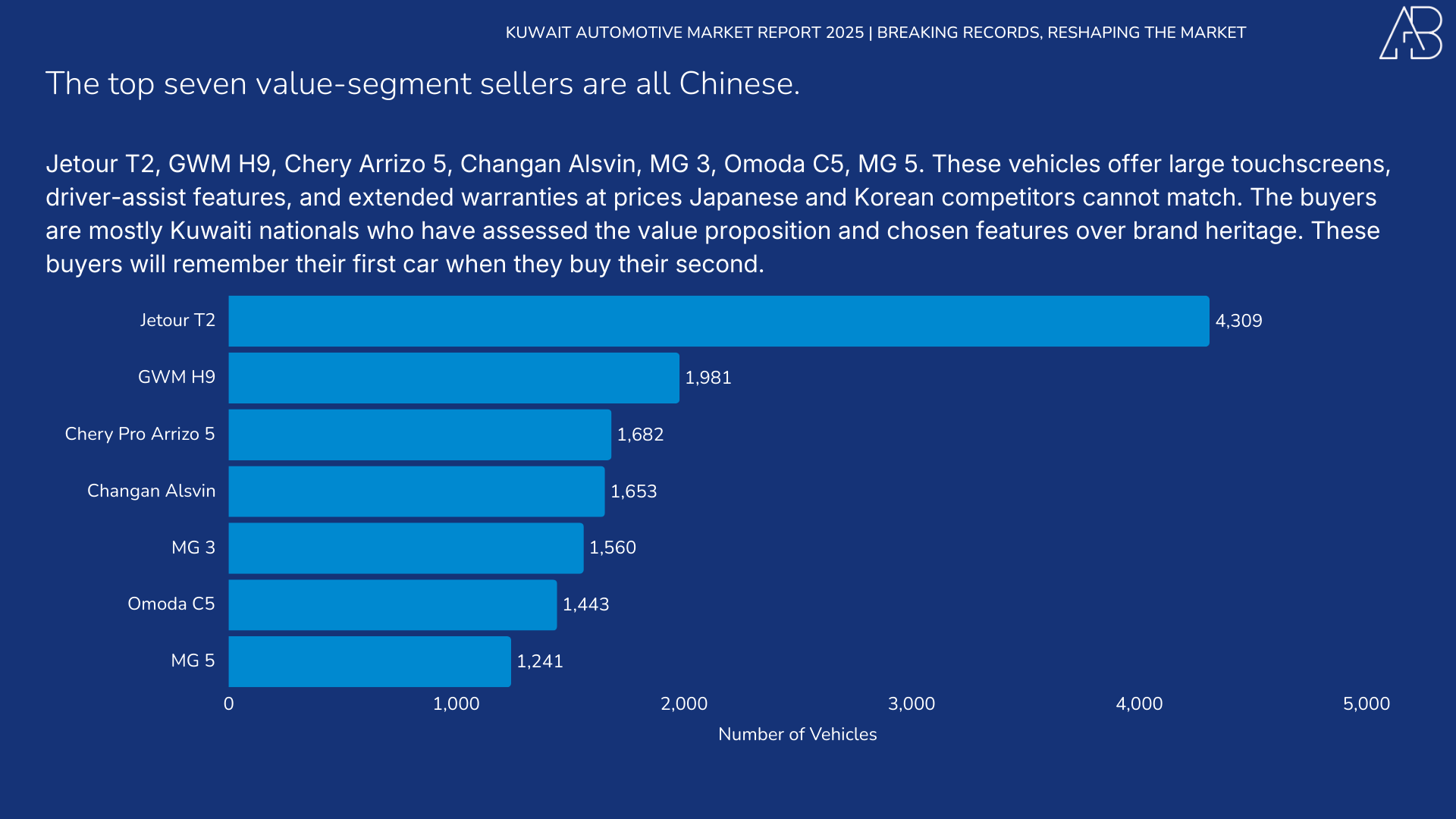

Chinese brands own the value segment. The top seven sellers in the budget-conscious bracket are all Chinese: Jetour T2, GWM H9, Chery Arrizo 5, Changan Alsvin, MG 3, Omoda C5, and MG 5.

These vehicles offer large touchscreens, driver-assist features, and extended warranties at prices Japanese and Korean competitors cannot match. The buyers are mostly Kuwaiti nationals, not expatriates. Strict license requirements for expats, a minimum salary of 600 KD, a university degree, and 2 years of residency mean that Kuwaitis make up roughly 83% of car purchases.

This demographic reality reshapes how to think about the Chinese brand buyer. These are not budget-constrained expats seeking any affordable option. They are Kuwaiti nationals who have assessed the value proposition and chosen features over brand heritage.

