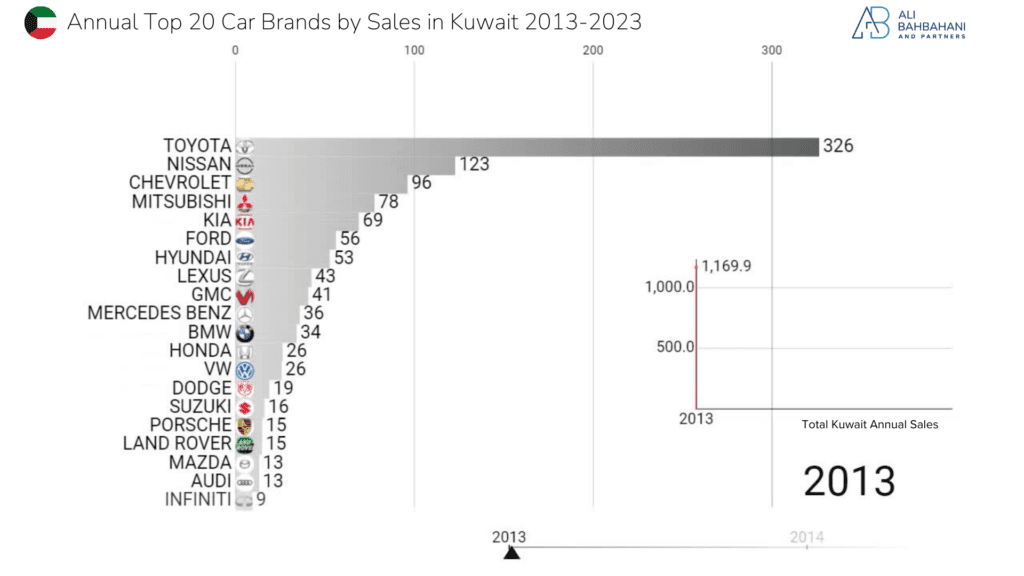

Kuwait's Automotive Revolution (2013-2023)

%201-min.avif)

.webp)

If you want to understand how a country is changing, watch what it drives. Kuwait's vehicle market between 2013 and 2023 is one of the cleanest windows into how the country's tastes, budgets, and loyalties have shifted over a decade. I have been tracking the registration data for years and the picture that emerges is not the one the dealers tell you at the showroom. The Kuwaiti market shifted underneath the traditional players while most of them were still congratulating themselves for holding share, and the customer journey that used to end at a Japanese dealership now routinely ends at a Chinese one.

This piece walks through the decade with the numbers in front of it. The data comes from the Ministry of Interior's official vehicle registration records, and where I have an opinion I will say so rather than hide behind the chart.

The Brands That Held the Top of the Market

Two names have anchored Kuwait's market across the entire decade, and they tell very different stories.

- Toyota is the story that has not changed. Sales kept climbing through the decade and cleared 30,000 units in 2023, with a steady 4% compound annual growth rate between 2018 and 2023. You can argue about why Toyota wins in Kuwait but the answer is not interesting: it wins on reliability, on resale value, and on the fact that Al-Sayer's dealer network makes service frictionless in a country where most dealers still do not respect the customer's time. Ask any Kuwaiti family why they keep going back and you will get the same answer phrased three different ways. The brand has earned something closer to inheritance than loyalty.

- Geely is the story that has changed the most. It arrived with modest numbers and was almost invisible before 2018. By 2023 it was clearing 2,600 units a year, and that undersells how quickly the Chinese brand conversation has moved. Geely is not alone — MG has pulled a parallel trick, and Changan is accelerating behind them. The interesting question is no longer whether Kuwaitis will buy Chinese vehicles with modern technology inside them. They already are. The question is which brand is going to get bought at scale next.

The Shift Toward Affordability, and Why Luxury Stopped Growing

The decade's big consumer story is not that Kuwaitis stopped buying luxury. It is that luxury stopped growing at the pace it used to. BMW, Lexus, and Mercedes-Benz are still strong performers in absolute terms. Walk through any Avenues parking lot on a Friday night and the mix of German badges is the same as it has been for a decade. What has changed is the growth curve.

- Lexus peaked in 2018 and slipped slightly in the years after. My read is that a chunk of the upgrade demand that used to flow into Lexus now flows into a better-equipped Toyota or into an Asian premium brand at a lower price point. The Lexus buyer is a creature of habit, and the new buyer in that income bracket is not automatically a Lexus buyer anymore.

- Electric vehicles are still a rounding error in Kuwait. I have been asked for five years in a row whether this is the year EVs break through. It is not. The charging infrastructure is not there, the electricity pricing does not reward the switch, and the climate does battery life no favours. That said, Tesla's aggressive push into Saudi Arabia is the first real pressure I have seen on the wider region. If Saudi gets a charging network and meaningful Tesla service footprint, Kuwait's timeline accelerates whether the ministries here want it to or not.

