Kuwait's Payment Revolution: 2025 Spending Trends

.webp)

In almost every business conversation this year, the same concern surfaces: spending is down. Retailers report softer footfall. Restaurateurs describe cautious diners. Furniture showrooms talk about longer decision cycles. The sentiment is consistent enough to feel like fact.

The numbers confirm it. In November, Al-Qabas reported that consumer spending had fallen by KD 1.68 billion in the first nine months of 2025, a 4.7 per cent decline. Cash withdrawals dropped over 10 per cent. Online spending retreated 8 per cent. An NBK report called it a 'natural correction' after the post-pandemic surge of 2021 and 2022.

We wanted to understand what the Central Bank's own payment statistics actually showed. Not sentiment. Not surveys. The transaction-level data that tracks every card swipe, every online purchase, every ATM withdrawal, every mobile payment across the entire banking system.

Walk into any café in Kuwait City today, and you will notice something that would have seemed impossible a decade ago: the person ahead of you just paid KD 1.200 for a coffee by tapping their phone. No cash. No card. Just a quick beep and a receipt.

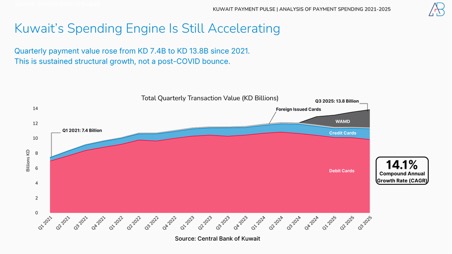

According to the Central Bank of Kuwait's latest payment statistics, quarterly consumer spending has nearly doubled from KD 7.4 billion in Q1 2021 to KD 13.8 billion in Q3 2025, representing a compound annual growth rate of 14.1 per cent. But this headline masks a more complex story, one that explains why the data says 'growth' while businesses feel 'pressure.'

The Great Behavioural Shift

Something fundamental changed in how Kuwait pays.

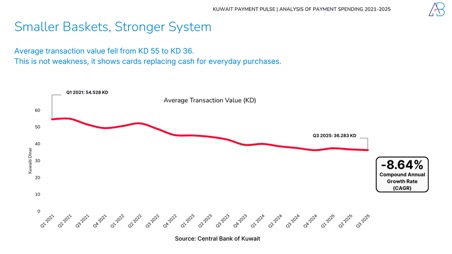

In 2021, the average transaction was KD 55. By Q3 2025, it had fallen to KD 36, a decline of one-third. At first glance, this looks like weakness. It isn't. It's the opposite.

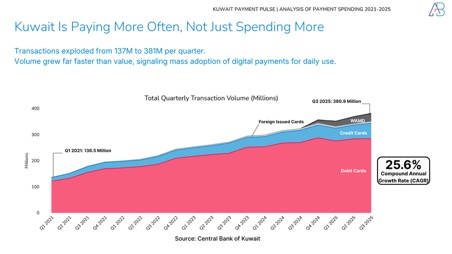

Kuwaitis aren't spending less. They're spending more often. Transaction volumes exploded from 137 million per quarter to 381 million, a 25.6 per cent compound annual growth rate that outpaces value growth by nearly double.

This is what payment maturity looks like. Cards and digital wallets are no longer reserved for big-ticket purchases. They've become the default for coffee, groceries, parking, and everything in between. The shift from 'cards for shopping' to 'cards for living' is now complete.

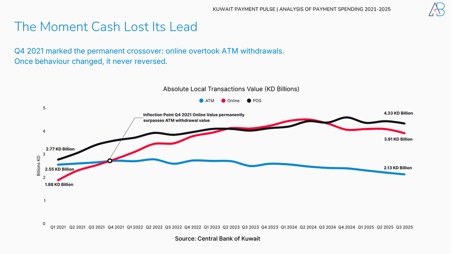

Q4 2021: The Moment Cash Lost Its Lead

If you had to pick a single quarter that changed Kuwait's payment landscape, it would be Q4 2021.

That was when online payment value permanently overtook ATM withdrawals. Before that quarter, cash was still king for value. After it, the lines never crossed back. Online payments have since grown from KD 1.88 billion to KD 3.91 billion per quarter, while ATM withdrawals have declined from KD 2.55 billion to KD 2.13 billion.

The crossover wasn't gradual. It was an inflection point. Once behaviour changed, it never reversed.

The Cash Era Is Ending, Quietly but Permanently

The channel mix tells the clearest story of structural change.