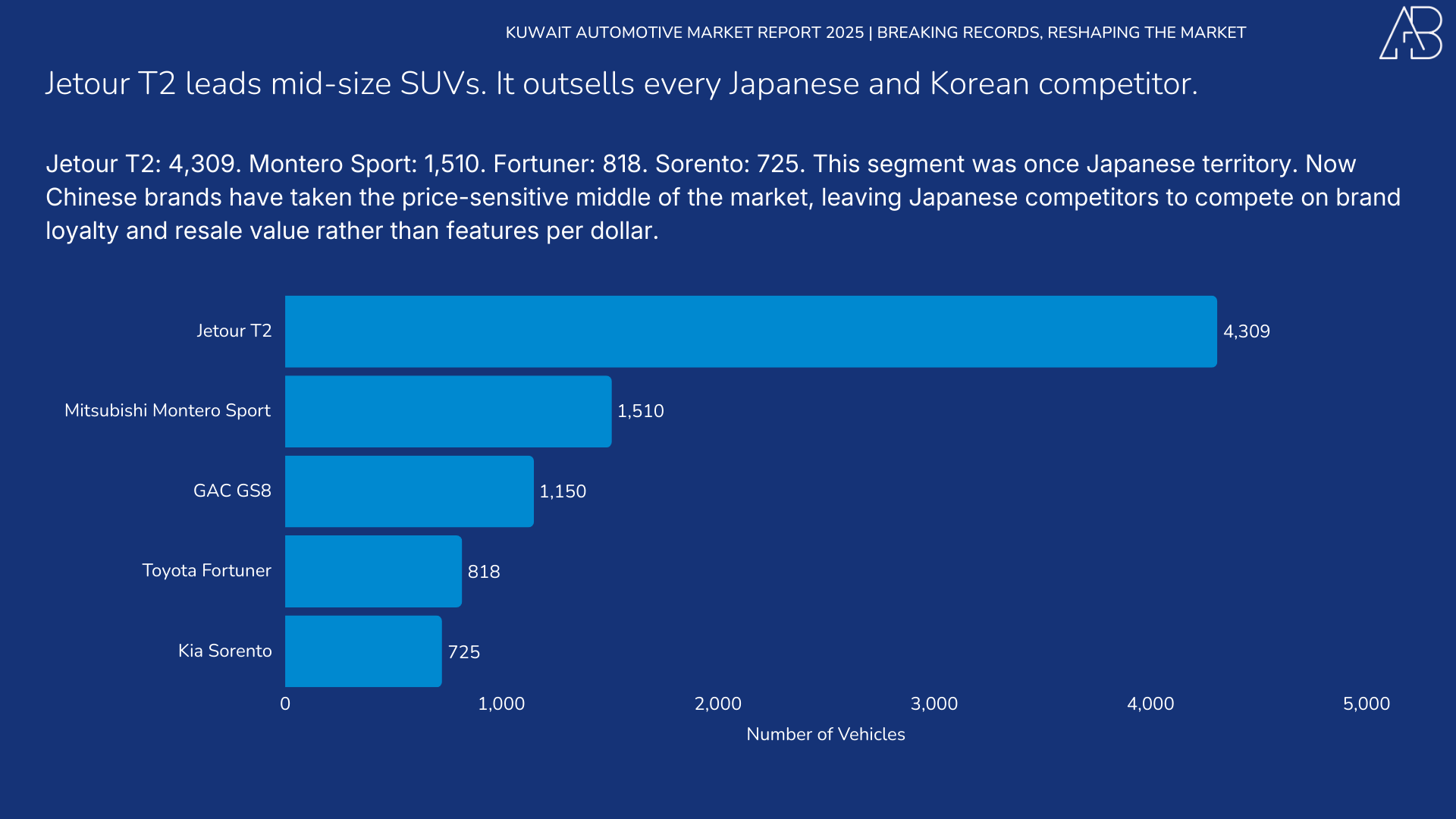

Mid-Size SUVs: Chinese Brands Lead

In the mid-size SUV segment, a Chinese model outsells all Japanese and Korean competitors. The Jetour T2, with 4,309 units, leads the segment, followed by the Ford Territory at 3,539 and the Chevrolet Captiva at 2,269.

This segment was once Japanese territory. Now, Chinese brands have taken the price-sensitive middle of the market, leaving Japanese competitors to compete on brand loyalty and resale value rather than features per dollar.

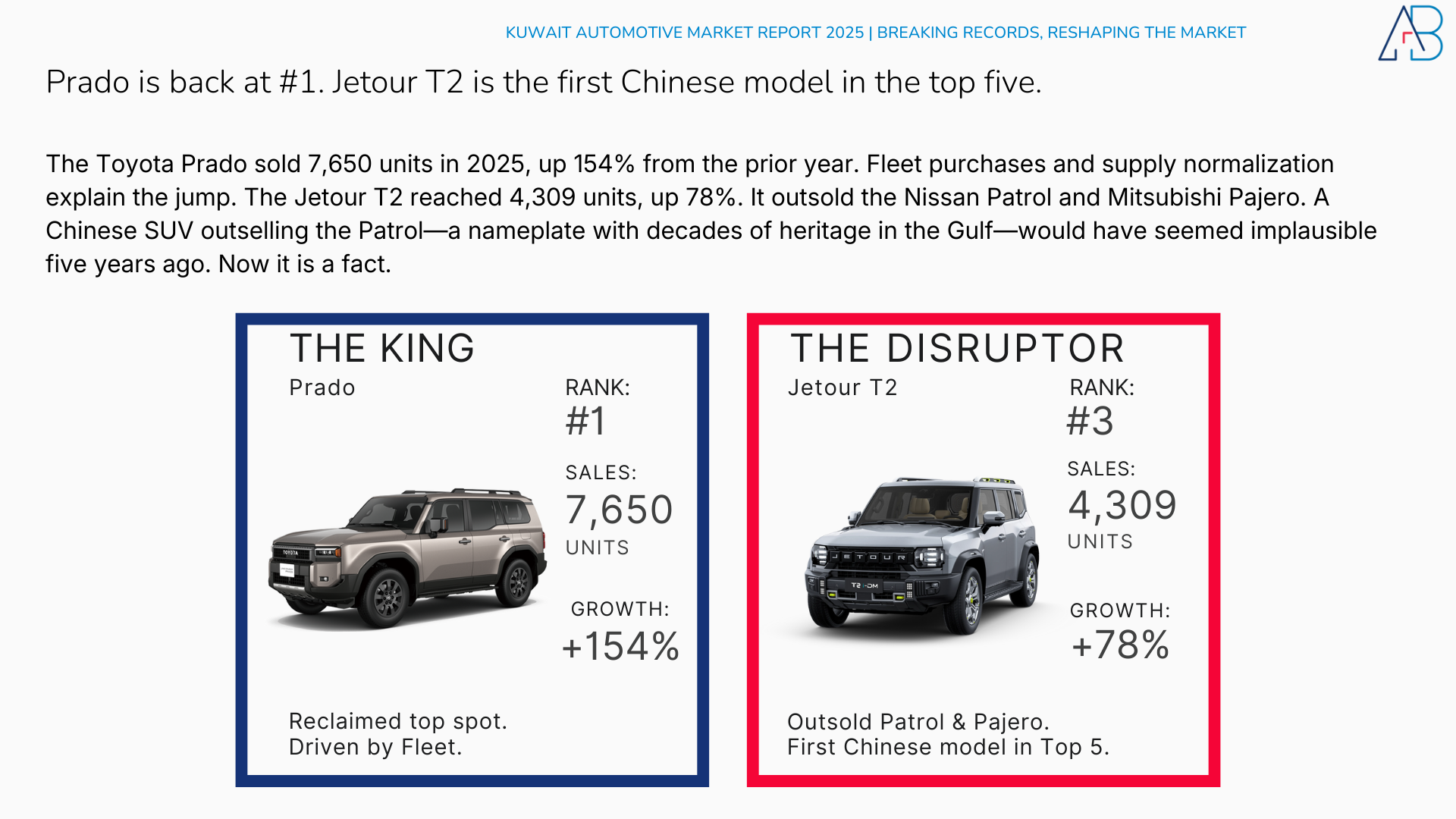

Prado Reclaims First, Jetour Takes Third

The Toyota Prado sold 7,650 units in 2025, up 154% from the prior year. Fleet purchases and supply normalization explain the jump. The Jetour T2 reached 4,309 units, up 78%. It outsold the Nissan Patrol and Mitsubishi Pajero.