The Economic Shock Years and What They Exposed

Every market eventually gets stress-tested. For Kuwait's car market, the test was 2020. Economic shocks do not affect every brand the same way, and the pandemic year was a clean illustration of who had a real customer relationship and who was just riding the rising tide.

- Kia and Ford rebounded fastest. Both have a broad price ladder and are not dependent on the luxury customer feeling wealthy. They were back at pre-pandemic volumes within 18 months.

- Rolls-Royce and the ultra-luxury end of the market took longer. That should surprise nobody — the ultra-luxury buyer's car purchase is about confidence signalling, and confidence was in short supply that year.

- Chinese brands came out of the pandemic faster than anyone. Changan and MG both posted growth rates that would have been unthinkable three years earlier. I am not going to pretend it is a coincidence that the pandemic started in China, but the more interesting reading is that Chinese manufacturers had supply chain control, pricing flexibility, and digital-first sales models exactly when the rest of the industry was stuck. They were ready for the recovery while everyone else was still apologising for the disruption.

Country of Origin: Who Gained, Who Lost

Between 2018 and 2022, the split of the Kuwaiti market by country of origin moved meaningfully. The Japanese share is still the largest slice but it is no longer the growing one.

- Chinese vehicles grew at roughly 30% CAGR post-2020. No other country of origin came close.

- Indian brands fell by about 24% over the same window. Indian vehicles never really took off in Kuwait and they are unlikely to now. The price advantage that India relies on elsewhere is fully covered by Chinese alternatives that are better equipped and frankly better looking.

- Korean brands slipped about 6%. Korean manufacturers have been the quiet professionals of the Kuwaiti market for years, but the Chinese squeeze has hit their value segment harder than Korea's marketing departments want to admit.

The Movement Across Vehicle Classes

Segment by segment, the decade rearranged itself in ways that tell you more about the consumer than any survey could.

- Economy: Roughly 15% CAGR post-pandemic. MG and Geely led the charge. The Kuwaiti customer who five years ago considered a used Japanese car as the cheap option is now considering a new Chinese car at the same monthly payment, with newer tech in the dashboard. That is a permanent shift, not a blip.

- Luxury and ultra-luxury: Still strong in absolute numbers but with declining momentum. Some models at the top of the range saw drops of up to 7%. The buyer who used to upgrade their Range Rover every two years is now keeping it for four, because the new model is not different enough to justify the replacement.

SUVs Kept Taking Share

The one trend that did not surprise me was the continued rise of the SUV.

- SUVs grew at about 7% CAGR from 2018 to 2022. Between school runs, family sizes, the informal carpooling culture here, and the fact that Kuwait's roads occasionally ask for clearance the sedan cannot give you, the SUV has become the default family vehicle. It is not a fashion — it is a fit to the actual conditions.

- Passenger vehicles dropped by about 6% over the same period. The sedan is becoming a second-car purchase rather than a first-car purchase for most households, and the data reflects that.

Watch the Decade in Motion

I built a bar chart race of the annual sales for every major brand from 2013 to 2023 because the static charts miss the story. Watching the ranking reshuffle month by month shows you something no summary can: the moment a brand stops climbing, the year a new entrant breaks in, the brands that looked unshakeable in 2015 and are fighting for relevance now. It is a short video and it is worth the four minutes.

What Happens Next

The decade ahead is not going to look like the decade behind. My read is this.

Toyota and Lexus will stay on top of their respective segments. Toyota because Kuwait has a hereditary relationship with the brand, Lexus because there is no credible alternative in the Japanese premium space for the customer who wants Japanese reliability with a quiet badge. That does not mean they will grow. It means they will defend.

The Chinese brands are going to keep gaining share, and by 2028 they will be the second-largest country-of-origin grouping in the Kuwaiti market if current trends hold. The only thing that stops them is a failure in after-sales service, which is the traditional Achilles heel of Chinese manufacturers in this region. If one of them solves service at scale before the others, that brand will pull ahead of the rest.

EVs are a 2027 conversation for Kuwait, not a 2025 one, unless Saudi forces the timeline.

For dealers, importers, and brand owners operating in this market, the lesson of the decade is that customer loyalty in Kuwait is not what it used to be. It still exists, but the thing the Kuwaiti buyer is loyal to is quieter: it is competent after-sales, respectful service, and a dealership experience that does not waste their time. The brands that win the next decade are the ones that treat that as a customer experience problem, not a marketing problem.

If you want to talk about what the data is saying about your segment, reach out. I keep this dataset current and I would rather discuss it specifically than generically.