2021 Channel Share:

ATM: 35.4% | POS: 38.5% | Online: 26.1%

Q3 2025 Channel Share:

ATM: 16.7% | POS: 33.9% | Online: 30.6% | WAMD: 18.9%

ATM share has halved. Online has grown. And a new category, WAMD (the national instant payment system), captured nearly 19 per cent of the market in just four quarters.

This isn't cannibalisation. It's expansion. WAMD didn't steal share from cards. It formalised spending that was previously fragmented or invisible: payment links, cash transactions with service providers, bank transfers that never entered the card system.

WAMD: The Disruptor That Rewrote the Map

WAMD's rise deserves special attention.

Launched in late 2024, WAMD scaled from zero to KD 2.4 billion per quarter by Q3 2025. In four quarters, it processed over 32 million transactions and captured 19 per cent of the payment market.

But here's the insight most analyses miss: WAMD isn't replacing cards. It's replacing cash and bank transfers.

Think about how Kuwaitis used to pay their driver, their housekeeper, their car wash service. Cash. Or a bank transfer that required logging into an app, entering account details, and waiting for confirmation. WAMD turned those transactions into instant, phone-to-phone payments.

This is why traditional card spending actually declined in 2025. Looking at Q1-Q3 data:

2024 Q1-Q3 (Cards Only): KD 33.7 billion

2025 Q1-Q3 (Cards Only): KD 31.8 billion

Change: -5.6%

Without WAMD, Kuwait's payment market would have contracted. With WAMD, total spending reached KD 37.9 billion, up 12.4 per cent year-over-year.

Growth didn't slow. It changed form.

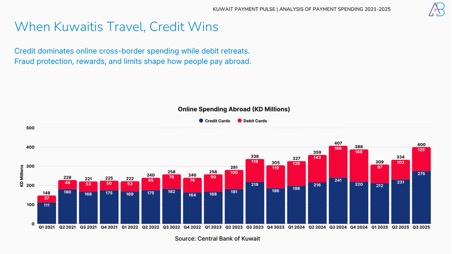

Summer Travel: A Clockwork Pattern

Every Q3, Kuwaiti spending abroad spikes. Every single year since 2021, without exception.

Q3 Abroad Spending:

2021: KD 551 million | 2022: KD 806 million | 2023: KD 901 million

2024: KD 944 million | 2025: KD 1,042 million

At the Q3 2025 peak, Kuwaitis were spending over KD 11 million per day abroad, a scale large enough to materially affect domestic retail and hospitality demand within a single season.

The summer travel peak is now structural. It's not discretionary spending that varies with economic conditions. It's a predictable rhythm that retailers, banks, and travel companies can build their calendars around.

For businesses targeting Kuwaiti consumers, this pattern is actionable intelligence. Q3 is when wallets open abroad. Q4 is when they open at home for year-end shopping and gifting.

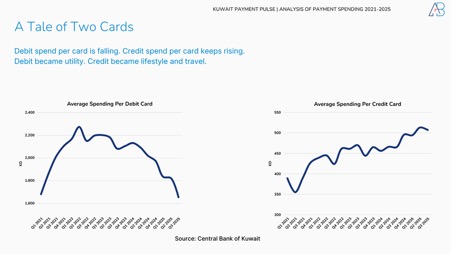

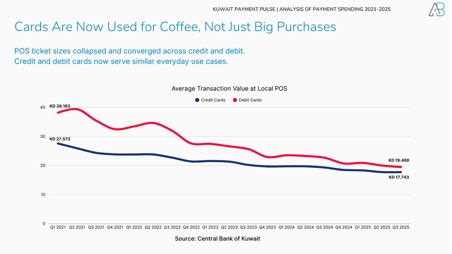

A Tale of Two Cards

Not all cards are created equal. The data reveals a clear divergence between credit and debit behaviour.

On a per-card basis, credit spending continues to rise while debit has retreated from its post-pandemic peak. Debit cards now carry the rhythm of everyday life, groceries, utilities, and obligations. Credit cards fund discretionary moments, travel, dining, and online shopping from abroad.

Credit Cards:

Average spend per card is rising. Dominates online cross-border spending. Transaction growth outpacing debit.

Debit Cards:

Average spend per card is falling from the 2022 peak. Still dominates domestic POS (but its share is shrinking). Transaction sizes are converging with credit at POS.