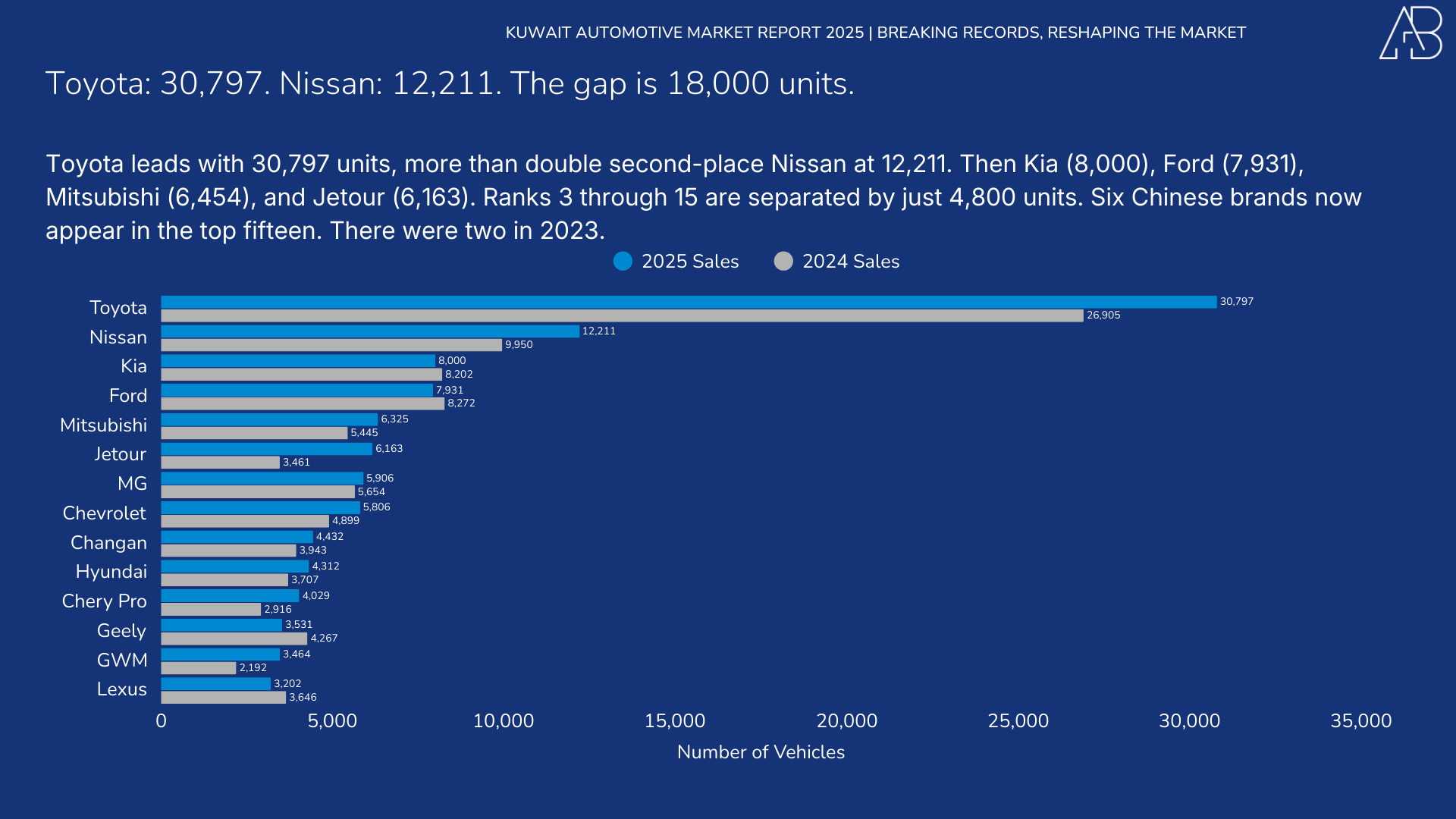

Brand Rankings

Toyota leads with 30,797 units, more than double the second-place Nissan at 12,211. Then Kia (8,000), Ford (7,931), Mitsubishi (6,454), and Jetour (6,163). Six Chinese brands now appear in the top fifteen.

Who Drove the Growth

Four brands added over half of the market's 21,054-unit expansion. Toyota added 3,892 units. Jetour added 2,702. Nissan added 2,261. GWM added 2,124. Two of these four are Chinese.

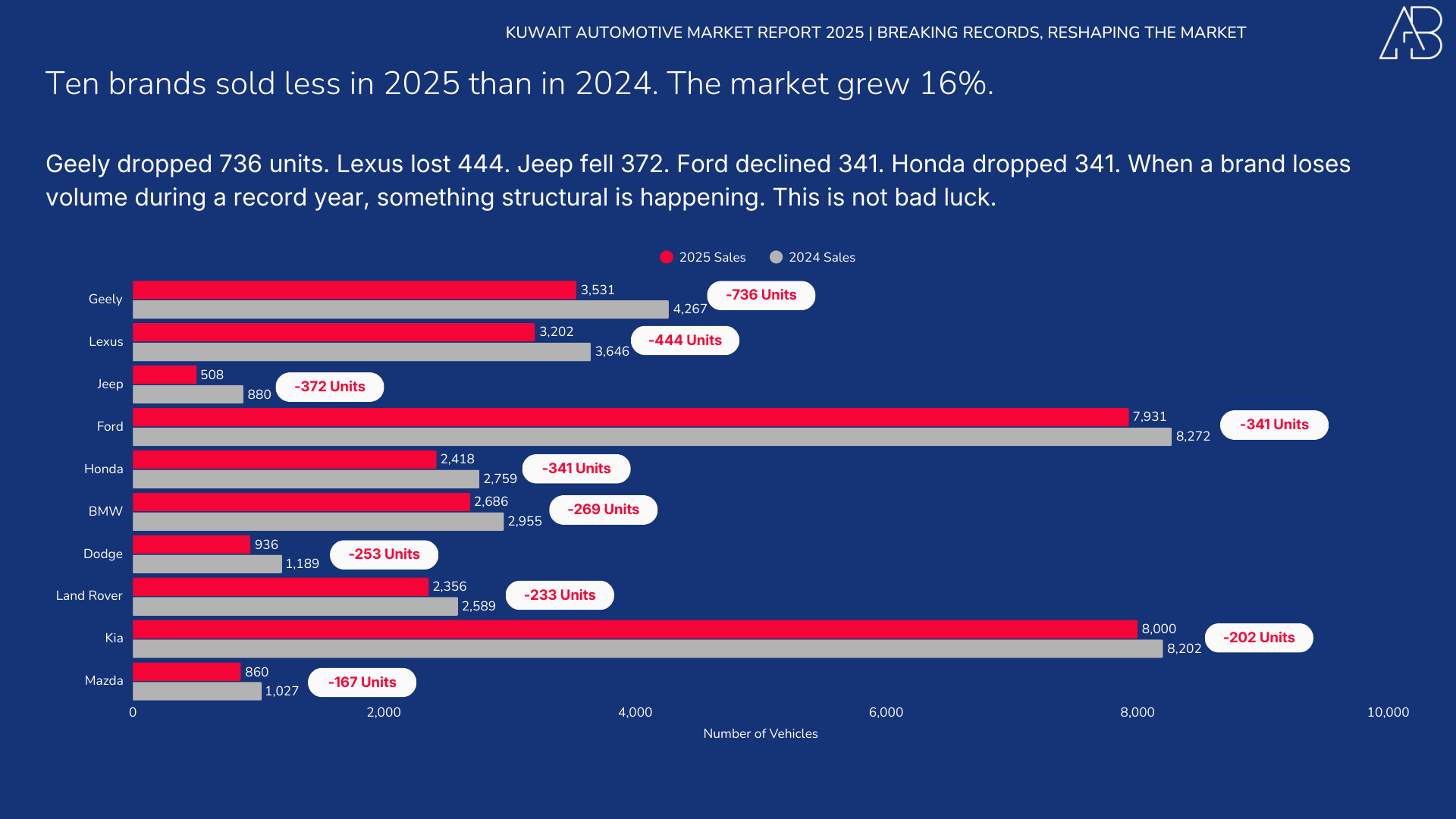

The Brands That Lost Ground

Ten brands sold fewer vehicles in 2025 than in 2024, even as the overall market grew 16%. Geely dropped 736 units, Lexus lost 444, Jeep fell 372, Ford declined 341, and Honda dropped 341. When a brand loses volume during a record year, something structural is happening.

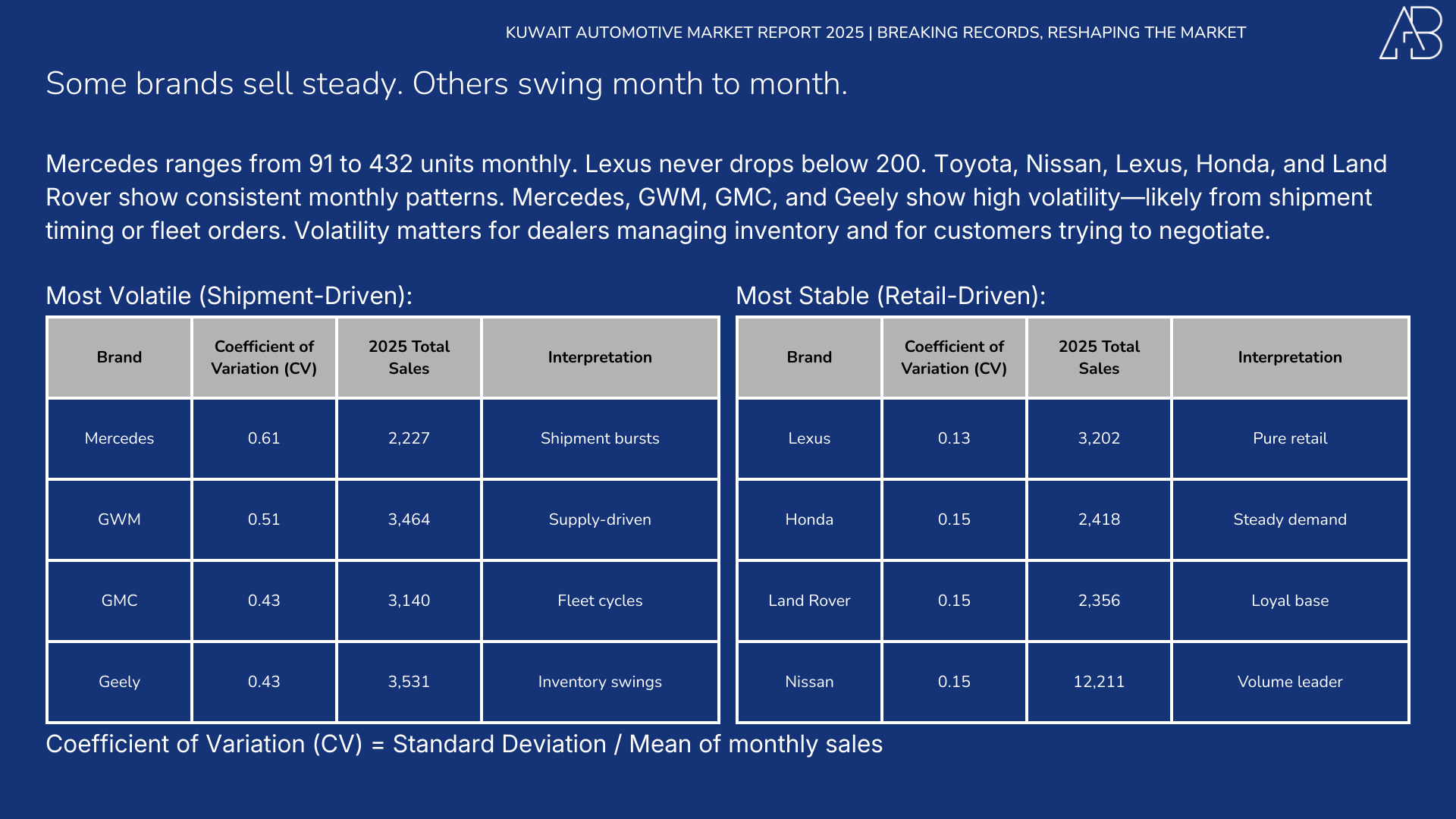

Stable vs Volatile Brands

Some brands sell steadily month after month. Others swing widely. Toyota, Nissan, Lexus, Honda, and Land Rover show consistent monthly patterns. Mercedes, GWM, GMC, and Geely show high volatility, likely from shipment timing or fleet orders.

Volatility matters for dealers managing inventory and for customers trying to negotiate. A brand that sells 500 units every month operates differently from one that sells 200 in June and 1,200 in December.

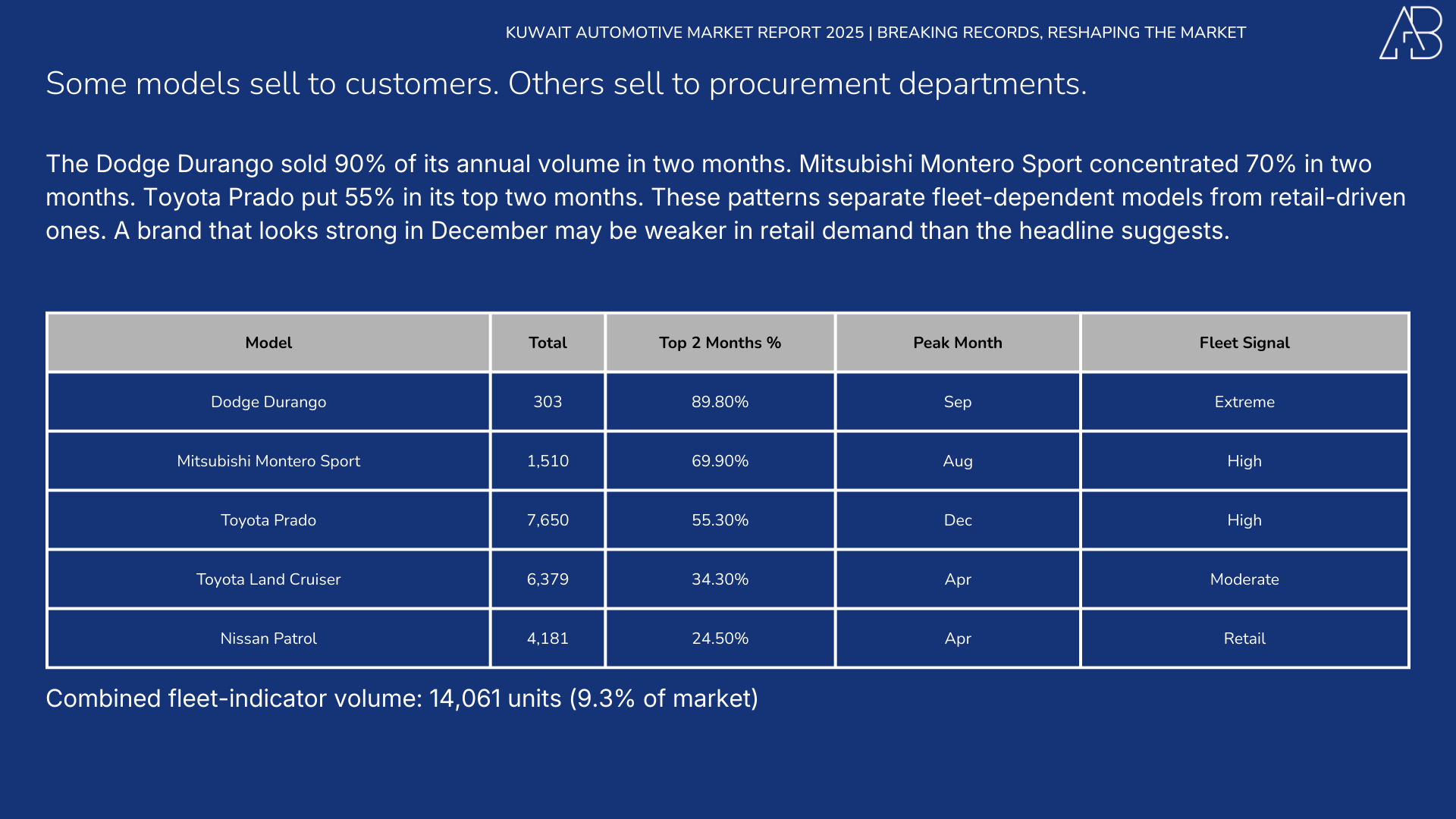

Fleet vs Retail Patterns

Certain models show sales spikes that indicate bulk purchases. The Dodge Durango sold 90% of its annual volume in two months. Mitsubishi Montero Sport concentrated 70% in two months. Toyota Prado put 55% in its top two months. These patterns separate fleet-dependent models from retail-driven ones.