Debit is a universal infrastructure; Kuwait now has more debit cards in circulation than people. Credit remains selective, concentrated among higher-income, professionally employed segments. That selectivity explains why credit spend per card continues to rise even as overall card growth slows.

When a Kuwaiti consumer pays for coffee, they tap whatever card is in their wallet. But when they book a flight, shop online from abroad, or make a large purchase, they reach for credit. The fraud protection, rewards, and international acceptance of credit cards make them the preferred tool for cross-border spending.

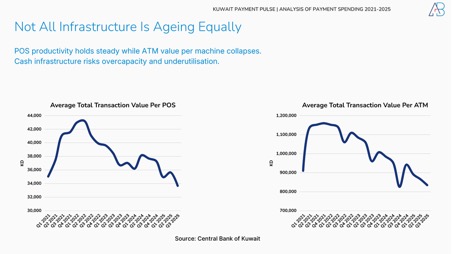

The Infrastructure Story

None of this happens without infrastructure. Kuwait built the foundation before the boom.

Since 2021:

POS terminals: +49% (now over 109,000)

Valid cards in circulation: +51% (now over 7.4 million)

Infrastructure expansion enabled behaviour change, not the other way around. Banks and payment providers invested in terminals and card issuance, and consumers followed.

But not all infrastructure is ageing equally. POS productivity has held relatively steady. However, the ATM value per machine has collapsed. Cash infrastructure is becoming overcapacity. Banks will need to rationalise their ATM networks as digital payments continue to grow.

Why Businesses Feel the Squeeze

If spending is growing at 14 per cent annually, why do so many businesses report the opposite?

Three forces are reshaping where money flows, and who captures it.

First, basket sizes have collapsed. The average transaction fell from KD 55 to KD 36—a 34 per cent decline. Consumers are making nearly three times as many transactions, but each one is smaller. For merchants whose economics depend on average ticket size, this feels like a contraction even when total volume grows.

Second, WAMD is bypassing traditional merchants entirely. Billions of dinars per quarter now move through instant person-to-person payments—money that flows directly between individuals without ever touching a retail cash register. The driver, the housekeeper, the private tutor: transactions that once required cash now happen digitally, but outside the merchant economy.

Third, summer travel is exporting demand. Over KD 11 million per day left Kuwait during Q3 2025, spent in London, Istanbul, Milan, and Dubai rather than in local malls and restaurants. That's retail turnover that simply isn't available to domestic businesses during the peak season.

The spending engine is running. But the pipes have changed. Businesses positioned for the old plumbing feel the pressure most acutely.

What This Means for Kuwait

The Central Bank data reveals four structural shifts that will shape Kuwait's economy for years to come:

1. The future of payments is frequency, not size. More transactions, smaller values. This favours payment systems with low per-transaction costs and rewards businesses that can capture high-frequency, low-value purchases.

2. WAMD is formalising the informal economy. Cash transactions that were invisible to the financial system are now tracked, taxed, and measured. This has implications for government revenue, economic planning, and financial inclusion.

3. Credit and debit are diverging in purpose. Debit for daily utility. Credit for lifestyle, travel, and protection. Banks should position their products accordingly, and merchants should understand which card their customers are likely to use.

4. Seasonal patterns are structural, not cyclical. Q3 travel peaks and Q4 shopping surges are predictable. Businesses that align inventory, marketing, and staffing to these rhythms will outperform those that don't.

Looking Ahead

Kuwait's payment transformation is not complete. If anything, the pace is accelerating.

The convergence of card evolution, digital banking infrastructure, and WAMD adoption suggests we're entering a new phase where the distinction between 'cash', 'card', and 'digital' becomes meaningless to consumers.

The winners will be those who treat payments not as a cost centre but as a customer experience advantage, whether through smooth checkout, embedded financing, or rewards that actually matter.

Kuwait's payment revolution illustrates how rapidly consumer behaviour can evolve when technology, demographics, and regulation align. The Central Bank data shows us where we've been. The question for businesses is whether they're ready for where we're going.

Daily spending is not only where Kuwait’s payment growth lives; it is the single largest line in a Kuwaiti household’s entire life. In The Kuwaiti Dream, Priced, we modelled one household from birth to 80: daily living absorbs KD 1.07 million of a KD 4.13 million lifetime total — more than state health and education combined.

Ali Bahbahani is the founder of Ali Bahbahani & Partners, a Kuwait-based consultancy specialising in customer experience and digital transformation across the GCC.

Source: Central Bank of Kuwait, Payment Statistics, 2021-2025