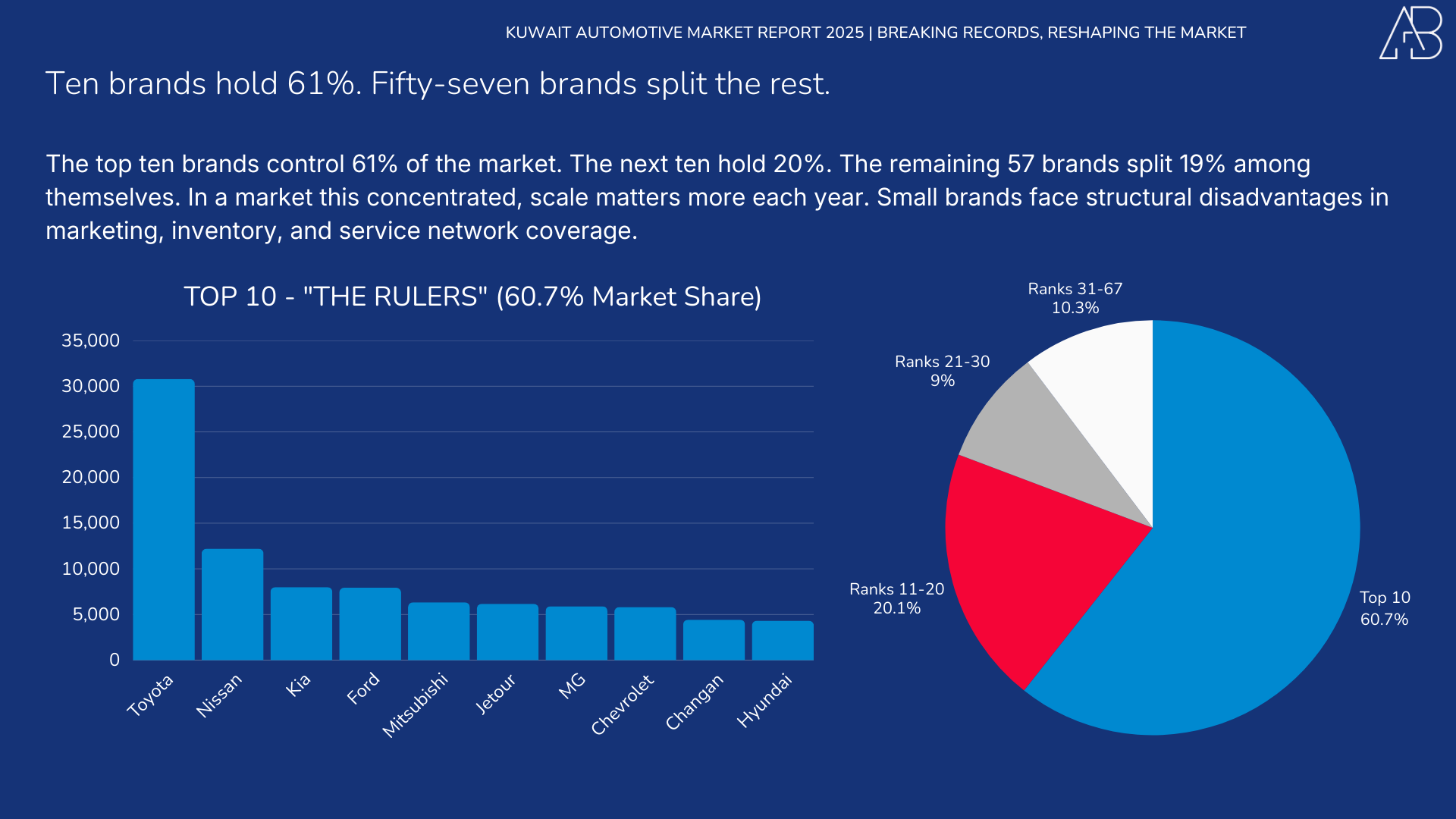

Market Concentration

The top ten brands control 61% of the market. The next ten hold 20%. The remaining 57 brands split 19% among themselves.

Dealer Group Dominance

Two dealer groups sold 39% of all vehicles in Kuwait in 2025. Mohamed Naser Al Sayer (Toyota, Lexus) and Alghanim Auto (Chevrolet, Ford) together moved nearly 60,000 units.

This concentration shapes the competitive market. When two groups control nearly two-fifths of the market, their inventory decisions, financing terms, and promotional calendars set the rhythm for everyone else.

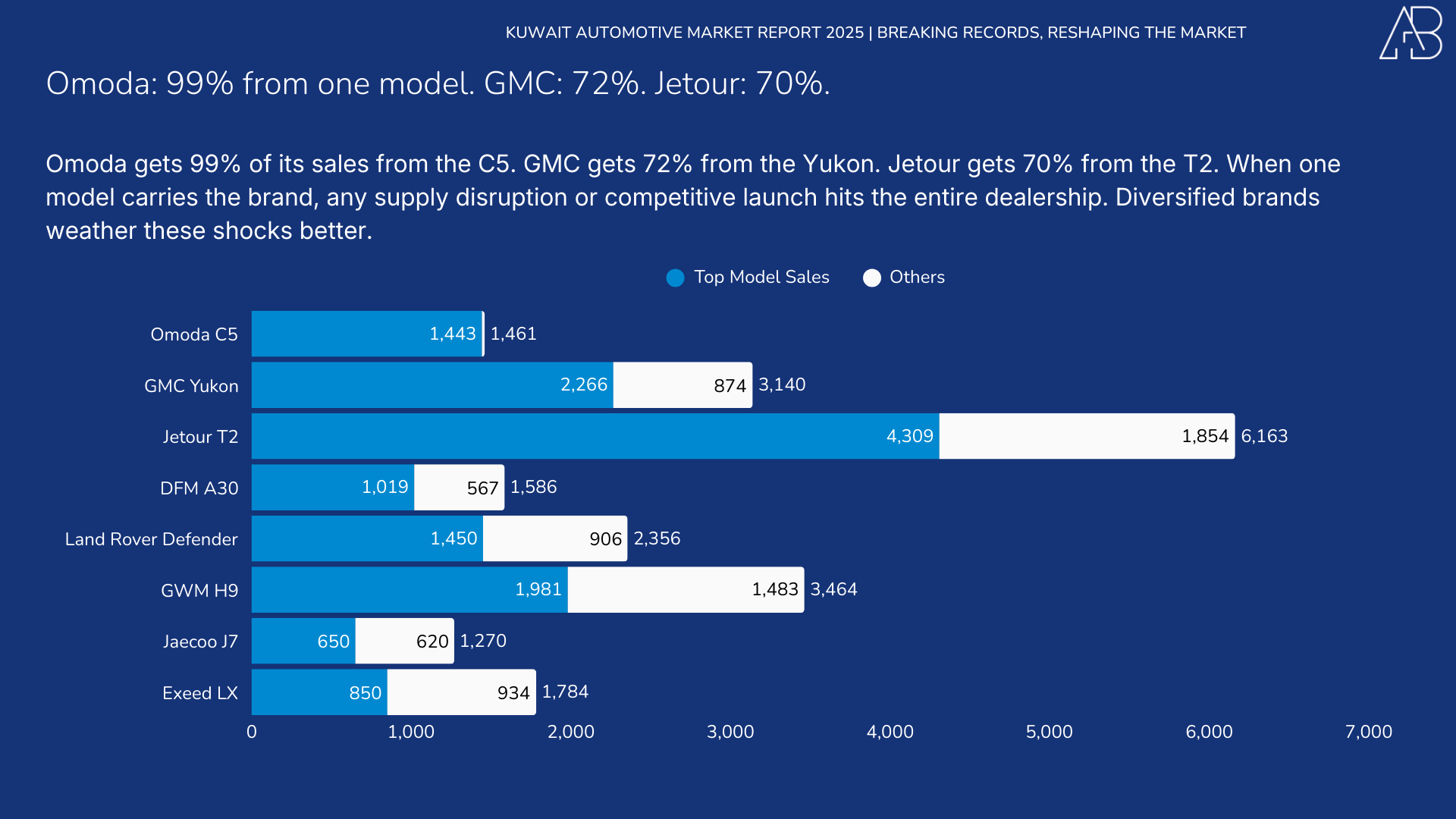

Single-Model Brands

Some brands depend heavily on one model. Omoda gets 99% of its sales from the C5. GMC gets 72% from the Yukon. Jetour gets 70% from the T2. If supply disrupts or a competitor launches an alternative, these brands face disproportionate risk.

What This Means If You Run a Dealership

The data points to three operational realities:

Floor space allocation needs to follow the data. If SUVs are 57% of what buyers want, but sedans still dominate your showroom, you are showing customers what they do not want to buy. The premium floor footage devoted to sedans should shrink proportionally.

Single-model brands carry inventory risk. When 70-99% of a brand’s sales come from one model, any supply disruption or competitive launch hits the entire dealership. Diversified brands weather these shocks better.

December numbers distort annual performance. Fleet purchases, year-end targets, and inventory clearance spike Q4 volumes. A brand that looks strong in December may be weaker in retail demand than the headline suggests. Strip out December when evaluating underlying performance.

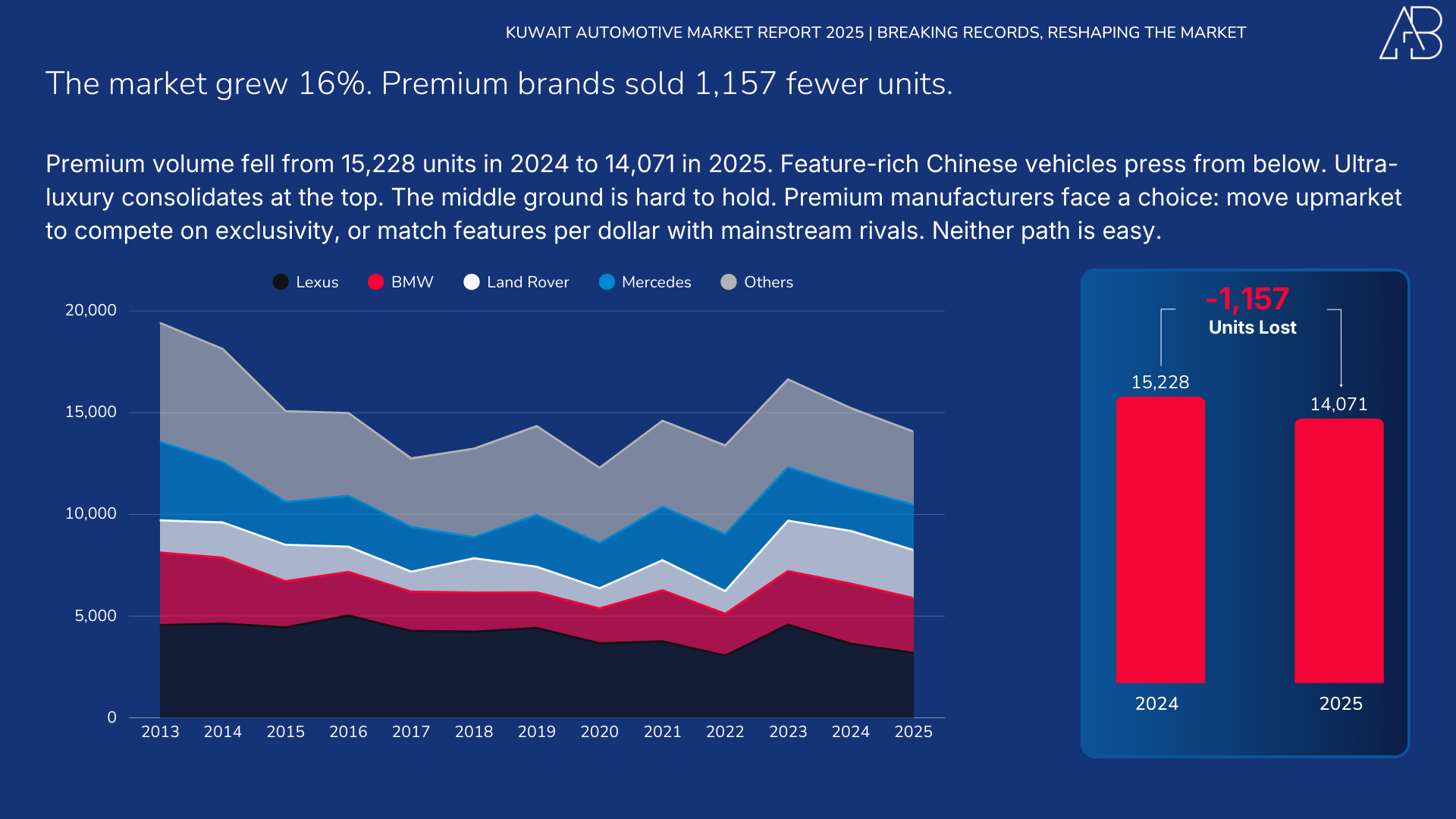

The Premium Segment Shrank

While the overall market grew 16%, premium brands sold fewer vehicles. Premium volume fell from 15,228 units in 2024 to 14,071 in 2025, a drop of 1,157 units.

Feature-rich Chinese vehicles press from below. Ultra-luxury consolidates at the top. The middle ground is hard to hold.

This squeeze affects brand strategy. Premium manufacturers face a choice: move upmarket to compete on exclusivity, or match features per dollar with mainstream rivals. Neither path is easy when the mainstream keeps adding features.

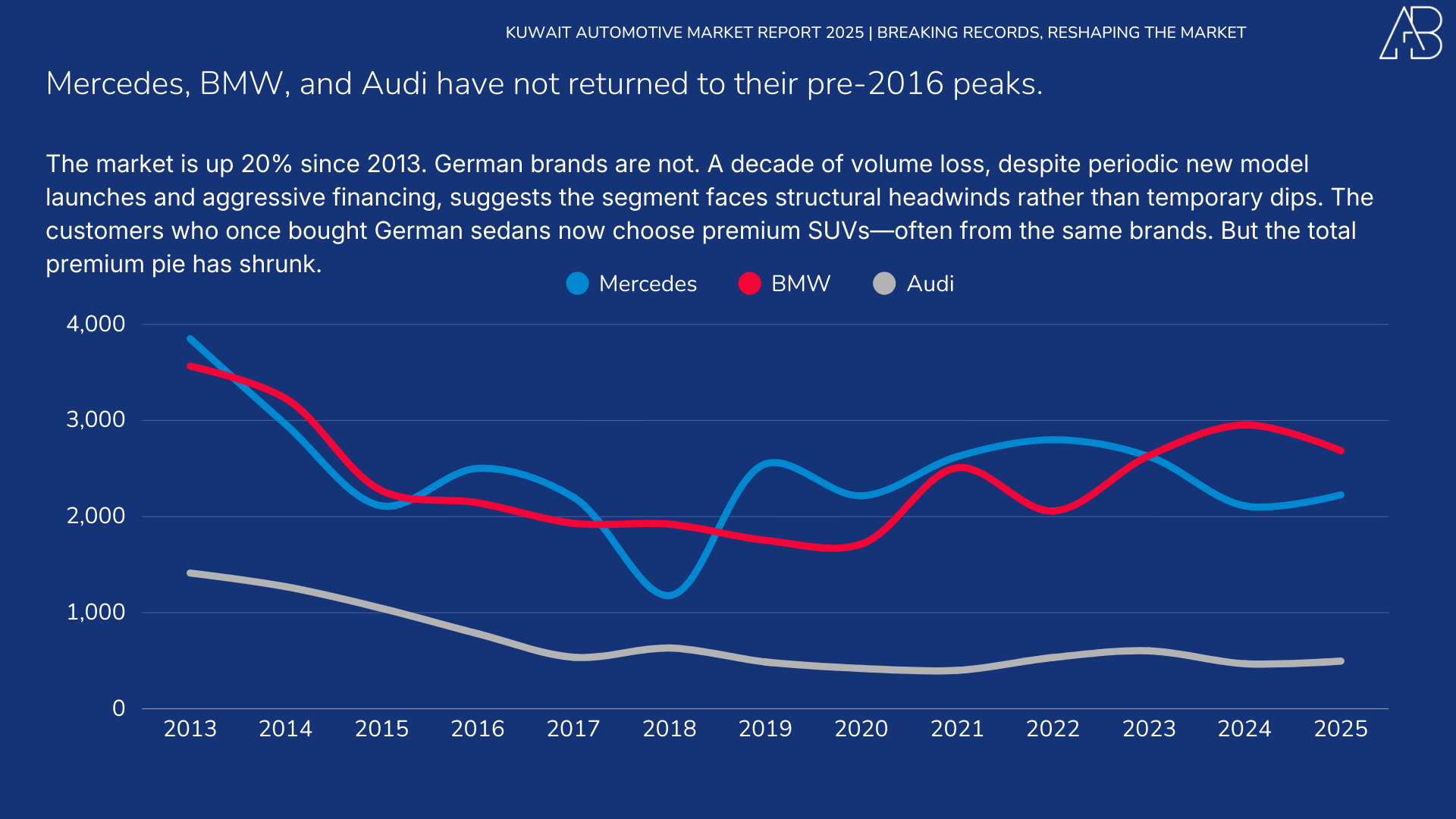

German Brands: Still Below 2016 Peaks

Mercedes, BMW, and Audi have not returned to their pre-2016 sales levels in Kuwait. A decade of volume losses, despite periodic new-model launches and aggressive financing, suggests the segment faces structural headwinds rather than temporary dips.

The customers who once bought German sedans now choose premium SUVs, often from the same brands. But the total premium pie has shrunk.

Premium Buyers Moved to SUVs

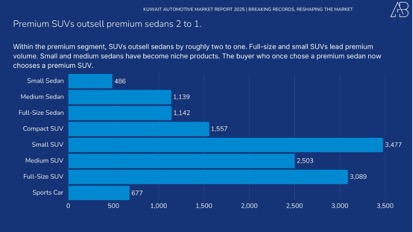

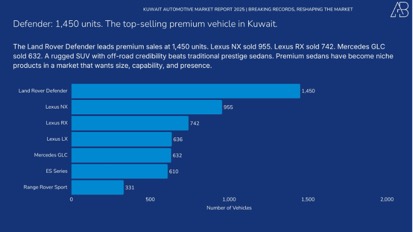

Within the premium segment, SUVs outsell sedans by roughly two to one. The Land Rover Defender is Kuwait's best-selling premium vehicle, with 1,450 units sold. Lexus NX sold 955. Mercedes GLC sold 632. Premium sedans have become niche products.

Premium SUV Breakdown

In compact premium SUVs, BMW dominates with the X1 and X2, outselling competitors from Mercedes and Audi.

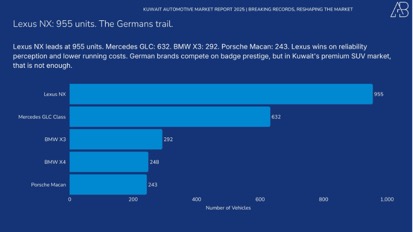

The small premium SUV segment sees Lexus NX leading ahead of German rivals.

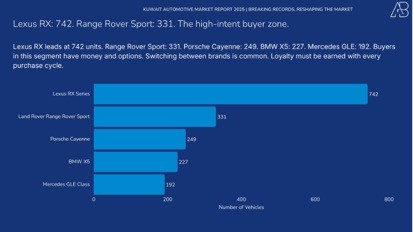

Mid-size premium SUVs are led by the Lexus RX and Range Rover Sport.

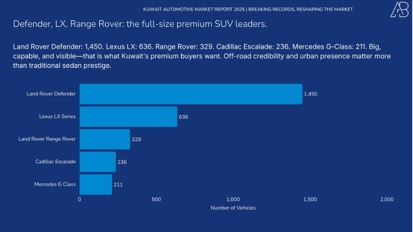

Full-size premium SUVs have the Defender at top, followed by the Lexus LX and Range Rover.

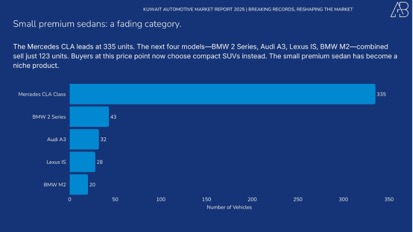

Premium Sedans: A Shrinking Category

Small premium sedans have become a niche. The BMW 2 Series, Mercedes-CLA Class, and Audi A3 compete for a shrinking pool of buyers who still want a premium badge on a compact sedan.

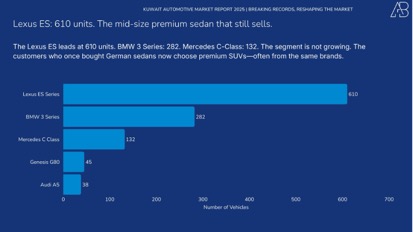

Mid-size premium sedans see the Lexus ES leading at 610 units, followed by the BMW 3 Series and Mercedes C-Class.

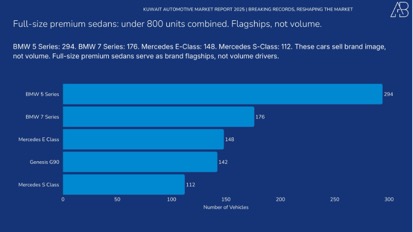

Full-size premium sedans, the BMW 5 and 7 Series, Mercedes S-Class serve as brand flagships, not volume drivers.

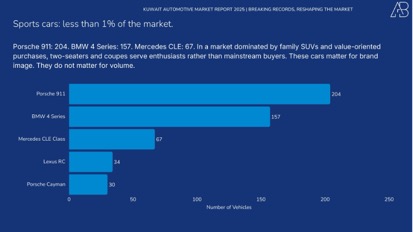

Sports Cars: Less Than 1%

Sports cars account for less than 1% of Kuwait's vehicle market. The Porsche 911, Corvette, and Mustang sell in hundreds, not thousands. In a market dominated by family SUVs and value-oriented purchases, two-seaters and coupes serve enthusiasts rather than mainstream buyers.

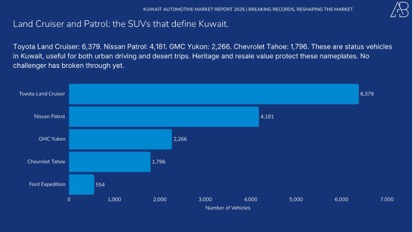

Extended SUVs: Land Cruiser and Patrol

The Toyota Land Cruiser (6,379 units) and Nissan Patrol (4,181) still dominate large, three-row SUVs. These are status vehicles in Kuwait, useful for both urban driving and desert trips. GMC Yukon (2,266), Chevrolet Tahoe (1,796), and Ford Expedition (554) offer the American alternative.

Full-Size SUVs: Prado vs Chinese Challengers

The Toyota Prado dominates full-size SUVs at 7,650 units. But Chinese challengers are climbing. The GWM H9 and Jetour T2 offer similar size and features at lower price points. Whether they can convert Prado intenders depends on long-term reliability perceptions and resale values.

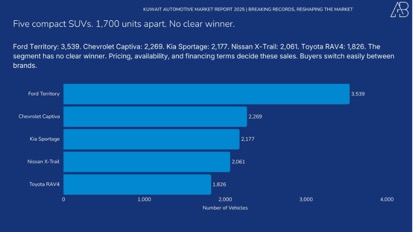

Compact SUVs: Five-Way Battle

The compact SUV segment has no clear winner. Ford Territory (3,539), Chevrolet Captiva (2,269), Kia Sportage (2,177), Nissan X-Trail (2,061), and Toyota RAV4 (1,826) are separated by just 1,700 units. Pricing, availability, and financing terms decide these sales.

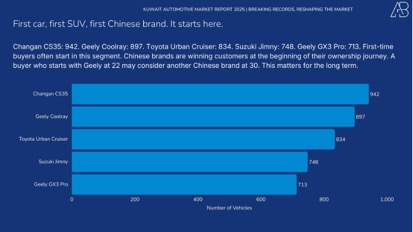

Subcompact SUVs: China's Entry Point

First-time buyers often start here. Changan CS35 (942), Geely Coolray (897), Toyota Urban Cruiser (834), Suzuki Jimny (748), and Geely GX3 Pro (713) lead this entry segment. Chinese brands are winning customers at the beginning of their ownership journey.

This matters for the long term. A buyer who starts with a Geely at 22 may consider another Chinese brand at 30.

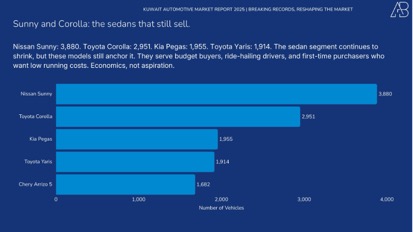

Small Sedans: Sunny and Corolla

The sedan segment continues to shrink, but the Nissan Sunny (3,880) and Toyota Corolla (2,951) still anchor it. These vehicles serve budget buyers, ride-hailing drivers, and first-time purchasers who want low running costs.

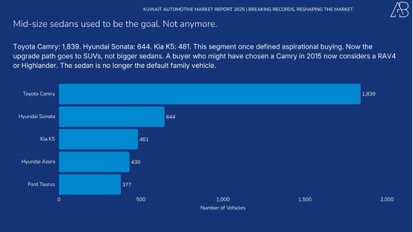

Mid-Size Sedans: Lost Ground

The Toyota Camry leads at 1,839 units, with Hyundai Sonata (644), Kia K5 (481), Hyundai Azera (430), and Ford Taurus (377) following. This segment once defined aspirational buying. SUVs have taken that role.

A buyer who might have chosen a Camry in 2015 now considers a RAV4 or Highlander. The sedan is no longer the default family vehicle.

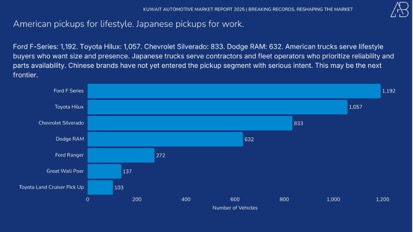

Pickups: American vs Japanese

The pickup market splits cleanly. Ford F-Series (1,192) and Toyota Hilux (1,057) lead, followed by Chevrolet Silverado (833) and Dodge RAM (632). American trucks serve lifestyle buyers who want size and presence. Japanese trucks serve contractors and fleet operators who prioritize reliability and parts availability.

Chinese brands have not yet entered the pickup segment with serious intent. This may be the next frontier as they build credibility in passenger vehicles.

Where Things Stand

Japan holds 40% of Kuwait's car market. China holds 28%. The gap was 55 percentage points in 2013. It is 12 points now.

What the Data Shows

The 151,489 vehicles sold in 2025 set a record. But the composition matters more than the total. SUVs have taken over. Chinese brands have established themselves. The premium segment is shrinking. Dealer concentration is high.

These are measurable facts from registration data. What comes next depends on product cycles, pricing decisions, and whether Chinese brands can maintain quality as they scale.

The old assumptions no longer apply. For dealers, that means rethinking floor plans and brand bets. For OEMs, it means Kuwait offers a preview of how mature markets respond when new competitors offer more for less. For buyers, the options have never been wider, and the data suggests they know it.

Data: Kuwait Ministry of Interior vehicle registrations, 2013-2025

Want to Go Deeper?

This analysis builds on our ongoing coverage of Kuwait's automotive market. If you found this useful, here are related pieces that explore different angles:

• Kuwait Auto Market Mid-Year 2025: Winners, Losers & Trends — The mid-year snapshot that tracked the market on its way to this record.

• GCC Car Rankings 2024 — How Kuwait's buying patterns compare to Qatar, Saudi Arabia, the UAE, Oman, and Bahrain.

• A Decade of Kuwait's Automotive Evolution (2013–2024) — The longer arc of how we got here.

• Why Are SUVs Taking Over Kuwait's Roads? — The structural shift toward SUVs and what's driving it.

• Kuwait's Automotive Revolution (2013–2023) — Brand dominance, market shifts, and the first signs of Chinese brand growth.

All available at alibahbahani.com/blog-and-insights

At Ali Bahbahani and Partners, we work with automotive brands, dealerships, and investors to turn market data into strategy. If you're looking to understand how these shifts affect your business, or where the opportunities are in this changing market, let's talk.

Exploring a transformation of your own? See how we approach Business Transformation.